MetLife 2010 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2010 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

|

|

Retirement Products. Policyholder account balances are held for fixed deferred annuities and the fixed account portion of variable

annuities, for certain income annuities, and for certain portions of guaranteed benefits. Policyholder account balances are credited interest at

a rate set by the Company. Credited rates for deferred annuities are influenced by current market rates, and most of these contracts have a

minimum guaranteed rate between 1.0% and 4.0%. See “— Variable Annuity Guarantees.”

Corporate Benefit Funding. Policyholder account balances are comprised of funding agreements. Interest crediting rates vary by type of

contract, and can be fixed or variable. Variable interest crediting rates are generally tied to an external index, most commonly 1-month or

3-month LIBOR. MetLife is exposed to interest rate risks, and foreign exchange risk when guaranteeing payment of interest and return of

principal at the contractual maturity date. The Company may invest in floating rate assets, or enter into floating rate swaps, also tied to external

indices, as well as caps to mitigate the impact of changes in market interest rates. The Company also mitigates its risks by implementing an

asset/liability matching policy and seeks to hedge all foreign currency risk through the use of foreign currency hedges, including cross

currency swaps.

International. Policyholder account balances are held largely for fixed income retirement and savings plans in Japan and Latin America

and to a lesser degree, amounts for unit-linked-type funds in certain countries across all regions that do not meet the GAAP definition of

separate accounts. Also included are certain liabilities for retirement and savings products sold in certain countries in Japan and Asia Pacific

that generally are sold with minimum credited rate guarantees. Liabilities for guarantees on certain variable annuities in Japan and Asia Pacific

are established in accordance with derivatives and hedging guidance and are also included within policyholder account balances. These

liabilities are generally impacted by sustained periods of low interest rates, where there are interest rate guarantees. The Company mitigates

its risks by implementing an asset/liability matching policy and by hedging its variable annuity guarantees. Liabilities for unit-linked-type funds

are impacted by changes in the fair value of the associated underlying investments, as the return on assets is generally passed directly to the

policyholder. See “— Variable Annuity Guarantees.”

Variable Annuity Guarantees

The Company issues certain variable annuity products with guaranteed minimum benefits that provide the policyholder a minimum return

based on their initial deposit (i.e., the benefit base) less withdrawals. In some cases the benefit base may be increased by additional deposits,

bonus amounts, accruals or market value resets. These guarantees are accounted for as insurance liabilities or as embedded derivatives

dependingonhowandwhenthebenefitispaid.Specifically,aguaranteeisaccountedforasanembeddedderivativeifaguaranteeispaid

without requiring (i) the occurrence of specific insurable event, or (ii) the policyholder to annuitize. Alternatively, a guarantee is accounted for

as an insurance liability if the guarantee is paid only upon either (i) the occurrence of a specific insurable event, or (ii) upon annuitization. In

certain cases, a guarantee may have elements of both an insurance liability and an embedded derivative and in such cases the guarantee is

accounted for under a split of the two models.

The net amount at risk (“NAR”) for guarantees can change significantly during periods of sizable and sustained shifts in equity market

performance, increased equity volatility, or changes in interest rates. The NAR disclosed in Note 8 of the Notes to the Consolidated Financial

Statements represents management’s estimate of the current value of the benefits under these guarantees if they were all exercised

simultaneously at December 31, 2010 and 2009, respectively. However, there are features, such as deferral periods and benefits requiring

annuitization or death, that limit the amount of benefits that will be payable in the near future.

Guarantees, including portions thereof, accounted for as embedded derivatives, are recorded at estimated fair value and included in

policyholder account balances. Guarantees accounted for as embedded derivatives include GMAB, the non life-contingent portion of GMWB

and the portion of certain GMIB that do not require annuitization. For more detail on the determination of estimated fair value, see Note 5 of the

Notes to the Consolidated Financial Statements.

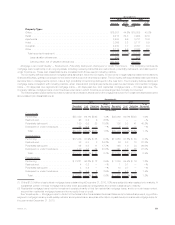

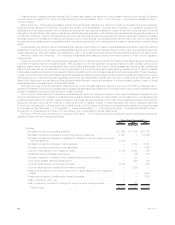

The table below contains the carrying value for guarantees included in policyholder account balances at:

2010 2009

December 31,

(In millions)

U.S. Business:

Guaranteedminimumaccumulationbenefit ...................................... $ 44 $ 60

Guaranteedminimumwithdrawalbenefit ........................................ 173 154

Guaranteedminimumincomebenefit .......................................... (51) 66

International:

Guaranteedminimumaccumulationbenefit ...................................... 454 195

Guaranteedminimumwithdrawalbenefit ........................................ 1,936 1,025

Total ............................................................... $2,556 $1,500

Included in net derivative gains (losses) for the years ended December 31, 2010 and 2009 were gains (losses) of ($269) million and

$1,806 million, respectively, in embedded derivatives related to the change in estimated fair value of the guarantees. The carrying amount of

guarantees accounted for at estimated fair value includes an adjustment for nonperformance risk. In connection with this adjustment, gains

(losses) of ($96) million and ($1,932) million are included in the gains (losses) of ($269) million and $1,806 million in net derivative gains

(losses) for the year ended December 31, 2010 and 2009, respectively.

The estimated fair value of guarantees accounted for as embedded derivatives can change significantly during periods of sizable and

sustained shifts in equity market performance, equity volatility, interest rates or foreign exchange rates. Additionally, because the estimated

fair value for guarantees accounted for at estimated fair value includes an adjustment for nonperformance risk, a decrease in the Company’s

credit spreads could cause the value of these liabilities to increase. Conversely, a widening of the Company’s credit spreads could cause the

value of these liabilities to decrease. The Company uses derivative instruments and reinsurance to mitigate the liability exposure, risk of loss

and the volatility of net income associated with these liabilities. The derivative instruments used are primarily equity and treasury futures,

equity options and variance swaps, and interest rate swaps. The change in valuation arising from the nonperformance risk is not hedged.

59MetLife, Inc.