MetLife 2010 Annual Report Download - page 165

Download and view the complete annual report

Please find page 165 of the 2010 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

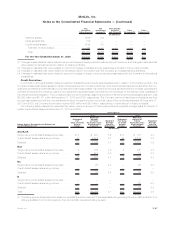

|

|

Option-based — Valuations are based on option pricing models, which utilize significant inputs that may include the swap yield curve,

LIBOR basis curves, and interest rate volatility.

Foreign currency contracts.

Non-option-based — Valuations are based on present value techniques, which utilize significant inputs that may include the swap yield

curve, LIBOR basis curves, currency spot rates, and cross currency basis curves.

Option-based — Valuations are based on option pricing models, which utilize significant inputs that may include the swap yield curve,

LIBOR basis curves, currency spot rates, cross currency basis curves, and currency volatility.

Credit contracts.

Non-option-based — Valuations are based on present value techniques, which utilize significant inputs that may include the swap yield

curve, credit curves, and recovery rates.

Equity market contracts.

Non-option-based — Valuations are based on present value techniques, which utilize significant inputs that may include the swap yield

curve, spot equity index levels, and dividend yield curves.

Option-based — Valuations are based on option pricing models, which utilize significant inputs that may include the swap yield curve,

spot equity index levels, dividend yieldcurves,andequityvolatility.

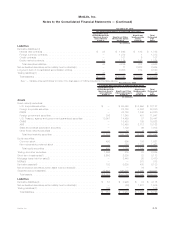

Embedded Derivatives Contained in Certain Funding Agreements

These derivatives are principally valued usinganincomeapproach.Valuationsarebasedonpresentvaluetechniques,whichutilize

significant inputs that may include the swap yield curve and the spot equity and bond index level.

Separate Account Assets

These assets are comprised of investments that are similar in nature to the fixed maturity securities, equity securities, short-term

investments and derivatives referred to above. Also included are certain mutual funds and hedge funds without readily determinable fair

values given prices are not published publicly. Valuation of the mutual funds and hedge funds is based upon quoted prices or reported NAV

provided by the fund managers.

Long-term Debt of CSEs

The estimated fair value of the long-term debt of the Company’s CSEs is based on quoted prices when traded as assets in active markets

or, if not available, based on market standard valuation methodologies, consistent with the Company’s methods and assumptions used to

estimate the fair value of comparable fixed maturity securities.

Level 3 Measurements:

In general, investments classified within Level 3 use many of the same valuation techniques and inputs as described above. However, if

key inputs are unobservable, or if the investments are less liquid and there is very limited trading activity, the investments are generally

classified as Level 3. The use of independent non-binding broker quotations to value investments generally indicates there is a lack of liquidity

or the general lack of transparency in the process to develop the valuation estimates generally causing these investments to be classified in

Level 3.

Fixed Maturity Securities, Equity Securities, Trading and Other Securities and Short-term Investments

This level includes fixed maturity securities and equity securities priced principally by independent broker quotations or market standard

valuation methodologies using inputs that are not market observable or cannot be derived principally from or corroborated by observable

market data. Trading and other securities and short-term investments within this level are of a similar nature and class to the Level 3 securities

described below; accordingly, the valuation techniques and significant market standard observable inputs used in their valuation are also

similar to those described below.

U.S. corporate and foreign corporate securities. These securities, including financial services industry hybrid securities classified

within fixed maturity securities, are principally valued using the market and income approaches. Valuations are based primarily on matrix

pricing or other similar techniques that utilize unobservable inputs or cannot be derived principally from, or corroborated by, observable

market data, including illiquidity premiums and spread adjustments to reflect industry trends or specific credit-related issues. Valuations

may be based on independent non-binding broker quotations. Generally, below investment grade privately placed or distressed

securities included in this level are valued using discounted cash flow methodologies which rely upon significant, unobservable inputs

and inputs that cannot be derived principally from, or corroborated by, observable market data.

Structured securities comprised of RMBS, CMBS and ABS. These securities are principally valued using the market approach.

Valuation is based primarily on matrix pricing or other similar techniques that utilize inputs that are unobservable or cannot be derived

principally from, or corroborated by, observable market data, or are based on independent non-binding broker quotations. Below

investment grade securities and ABS supported by sub-prime mortgage loans included in this level are valued based on inputs including

quoted prices for identical or similar securities that are less liquid and based on lower levels of trading activity than securities classified in

Level 2, and certain of these securities are valued based on independent non-binding broker quotations.

Foreign government and state and political subdivision securities. These securities are principally valued using the market approach.

Valuation is based primarily on matrix pricing or other similar techniques, however these securities are less liquid and certain of the inputs

are based on very limited trading activity.

Common and non-redeemable preferred stock. These securities, including privately held securities and financial services industry

hybrid securities classified within equity securities, are principally valued using the market and income approaches. Valuations are based

primarily on matrix pricing or other similar techniques using inputs such as comparable credit rating and issuance structure. Equity

securities valuations determined with discounted cash flow methodologies use inputs such as earnings multiples based on comparable

F-76 MetLife, Inc.

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)