MetLife 2010 Annual Report Download - page 203

Download and view the complete annual report

Please find page 203 of the 2010 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

|

|

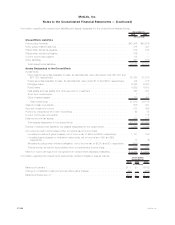

aforementioned IRS settlements. Of the $22 million decrease, $20 million was reclassified to current income tax payable and was paid in

2009. The remaining $2 million reduced interest expense.

During the year ended December 31, 2008, the Company recognized $37 million in interest expense associated with the liability for

unrecognized tax benefits. At December 31, 2008, the Company had $176 million of accrued interest associated with the liability for

unrecognized tax benefits. The $42 million decrease from December 31, 2007 in accrued interest associated with the liability for

unrecognized tax benefits resulted from an increase of $37 million of interest expense and a $79 million decrease primarily resulting from

the aforementioned IRS settlements. Of the $79 million decrease, $78 million was reclassified to current income tax payable in 2008, with

$7 million and $71 million paid in 2008 and 2009, respectively. The remaining $1 million reduced interest expense.

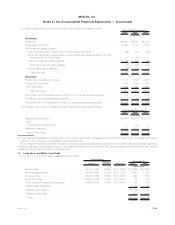

The U.S. Treasury Department and the IRS have indicated that they intend to address through regulations the methodology to be followed

in determining the dividends received deduction (“DRD”), related to variable life insurance and annuity contracts. The DRD reduces the

amount of dividend income subject to tax and is a significant component of the difference between the actual tax expense and expected

amount determined using the federal statutory tax rate of 35%. Any regulations that the IRS ultimately proposes for issuance in this area will be

subject to public notice and comment, at which time insurance companies and other interested parties will have the opportunity to raise legal

and practical questions about the content, scope and application of such regulations. As a result, the ultimate timing and substance of any

such regulations are unknown at this time. For the years ended December 31, 2010 and 2009, the Company recognized an income tax

benefit of $87 million and $216 million, respectively, related to the separate account DRD. The 2010 benefit included an expense of

$57 million related to a true-up of the 2009 tax return. The 2009 benefit included a benefit of $33 million related to a true up of the 2008 tax

return.

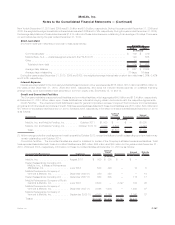

16. Contingencies, Commitments and Guarantees

Contingencies

Litigation

The Company is a defendant in a large number of litigation matters. In some of the matters, very large and/or indeterminate amounts,

including punitive and treble damages, are sought. Modern pleading practice in the United States permits considerable variation in the

assertion of monetary damages or other relief. Jurisdictions may permit claimants not to specify the monetary damages sought or may permit

claimants to state only that the amount sought is sufficient to invoke the jurisdiction of the trial court. In addition, jurisdictions may permit

plaintiffs to allege monetary damages in amounts well exceeding reasonably possible verdicts in the jurisdiction for similar matters. This

variability in pleadings, together with the actual experience of the Company in litigating or resolving through settlement numerous claims over

an extended period of time, demonstrates to management that the monetary relief which may be specified in a lawsuit or claim bears little

relevance to its merits or disposition value.

Due to the vagaries of litigation, the outcome of a litigation matter and the amount or range of potential loss at particular points in time may

normally be difficult to ascertain. Uncertainties can include how fact finders will evaluate documentary evidence and the credibility and

effectiveness of witness testimony, and how trial and appellate courts will apply the law in the context of the pleadings or evidence presented,

whether by motion practice, or at trial or on appeal. Disposition valuations are also subject to the uncertainty of how opposing parties and their

counsel will themselves view the relevant evidence and applicable law.

On a quarterly and annual basis, the Company reviews relevant information with respect to litigation and contingencies to be reflected in

the Company’s consolidated financial statements. The review includes senior legal and financial personnel. Estimates of possible losses or

ranges of loss for particular matters cannot in the ordinary course be made with a reasonable degree of certainty. Liabilities are established

when it is probable that a loss has been incurred and the amount of the loss can be reasonably estimated. Liabilities have been established for

a number of the matters noted below. It is possible that some of the matters could require the Company to pay damages or make other

expenditures or establish accruals in amounts that could not be estimated at December 31, 2010.

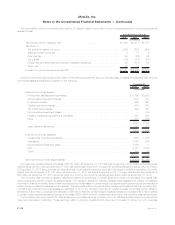

Asbestos-Related Claims

MLIC is and has been a defendant in a large number of asbestos-related suits filed primarily in state courts. These suits principally allege

that the plaintiff or plaintiffs suffered personal injury resulting from exposure to asbestos and seek both actual and punitive damages. MLIC

has never engaged in the business of manufacturing, producing, distributing or selling asbestos or asbestos-containing products nor has

MLIC issued liability or workers’ compensation insurance to companies in the business of manufacturing, producing, distributing or selling

asbestos or asbestos-containing products. The lawsuits principally have focused on allegations with respect to certain research, publication

and other activities of one or more of MLIC’s employees during the period from the 1920’s through approximately the 1950’s and allege that

MLIC learned or should have learned of certain health risks posed by asbestos and, among other things, improperly publicized or failed to

disclose those health risks. MLIC believes that it should not have legal liability in these cases. The outcome of most asbestos litigation

matters, however, is uncertain and can be impacted by numerous variables, including differences in legal rulings in various jurisdictions, the

nature of the alleged injury and factors unrelated to the ultimate legal merit of the claims asserted against MLIC. MLIC employs a number of

resolution strategies to manage its asbestos loss exposure, including seeking resolution of pending litigation by judicial rulings and settling

individual or groups of claims or lawsuits under appropriate circumstances.

Claims asserted against MLIC have included negligence, intentional tort and conspiracy concerning the health risks associated with

asbestos. MLIC’s defenses (beyond denial of certain factual allegations) include that: (i) MLIC owed no duty to the plaintiffs— it had no special

relationship with the plaintiffs and did not manufacture, produce, distribute or sell the asbestos products that allegedly injured plaintiffs;

(ii) plaintiffs did not rely on any actions of MLIC; (iii) MLIC’s conduct was not the cause of the plaintiffs’ injuries; (iv) plaintiffs’ exposure occurred

after the dangers of asbestos were known; and (v) the applicable time with respect to filing suit has expired. During the course of the litigation,

certain trial courts have granted motions dismissing claims against MLIC, while other trial courts have denied MLIC’s motions to dismiss.

There can be no assurance that MLIC will receive favorable decisions on motions in the future. While most cases brought to date have settled,

MLIC intends to continue to defend aggressively against claims based on asbestos exposure, including defending claims at trials.

F-114 MetLife, Inc.

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)