MetLife 2012 Annual Report Download - page 117

Download and view the complete annual report

Please find page 117 of the 2012 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

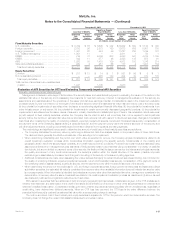

6. Reinsurance

The Company enters into reinsurance agreements primarily as a purchaser for reinsurance for its various insurance products and also as a provider

of reinsurance for some insurance products issued by third parties. The Company participates in reinsurance activities in order to limit losses, minimize

exposure to significant risks and provide additional capacity for future growth.

Accounting for reinsurance requires extensive use of assumptions and estimates, particularly related to the future performance of the underlying

business and the potential impact of counterparty credit risks. The Company periodically reviews actual and anticipated experience compared to the

aforementioned assumptions used to establish assets and liabilities relating to ceded and assumed reinsurance and evaluates the financial strengthof

counterparties to its reinsurance agreements using criteria similar to that evaluated in the security impairment process discussed in Note 8.

Americas — Excluding Latin America

For its Retail Life & Other insurance products, the Company has historically reinsured the mortality risk primarily on an excess of retention basis or on

a quota share basis. The Company currently reinsures 90% of the mortality risk in excess of $2 million for most products and reinsures up to 90% of the

mortality risk for certain other products. In addition to reinsuring mortality risk as described above, the Company reinsures other risks, as well as specific

coverages. Placement of reinsurance is done primarily on an automatic basis and also on a facultative basis for risks with specified characteristics.Ona

case by case basis, the Company may retain up to $20 million per life and reinsure 100% of amounts in excess of the amount the Company retains.

The Company evaluates its reinsurance programs routinely and may increase or decrease its retention at any time.

The Company’s Retail Annuities business reinsures a portion of the living and death benefit guarantees issued in connection with its variable

annuities. Under these reinsurance agreements, the Company pays a reinsurance premium generally based on fees associated with the guarantees

collected from policyholders, and receives reimbursement for benefits paid or accrued in excess of account values, subject to certain limitations. The

value of the embedded derivatives on the ceded risk is determined using a methodology consistent with the guarantees directly written by the Company

with the exception of the input for nonperformance risk that reflects the credit of the reinsurer.

The Company’s Corporate Benefit Funding segment periodically engages in reinsurance activities, as considered appropriate. The impact of these

activities on the financial results of this segment has not been significant.

The Company, through its property & casualty business within both the Retail and Group, Voluntary and Worksite Benefits segments, purchases

reinsurance to manage its exposure to large losses (primarily catastrophe losses) and to protect statutory surplus. The Company cedes to reinsurers

losses and premiums based upon the exposure of the policies subject to reinsurance. To manage exposure to large property and casualty losses, the

Company purchases property catastrophe, casualty and property per risk excess of loss reinsurance protection.

For other policies, the Company generally retains most of the risk and cedes particular risks on certain client arrangements.

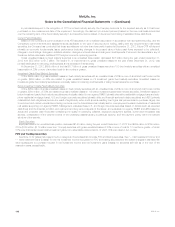

Latin America, Asia and EMEA

For life insurance products, the Company currently reinsures, depending on the product, risks in excess of $5 million to external reinsurers on a

yearly renewable term basis. The Company may also reinsure certain risks with external reinsurers depending upon the nature of the risk and local

regulatory requirements. For selected large corporate clients, the Company reinsures group employee benefits or credit insurance business with various

client-affiliated reinsurance companies, covering policies issued to the employees or customers of the clients. Additionally, the Company cedes and

assumes risk with other insurance companies when either company requires a business partner with the appropriate local licensing to issue certain

types of policies in certain countries. In these cases, the assuming company typically underwrites the risks, develops the products and assumes most

or all of the risk. The Company also has reinsurance agreements in force that reinsure a portion of the living and death benefit guarantees issued in

connection with variable annuity products. Under these agreements, the Company pays reinsurance fees associated with the guarantees collected from

policyholders, and receives reimbursement for benefits paid or accrued in excess of account values, subject to certain limitations.

Corporate & Other

The Company also reinsures, through 100% quota share reinsurance agreements, certain run-off LTC and workers’ compensation business written

by MetLife Insurance Company of Connecticut (“MICC”).

Corporate & Other also has a reinsurance agreement, whereby it assumes the living and death benefit guarantees issued in connection with variable

annuity products. Under this agreement, the Company receives reinsurance fees associated with the guarantees collected from policyholders, and

provides reimbursement for benefits paid or accrued in excess of account values, subject to certain limitations.

Catastrophe Coverage

The Company has exposure to catastrophes which could contribute to significant fluctuations in the Company’s results of operations. In the

Americas, excluding Latin America, the Company uses excess of retention and quota share reinsurance agreements to provide greater diversification of

risk and minimize exposure to larger risks. Currently, for Latin America, Asia and EMEA, the Company purchases catastrophe coverage to insure risks

within certain countries deemed by management to be exposed to the greatest catastrophic risks.

Reinsurance Recoverables

The Company reinsures its business through a diversified group of well-capitalized, highly rated reinsurers. The Company analyzes recent trends in

arbitration and litigation outcomes in disputes, if any, with its reinsurers. The Company monitors ratings and evaluates the financial strength of its

reinsurers by analyzing their financial statements. In addition, the reinsurance recoverable balance due from each reinsurer is evaluated as part of the

overall monitoring process. Recoverability of reinsurance recoverable balances is evaluated based on these analyses. The Company generally secures

large reinsurance recoverable balances with various forms of collateral, including secured trusts, funds withheld accounts and irrevocable letters of

credit. These reinsurance recoverable balances are stated net of allowances for uncollectible reinsurance, which at December 31, 2012 and 2011,

were immaterial.

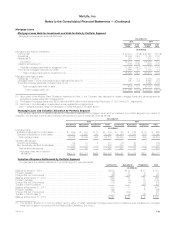

The Company has secured certain reinsurance recoverable balances with various forms of collateral, including secured trusts, funds withheld

accounts and irrevocable letters of credit. The Company had $5.7 billion and $5.6 billion of unsecured reinsurance recoverable balances at

December 31, 2012 and 2011, respectively.

At December 31, 2012, the Company had $14.1 billion of net ceded reinsurance recoverables. Of this total, $10.4 billion, or 74%, were with the

Company’s five largest ceded reinsurers, including $2.8 billion of net ceded reinsurance recoverables which were unsecured. At December 31, 2011,

MetLife, Inc. 111