MetLife 2010 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2010 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

|

|

Due to the nature of the underlying risks and the high degree of uncertainty associated with the determination of actuarial liabilities, the

Company cannot precisely determine the amounts that will ultimately be paid with respect to these actuarial liabilities, and the ultimate

amounts may vary from the estimated amounts, particularly when payments may not occur until well into the future.

However, we believe our actuarial liabilities for future benefits are adequate to cover the ultimate benefits required to be paid to

policyholders. We periodically review our estimates of actuarial liabilities for future benefits and compare them with our actual experience. We

revise estimates, to the extent permitted or required under GAAP, if we determine that future expected experience differs from assumptions

used in the development of actuarial liabilities.

The Company has experienced, and will likely in the future experience, catastrophe losses and possibly acts of terrorism, and turbulent

financial markets that may have an adverse impact on our business, results of operations, and financial condition. Catastrophes can be

caused by various events, including pandemics, hurricanes, windstorms, earthquakes, hail, tornadoes, explosions, severe winter weather

(including snow, freezing water, ice storms and blizzards), fires and man-made events such as terrorist attacks. Due to their nature, we cannot

predict the incidence, timing, severity or amount of losses from catastrophes and acts of terrorism, but we make broad use of catastrophic

and non-catastrophic reinsurance to manage risk from these perils.

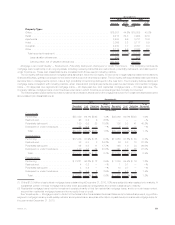

Future Policy Benefits

The Company establishes liabilities for amounts payable under insurance policies. Generally, amounts are payable over an extended

period of time and related liabilities are calculated as the present value of expected future benefits to be paid, reduced by the present value of

expected future net premiums. Such liabilities are established based on methods and underlying assumptions in accordance with GAAP and

applicable actuarial standards. Principal assumptions used in the establishment of liabilities for future policy benefits include mortality,

morbidity, policy lapse, renewal, retirement, investment returns, inflation, expenses and other contingent events as appropriate to the

respective product type. These assumptions are established at the time the policy is issued and are intended to estimate the experience for

the period the policy benefits are payable. Utilizing these assumptions, liabilities are established on a block of business basis. If experience is

less favorable than assumed and future losses are projected under loss recognition testing, then additional liabilities may be required,

resulting in a charge to policyholder benefits and claims.

Insurance Products. Future policy benefits are comprised mainly of liabilities for disabled lives under disability waiver of premium policy

provisions, liabilities for survivor income benefit insurance, long-term care (“LTC”) policies, active life policies and premium stabilization and

other contingency liabilities held under participating life insurance contracts. In order to manage risk, the Company has often reinsured a

portion of the mortality risk on new individual life insurance policies. The reinsurance programs are routinely evaluated and this may result in

increases or decreases to existing coverage. The Company entered into various derivative positions, primarily interest rate swaps and

swaptions, to mitigate the risk that investment of premiums received and reinvestment of maturing assets over the life of the policy will be at

rates below those assumed in the original pricing of these contracts.

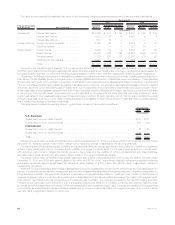

Retirement Products. Future policy benefits are comprised mainly of liabilities for life-contingent income annuities, supplemental

contracts with and without life contingencies, liabilities for Guaranteed Minimum Death Benefits (“GMDBs”) included in certain annuity

contracts, and a certain portion of guaranteed living benefits. See “— Variable Annuity Guarantees.”

Corporate Benefit Funding. Liabilities are primarily related to structured settlement annuities. There is no interest rate crediting flexibility

on these liabilities. A sustained low interest rate environment could negatively impact earnings as a result. The Company has various

derivative positions, primarily interest rate floors and interest rate swaps, to mitigate the risks associated with such a scenario.

Auto & Home. Future policy benefits include liabilities for unpaid claims and claim expenses for property and casualty insurance and

represent the amount estimated for claims that have been reported but not settled and claims incurred but not reported. Liabilities for unpaid

claims are estimated based upon assumptions such as rates of claim frequencies, levels of severities, inflation, judicial trends, legislative

changes or regulatory decisions. Assumptions are based upon the Company’s historical experience and analyses of historical development

patterns of the relationship of loss adjustment expenses to losses for each line of business, and consider the effects of current developments,

anticipated trends and risk management programs, reduced for anticipated salvage and subrogation.

International. Future policy benefits are held primarily for traditional life and accident and health contracts in Japan, Asia Pacific and

immediate annuities in Latin America. They are also held for total return pass-thru provisions included in certain universal life and savings

products mainly in Japan and Latin America, and traditional life, endowment and annuity contracts sold in various countries in Asia Pacific.

They also include certain liabilities for variable annuity guarantees of minimum death benefits, and longevity guarantees sold in Japan and Asia

Pacific. Finally, in Europe and the Middle East, they also include unearned premium liabilities established for credit insurance contracts

covering death, disability and involuntary loss of employment, as well as traditional life, accident and health and endowment contracts.

Factors impacting these liabilities include sustained periods of lower yields than rates established at issue, lower than expected asset

reinvestment rates, higher than expected lapse rates, asset default and more rapid improvement of mortality levels than anticipated for life

contingent immediate annuities. The Company mitigates its risks by implementing an asset/liability matching policy and through the

development of periodic experience studies. See “— Variable Annuity Guarantees.”

Estimates for the liabilities for unpaid claims and claim expenses are reset as actuarial indications change and these changes in the liability

are reflected in the current results of operation as either favorable or unfavorable development of prior year losses.

Banking, Corporate & Other. Future policy benefits primarily include liabilities for quota-share reinsurance agreements for certain LTC

and workers’ compensation business written by MetLife Insurance Company of Connecticut (“MICC”), prior to its acquisition by MetLife, Inc.

These are run-off businesses that have been included within Banking, Corporate & Other since the acquisition of MICC.

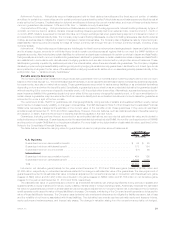

Policyholder Account Balances

Policyholder account balances are generally equal to the account value, which includes accrued interest credited, but exclude the impact

of any applicable surrender charge that may be incurred upon surrender.

Insurance Products. Policyholder account balances are held for death benefit disbursement retained asset accounts, universal life

policies, the fixed account of variable life insurance policies, specialized life insurance products for benefit programs and general account

universal life policies. Policyholder account balances are credited interest at a rate set by the Company, which are influenced by current

market rates. The majority of the policyholder account balances have a guaranteed minimum credited rate between 0.5% and 6.0%. A

sustained low interest rate environment could negatively impact earnings as a result of the minimum credited rate guarantees. The Company

has various derivative positions, primarily interest rate floors, to partially mitigate the risks associated with such a scenario.

58 MetLife, Inc.