MetLife 2012 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2012 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

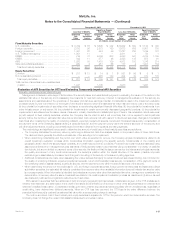

Valuation Allowance Methodology

Mortgage loans are considered to be impaired when it is probable that, based upon current information and events, the Company will be unable

to collect all amounts due under the loan agreement. Specific valuation allowances are established using the same methodology for all three portfolio

segments as the excess carrying value of a loan over either (i) the present value of expected future cash flows discounted at the loan’s original

effective interest rate, (ii) the estimated fair value of the loan’s underlying collateral if the loan is in the process of foreclosure or otherwise collateral

dependent, or (iii) the loan’s observable market price. A common evaluation framework is used for establishing non-specific valuation allowances for

all loan portfolio segments; however, a separate non-specific valuation allowance is calculated and maintained for each loan portfolio segment thatis

based on inputs unique to each loan portfolio segment. Non-specific valuation allowances are established for pools of loans with similar risk

characteristics where a property-specific or market-specific risk has not been identified, but for which the Company expects to incur a credit loss.

These evaluations are based upon several loan portfolio segment-specific factors, including the Company’s experience for loan losses, defaults and

loss severity, and loss expectations for loans with similar risk characteristics. These evaluations are revised as conditions change and new information

becomes available.

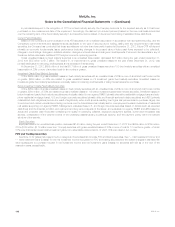

Commercial and Agricultural Mortgage Loan Portfolio Segments

The Company typically uses several years of historical experience in establishing non-specific valuation allowances which captures multiple

economic cycles. For evaluations of commercial loans, in addition to historical experience, management considers factors that include the impact ofa

rapid change to the economy, which may not be reflected in the loan portfolio, and recent loss and recovery trend experience as compared to

historical loss and recovery experience. For evaluations of agricultural loans, in addition to historical experience, management considers factors that

include increased stress in certain sectors, which may be evidenced by higher delinquency rates, or a change in the number of higher risk loans. On

a quarterly basis, management incorporates the impact of these current market events and conditions on historical experience in determining the non-

specific valuation allowance established for each portfolio segment.

All commercial loans are reviewed on an ongoing basis which may include an analysis of the property financial statements and rent roll, lease

rollover analysis, property inspections, market analysis, estimated valuations of the underlying collateral, loan-to-value ratios, debt service coverage

ratios, and tenant creditworthiness. All agricultural loans are monitored on an ongoing basis. The monitoring process focuses on higher risk loans,

which include those that are classified as restructured, potentially delinquent, delinquent or in foreclosure, as well as loans with higher loan-to-value

ratios and lower debt service coverage ratios. The monitoring process for agricultural loans is generally similar to the commercial loan monitoring

process, with a focus on higher risk loans, including reviews on a geographic and property-type basis. Higher risk loans are reviewed individually on

an ongoing basis for potential credit loss and specific valuation allowances are established using the methodology described above for all loan

portfolio segments. Quarterly, the remaining loans are reviewed on a pool basis by aggregating groups of loans that have similar risk characteristics for

potential credit loss, and non-specific valuation allowances are established as described above using inputs that are unique to each segment of the

loan portfolio.

For commercial loans, the primary credit quality indicator is the debt service coverage ratio, which compares a property’s net operating income to

amounts needed to service the principal and interest due under the loan. Generally, the lower the debt service coverage ratio, the higher the risk of

experiencing a credit loss. The Company also reviews the loan-to-value ratio of its commercial loan portfolio. Loan-to-value ratios compare the unpaid

principal balance of the loan to the estimated fair value of the underlying collateral. Generally, the higher the loan-to-value ratio, the higher the risk of

experiencing a credit loss. The debt service coverage ratio and loan-to-value ratio, as well as the values utilized in calculating these ratios, are

updated annually, on a rolling basis, with a portion of the loan portfolio updated each quarter.

For agricultural loans, the Company’s primary credit quality indicator is the loan-to-value ratio. The values utilized in calculating this ratio are

developed in connection with the ongoing review of the agricultural loan portfolio and are routinely updated. Additionally, the Company focuses the

monitoring process on higher risk loans, including reviews on a geographic and property-type basis.

Residential Mortgage Loan Portfolio Segment

The Company’s residential loan portfolio is comprised primarily of closed end, amortizing residential loans. For evaluations of residential loans, the

key inputs of expected frequency and expected loss reflect current market conditions, with expected frequency adjusted, when appropriate, for

differences from market conditions and the Company’s historical experience. In contrast to the commercial and agricultural loan portfolios, residential

loans are smaller-balance homogeneous loans that are collectively evaluated for impairment. Non-specific valuation allowances are established using

the evaluation framework described above for pools of loans with similar risk characteristics from inputs that are unique to the residential segment of

the loan portfolio. Loan specific valuation allowances are only established on residential loans when they have been restructured and are established

using the methodology described above for all loan portfolio segments.

For residential loans, the Company’s primary credit quality indicator is whether the loan is performing or non-performing. The Company generally

defines non-performing residential loans as those that are 90 or more days past due and/or in non-accrual status which is assessed monthly.

Generally, non-performing residential loans have a higher risk of experiencing a credit loss.

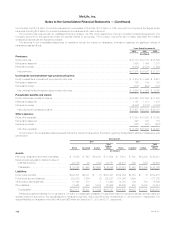

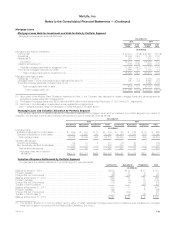

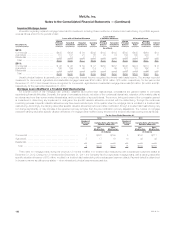

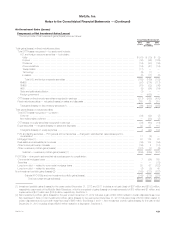

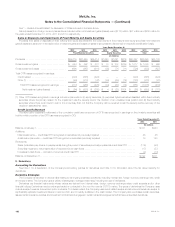

Credit Quality of Commercial Mortgage Loans

Information about the credit quality of commercial mortgage loans held-for-investment is presented below at:

120 MetLife, Inc.