MetLife 2012 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2012 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

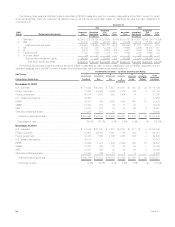

Asia. Future policy benefits for this segment are held primarily for traditional life, endowment, annuity and accident & health contracts. They are also

held for total return pass-through provisions included in certain universal life and savings products. They include certain liabilities for variable annuity and

variable life guarantees of minimum death benefits, and longevity guarantees. Factors impacting these liabilities include sustained periods of lower yields

than rates established at policy issuance, lower than expected asset reinvestment rates, market volatility, actual lapses resulting in lower than expected

income, and actual mortality or morbidity resulting in higher than expected benefit payments. We mitigate our risks by implementing an ALM policy and

through the development of periodic experience studies.

EMEA. Future policy benefits for this segment include unearned premium reserves for group life and credit insurance contracts. Future policy

benefits are also held for traditional life, endowment and annuity contracts with significant mortality risk and accident & health contracts. Factors

impacting these liabilities include sustained periods of lower yields than rates established at issue, lower than expected asset reinvestment rates, market

volatility, actual lapses resulting in lower than expected income, and actual mortality or morbidity resulting in higher than expected benefit payments. We

mitigate our risks by having premiums which are adjustable or cancellable in some cases, implementing an asset/liability matching policy and through

the development of periodic experience studies.

Corporate & Other. Future policy benefits primarily include liabilities for quota-share reinsurance agreements for certain run-off LTC and workers’

compensation business written by MetLife Insurance Company of Connecticut (“MICC”). Additionally, future policy benefits includes liabilities for variable

annuity guaranteed minimum benefits assumed from a former operating joint venture in Japan that are accounted for as insurance.

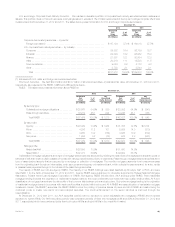

Policyholder Account Balances

PABs are generally equal to the account value, which includes accrued interest credited, but excludes the impact of any applicable surrender charge

that may be incurred upon surrender. See “— Industry Trends — Interest Rate Stress Scenario” and “— Variable Annuity Guarantees.” See also Notes 1

and 4 of the Notes to the Consolidated Financial Statements for additional information.

Retail. Life & Other PABs are held for retained asset accounts, universal life policies and the fixed account of variable life insurance policies. For

Annuities, PABs are held for fixed deferred annuities, the fixed account portion of variable annuities, and non-life contingent income annuities. PABs are

credited interest at a rate set by us, which is influenced by current market rates. A sustained low interest rate environment could negatively impact

earnings as a result of the minimum credited rate guarantees present in most of these PABs. We have various derivative positions, primarily interest rate

floors, to partially mitigate the risks associated with such a scenario. Additionally, PABs are held for variable annuity guaranteed minimum living benefits

that are accounted for as embedded derivatives.

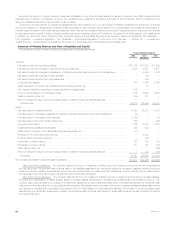

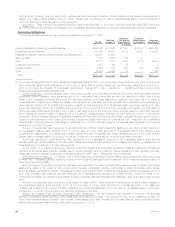

The table below presents the breakdown of account value subject to minimum guaranteed crediting rates for Retail:

December 31, 2012

Guaranteed Minimum Crediting Rate Account

Value(1)

Account

Value at

Guarantee(1)

(In millions)

Life & Other:

Greater than 0% but less than 2% ..................................................... $ 70 $ 70

Equal to 2% but less than 4% ......................................................... $10,761 $ 4,658

Equal to or greater than 4% .......................................................... $10,860 $ 6,577

Annuities:

Greater than 0% but less than 2% ................................................... $ 3,646 $ 2,023

Equal to 2% but less than 4% ....................................................... $34,145 $ 26,157

Equal to or greater than 4% ........................................................ $ 2,946 $ 2,852

(1) The table above is not adjusted for policy loans.

As a result of acquisitions, we establish additional liabilities known as excess interest reserves for policies with credited rates in excess of market

rates as of the applicable acquisition dates. At December 31, 2012, excess interest reserves were $146 million and $386 million for Life & Other and

Annuities, respectively.

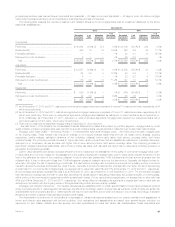

Group, Voluntary & Worksite Benefits. PABs in this segment are held for retained asset accounts, universal life policies, the fixed account of

variable life insurance policies and specialized life insurance products for benefit programs. PABs are credited interest at a rate set by us, which are

influenced by current market rates. A sustained low interest rate environment could negatively impact earnings as a result of the minimum credited rate

guarantees present in most of these PABs. We have various derivative positions, primarily interest rate floors, to partially mitigate the risks associated

with such a scenario.

The table below presents the breakdown of account value subject to minimum guaranteed crediting rates for Group, Voluntary & Worksite Benefits:

December 31, 2012

Guaranteed Minimum Crediting Rate Account

Value(1)

Account

Value at

Guarantee(1)

(In millions)

Greater than 0% but less than 2% ......................................................... $5,305 $ 5,305

Equal to 2% but less than 4% ............................................................ $2,387 $ 2,374

Equal to or greater than 4% .............................................................. $ 596 $ 568

(1) The table above is not adjusted for policy loans.

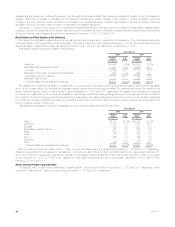

Corporate Benefit Funding. PABs in this segment are comprised of funding agreements. Interest crediting rates vary by type of contract, and can

be fixed or variable. Variable interest crediting rates are generally tied to an external index, most commonly (1-month or 3-month) London Inter-Bank

Offer Rate (“LIBOR”). We are exposed to interest rate risks, as well as foreign currency exchange rate risk when guaranteeing payment of interest and

return of principal at the contractual maturity date. We may invest in floating rate assets or enter into receive-floating interest rate swaps, also tied to

external indices, as well as caps, to mitigate the impact of changes in market interest rates. We also mitigate risks by implementing an ALM policy and

seek to hedge all foreign currency exchange rate risk through the use of foreign currency hedges, including cross currency swaps.

Latin America. PABs in this segment are held largely for deferred annuities mainly in Mexico and Brazil, and for universal life products mainly in

Mexico. Some of the deferred annuities in Brazil are unit-linked-type funds that do not meet the GAAP definition of separate accounts. The rest of the

deferred annuities have minimum credited rate guarantees, and these liabilities and the universal life liabilities are generally impacted by sustained

50 MetLife, Inc.