MetLife 2010 Annual Report Download - page 217

Download and view the complete annual report

Please find page 217 of the 2010 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

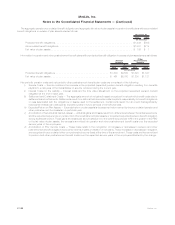

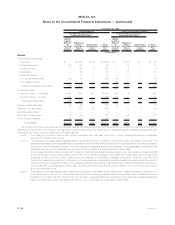

|

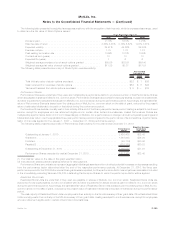

|

Balance,

January 1, Earnings

Other

Comprehensive

Income (Loss)

Purchases,

Sales,

Issuances and

Settlements

Transfer Into

and/or Out

of Level 3 Balance,

December 31,

Total Realized/Unrealized

Gains (Losses) included in:

(In millions)

Year Ended December 31, 2009:

Pension:

Fixed maturity securities:

Corporate................ $ 57 $ (5) $ 21 $ (3) $(2) $ 68

Foreignbonds ............. 4 (1) 5 (3) — 5

Total fixed maturity securities . . 61 (6) 26 (6) (2) 73

Equity securities:

Common stock — domestic . . . . 460 — (232) 13 — 241

Total equity securities . . . . . . . 460 — (232) 13 — 241

Pass-throughsecurities......... 80 (2) 8 (24) 7 69

Derivativesecurities........... 40 36 (39) (37) — —

Otherinvestedassets.......... 392 4 (59) 36 — 373

Total pension assets . . . . . . $1,033 $ 32 $(296) $(18) $ 5 $756

Other postretirement:

Pass-throughsecurities......... $ 13 $(17) $ 17 $ (4) $— $ 9

Total other postretirement

assets .............. $ 13 $(17) $ 17 $ (4) $— $ 9

Totalassets........... $1,046 $15 $(279) $(22) $5 $765

The U.S. Subsidiaries provide employees with benefits under various ERISA benefit plans. These include qualified pension plans,

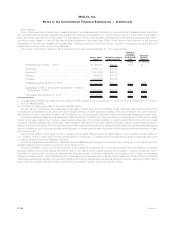

postretirement medical plans and certain retiree life insurance coverage. The assets of the Subsidiaries’ qualified pension plans are held in

insurance group annuity contracts, and the vast majority of the assets of the postretirement medical plan and backing the retiree life coverage

are held in insurance contracts. All of these contracts are issued by Company insurance affiliates, and the assets under the contracts are held

in insurance separate accounts that have been established by the Company. The insurance contract provider engages investment

management firms (“Managers”) to serve as sub-advisors for the separate accounts based on the specific investment needs and requests

identified by the plan fiduciary. These Managers have portfolio management discretion over the purchasing and selling of securities and other

investment assets pursuant to the respective investment management agreements and guidelines established for each insurance separate

account. The assets of the qualified pension plans and postretirement medical plans (the “Invested Plans”) are well diversified across multiple

asset categories and across a number of different Managers, with the intent of minimizing risk concentrations within any given asset category

or with any given Manager.

The Invested Plans, other than those held in participant directed investment accounts, are managed in accordance with investment

policies consistent with the longer-term nature of related benefit obligations and within prudent risk parameters. Specifically, investment

policies are oriented toward (i) maximizing the Invested Plan’s funded status; (ii) minimizing the volatility of the Invested Plan’s funded status;

(iii) generating asset returns that exceed liability increases; and (iv) targeting rates of return in excess of a custom benchmark and industry

standards over appropriate reference time periods. These goals are expected to be met through identifying appropriate and diversified asset

classes and allocations, ensuring adequate liquidity to pay benefits and expenses when due and controlling the costs of administering and

managing the Invested Plan’s investments. Independent investment consultants are periodically used to evaluate the investment risk of

Invested Plan’s assets relative to liabilities, analyze the economic and portfolio impact of various asset allocations and management

strategies and to recommend asset allocations.

Certain foreign subsidiaries sponsor defined benefit plans that cover employees and sales representatives who meet specified eligibility

requirements. Pension benefits are provided utilizing either a traditional formula or cash balance formula, similar to the U.S. plans discussed

above. The investment objectives are also similar, subject to local regulations. Generally, these international pension plans invest directly in

high quality equity and fixed maturity securities. The assets of the foreign pension plans are comprised of cash and cash equivalents, equity

and fixed maturity securities, real estate and hedge fund investments.

Derivative contracts may be used to reduce investment risk, to manage duration and to replicate the risk/return profile of an asset or asset

class. Derivatives may not be used to leverage a portfolio in any manner, such as to magnify exposure to an asset, asset class, interest rates

or any other financial variable. Derivatives are also prohibited for use in creating exposures to securities, currencies, indices or any other

financial variable that are otherwise restricted.

F-128 MetLife, Inc.

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)