MetLife 2012 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2012 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

Investment Impairments

One of the significant estimates related to available-for-sale (“AFS”) securities is our impairment evaluation. The assessment of whether an other-

than-temporary impairment (“OTTI”) occurred is based on our case-by-case evaluation of the underlying reasons for the decline in estimated fair value on

a security-by-security basis. Our review of each fixed maturity and equity security for OTTI includes an analysis of gross unrealized losses by three

categories of severity and/or age of gross unrealized loss. An extended and severe unrealized loss position on a fixed maturity security may not have

any impact on the ability of the issuer to service all scheduled interest and principal payments. Accordingly, such an unrealized loss position may not

impact our evaluation of recoverability of all contractual cash flows or the ability to recover an amount at least equal to its amortized cost based on the

present value of the expected future cash flows to be collected. In contrast, for certain equity securities, greater weight and consideration are given to a

decline in estimated fair value and the likelihood such estimated fair value decline will recover.

Additionally, we consider a wide range of factors about the security issuer and use our best judgment in evaluating the cause of the decline in the

estimated fair value of the security and in assessing the prospects for near-term recovery. Inherent in our evaluation of the security are assumptions and

estimates about the operations of the issuer and its future earnings potential. Factors we consider in the OTTI evaluation process are described in Note

8 of the Notes to Consolidated Financial Statements.

The determination of the amount of allowances and impairments on the remaining invested asset classes is highly subjective and is based upon our

periodic evaluation and assessment of known and inherent risks associated with the respective asset class. Such evaluations and assessments are

revised as conditions change and new information becomes available.

See Note 8 of the Notes to the Consolidated Financial Statements for additional information relating to our determination of the amount of allowances

and impairments.

Derivatives

The determination of estimated fair value of freestanding derivatives, when quoted market values are not available, is based on market standard

valuation methodologies and inputs that management believes are consistent with what other market participants would use when pricing the

instruments. Derivative valuations can be affected by changes in interest rates, foreign currency exchange rates, financial indices, credit spreads, default

risk, nonperformance risk, volatility, liquidity and changes in estimates and assumptions used in the pricing models. See Note 10 of the Notes to the

Consolidated Financial Statements for additional details on significant inputs into the over-the-counter (“OTC”) derivative pricing models and credit risk

adjustment.

We issue certain variable annuity products with guaranteed minimum benefits, which are measured at estimated fair value separately from the host

variable annuity product, with changes in estimated fair value reported in net derivative gains (losses). The estimated fair values of these embedded

derivatives are determined based on the present value of projected future benefits minus the present value of projected future fees. The projections of

future benefits and future fees require capital market and actuarial assumptions, including expectations concerning policyholder behavior. A risk neutral

valuation methodology is used under which the cash flows from the guarantees are projected under multiple capital market scenarios using observable

risk free rates. The valuation of these embedded derivatives also includes an adjustment for our nonperformance risk and risk margins for non-capital

market inputs. The nonperformance risk adjustment, which is captured as a spread over the risk free rate in determining the discount rate to discount

the cash flows of the liability, is determined by taking into consideration publicly available information relating to spreads in the secondary market for

MetLife, Inc.’s debt, including related credit default swaps. These observable spreads are then adjusted, as necessary, to reflect the priority of these

liabilities and the claims paying ability of the issuing insurance subsidiaries compared to MetLife, Inc. Risk margins are established to capture the non-

capital market risks of the instrument which represent the additional compensation a market participant would require to assume the risks related to the

uncertainties in certain actuarial assumptions. The establishment of risk margins requires the use of significant management judgment, including

assumptions of the amount and cost of capital needed to cover the guarantees.

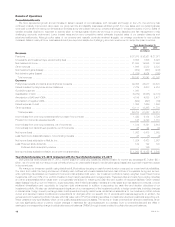

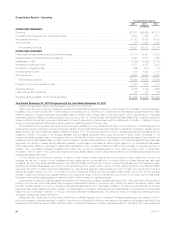

The table below illustrates the impact that a range of reasonably likely variances in credit spreads would have on our consolidated balance sheet,

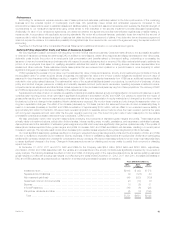

excluding the effect of income tax, related to the embedded derivative valuation on certain variable annuity products measured at estimated fair value.

However, these estimated effects do not take into account potential changes in other variables, such as equity price levels and market volatility, that can

also contribute significantly to changes in carrying values. Therefore, the table does not necessarily reflect the ultimate impact on the consolidated

financial statements under the credit spread variance scenarios presented below.

In determining the ranges, we have considered current market conditions, as well as the market level of spreads that can reasonably be anticipated

over the near term. The ranges do not reflect extreme market conditions experienced during the recent financial crisis as we do not consider those to be

reasonably likely events in the near future.

Changes in Balance Sheet

Carrying Value

At December 31, 2012

Policyholder

Account Balances DAC and

VOBA

(In millions)

100% increase in our credit spread ................................................... $2,368 $232

As reported ...................................................................... $3,308 $313

50% decrease in our credit spread ................................................... $3,910 $379

The accounting for derivatives is complex and interpretations of accounting standards continue to evolve in practice. If it is determined that hedge

accounting designations were not appropriately applied, reported net income could be materially affected. Assessments of hedge effectiveness and

measurements of ineffectiveness of hedging relationships are also subject to interpretations and estimations and different interpretations or estimates

may have a material effect on the amount reported in net income.

Variable annuities with guaranteed minimum benefits may be more costly than expected in volatile or declining equity markets. Market conditions

including, but not limited to, changes in interest rates, equity indices, market volatility and foreign currency exchange rates, changes in our

nonperformance risk, variations in actuarial assumptions regarding policyholder behavior, mortality and risk margins related to non-capital market inputs,

may result in significant fluctuations in the estimated fair value of the guarantees that could materially affect net income. If interpretations change, there is

a risk that features previously not bifurcated may require bifurcation and reporting at estimated fair value in the consolidated financial statements and

respective changes in estimated fair value could materially affect net income.

MetLife, Inc. 15