MetLife 2012 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2012 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

Segments and Corporate & Other

The following discussion summarizes the impact of the above hypothetical U.S. interest rate stress scenario on the operating earnings of our

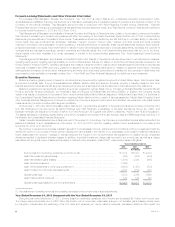

segments, as well as Corporate & Other. See also “— Policyholder Liabilities — Policyholder Account Balances” for information regarding the account

values subject to minimum guaranteed credited rates.

Retail

Life & Other – Our interest rate sensitive products include traditional life, universal life, and retained asset accounts. Because the majority of our

traditional life insurance business is participating, we can largely offset lower investment returns on assets backing our traditional life products through

adjustments to the applicable dividend scale. In our universal life products, we manage interest rate risk through a combination of product design

features and ALM strategies, including the use of hedges such as interest rate swaps and floors. While the Company has the ability to lower crediting

rates on certain in-force universal life policies to mitigate margin compression, such actions would be partially offset by increases in our liabilities related

to those with secondary guarantees. Our retained asset accounts have minimum interest crediting rate guarantees which range from 1.5% to 3.0%, all

of which are currently at their respective minimum interest crediting rates. While we expect to experience margin compression as we re-invest at lower

rates, interest rate floors purchased in this portfolio will partially mitigate this risk.

Annuities – The impact on operating earnings from margin compression is concentrated in our deferred annuities where there are minimum interest

rate guarantees. Under low U.S. interest rate scenarios, we assume that a larger percentage of customers will maintain their funds with the Company to

take advantage of the attractive minimum guaranteed rates and we expect to experience margin compression as we reinvest cash flows at lower

interest rates. Partially offsetting this margin compression, we assume we will lower crediting rates on their contractual reset dates for the portion of

business that is not currently at minimum crediting rates. Additionally, we have various derivative positions, primarily interest rate floors, to partially

mitigate this risk. Reinvestment risk is defined here as the amount of reinvestment in 2013 and 2014 that would impact operating earnings due to

reinvesting cash flows in the hypothetical interest rate stress scenario. For the deferred annuities business, $1.3 billion and $2.3 billion in 2013 and

2014, respectively of the asset base will be subject to reinvestment risk on an average asset base of $37.6 billion and $37.2 billion in 2013 and 2014,

respectively.

We estimate an unfavorable operating earnings impact in our Retail segment from the hypothetical U.S. interest rate stress scenario noted above of

$15 million and $60 million in 2013 and 2014, respectively.

Group, Voluntary & Worksite Benefits

Group – In general, most of our group life insurance products in this segment are renewable term insurance and, therefore, have significant repricing

flexibility. Interest rate risk mainly arises from minimum interest rate guarantees on retained asset accounts. These accounts have minimum interest

crediting rate guarantees which range from 0.5% to 3.0%. All of these account balances are currently at their respective minimum interest crediting rates

and we expect to experience margin compression as we reinvest at lower interest rates. We have used interest rate floors to partially mitigate the risksof

a sustained U.S. low interest rate environment. We also have exposure to interest rate risk in this business arising from our group disability policy claim

reserves. For these products, lower reinvestment rates cannot be offset by a reduction in liability crediting rates for established claim reserves. Group

disability policies are generally renewable term policies. Rates may be adjusted on in-force policies at renewal based on the retrospective experience

rating and current interest rate assumptions. We review the discount rate assumptions and other assumptions associated with our long-term disability

claim reserves no less frequently than annually. Our most recent review at the end of 2012 resulted in no change to the applicable discount rates.

Voluntary & Worksite – We have exposure to interest rate risk in this business arising mainly from our long-term care (“LTC”) policy reserves. For

these products, lower reinvestment rates cannot be offset by a reduction in liability crediting rates for established claim reserves. LTC policies are

generally guaranteed renewable, and rates may be adjusted on a class basis with regulatory approval to reflect emerging experience. Our LTC block is

closed to new business. The Company makes use of derivative instruments to more closely match asset and liability duration and immunize the portfolio

against changes in interest rates. Reinvestment risk is defined here as the amount of reinvestment in 2013 and 2014 that would impact operating

earnings due to reinvesting cash flows in the hypothetical interest rate stress scenario. For the LTC portfolio, $0.9 billion of the asset base in both 2013

and 2014 will be subject to reinvestment risk on an average asset base of $8.0 billion and $8.7 billion in 2013 and 2014, respectively.

We estimate an unfavorable operating earnings impact in our Group, Voluntary & Worksite Benefits segment from the hypothetical U.S. interest rate

stress scenario noted above of $5 million and $20 million in 2013 and 2014, respectively.

Corporate Benefit Funding

This segment contains both short and long duration products consisting of capital market products, pension closeouts, structured settlements, and

other benefit funding products. The majority of short duration products are managed on a floating rate basis, which mitigates the impact of the low

interest rate environment in the U.S. The long duration products have very predictable cash flows and we have matched these cash flows through our

ALM practices. We also use interest rate swaps to help protect income in this segment against a low interest rate environment in the U.S. Based on the

cash flow estimates, only a small component is subject to reinvestment risk. Reinvestment risk is defined here as the amount of reinvestment in 2013

and 2014 that would impact operating earnings due to reinvesting cash flows in the hypothetical interest rate stress scenario. For the long duration

business, $0 and $0.4 billion of the asset base in 2013 and 2014, respectively, will be subject to reinvestment risk on an average asset base of $46.3

billion and $46.2 billion in 2013 and 2014, respectively.

We estimate an unfavorable operating earnings impact in our Corporate Benefit Funding segment from the hypothetical U.S. interest rate stress

scenario noted above of $0 and $10 million in 2013 and 2014, respectively.

Asia

Our Asia segment has a portion of its investments in U.S. dollar denominated assets. The following represents the impact on our Asia segment’s

operating earnings under the hypothetical U.S. interest rate stress scenario.

Life & Other – Our Japan business offers traditional life insurance and accident & health products. To the extent the Japan life insurance portfolio is

U.S. interest rate sensitive and we are unable to lower crediting rates to the customer, operating earnings will decline. We manage interest rate risk on

our life products through a combination of product design features and ALM strategies.

Annuities – We sell annuities in Asia which are predominantly single premium products with crediting rates set at the time of issue. This allows us to

tightly manage product ALM, cash flows and net spreads, thus maintaining profitability.

We estimate an unfavorable operating earnings impact in our Asia segment from the hypothetical U.S. interest rate stress scenario noted above of

$10 million and $20 million in 2013 and 2014, respectively.

10 MetLife, Inc.