MetLife 2012 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2012 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

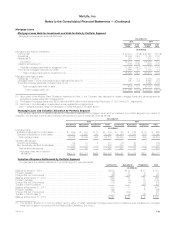

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

Factors Impacting Amortization

Separate account rates of return on variable universal life contracts and variable deferred annuity contracts affect in-force account balances on such

contracts each reporting period which can result in significant fluctuations in amortization of DAC and VOBA. Returns that are higher than the

Company’s long-term expectation produce higher account balances, which increases the Company’s future fee expectations and decreases future

benefit payment expectations on minimum death and living benefit guarantees, resulting in higher expected future gross profits. The opposite result

occurs when returns are lower than the Company’s long-term expectation. The Company’s practice to determine the impact of gross profits resulting

from returns on separate accounts assumes that long-term appreciation in equity markets is not changed by short-term market fluctuations, but is only

changed when sustained interim deviations are expected. The Company monitors these events and only changes the assumption when its long-term

expectation changes.

The Company also periodically reviews other long-term assumptions underlying the projections of estimated gross margins and profits. These

assumptions primarily relate to investment returns, policyholder dividend scales, interest crediting rates, mortality, persistency and expensesto

administer business. Management annually updates assumptions used in the calculation of estimated gross margins and profits which may have

significantly changed. If the update of assumptions causes expected future gross margins and profits to increase, DAC and VOBA amortization will

decrease, resulting in a current period increase to earnings. The opposite result occurs when the assumption update causes expected future gross

margins and profits to decrease.

Periodically, the Company modifies product benefits, features, rights or coverages that occur by the exchange of a contract for a new contract, or by

amendment, endorsement, or rider to a contract, or by election or coverage within a contract. If such modification, referred to as an internal

replacement, substantially changes the contract, the associated DAC or VOBA is written off immediately through income and any new deferrable costs

associated with the replacement contract are deferred. If the modification does not substantially change the contract, the DAC or VOBA amortization on

the original contract will continue and any acquisition costs associated with the related modification are expensed.

Amortization of DAC and VOBA is attributed to both investment gains and losses and to other expenses for the amount of gross margins or profits

originating from transactions other than investment gains and losses. Unrealized investment gains and losses represent the amount of DAC and VOBA

that would have been amortized if such gains and losses had been recognized.

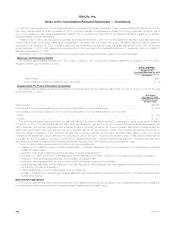

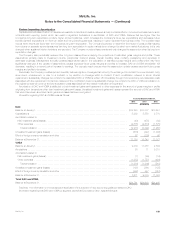

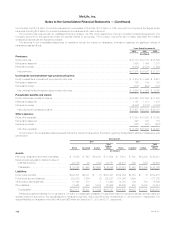

Information regarding DAC and VOBA was as follows:

Years Ended December 31,

2012 2011 2010

(In millions)

DAC

Balance at January 1, ........................................................................... $15,240 $13,377 $13,551

Capitalizations ................................................................................ 5,289 5,558 2,770

Amortization related to:

Net investment gains (losses) ................................................................... (40) (478) (92)

Other expenses ............................................................................. (2,875) (2,614) (1,875)

Total amortization .......................................................................... (2,915) (3,092) (1,967)

Unrealized investment gains (losses) ............................................................... (516) (427) (1,043)

Effect of foreign currency translation and other ....................................................... 52 (176) 66

Balance at December 31, ....................................................................... 17,150 15,240 13,377

VOBA

Balance at January 1, ........................................................................... 9,379 11,088 2,864

Acquisitions .................................................................................. 55 11 9,210

Amortization related to:

Net investment gains (losses) ................................................................... (1) (49) (16)

Other expenses ............................................................................. (1,283) (1,757) (494)

Total amortization .......................................................................... (1,284) (1,806) (510)

Unrealized investment gains (losses) ............................................................... (197) (361) (125)

Effect of foreign currency translation and other ....................................................... (342) 447 (351)

Balance at December 31, ....................................................................... 7,611 9,379 11,088

Total DAC and VOBA

Balance at December 31, ....................................................................... $24,761 $24,619 $24,465

See Note 1 for information on the retrospective application of the adoption of new accounting guidance related to DAC.

Information regarding total DAC and VOBA by segment, as well as Corporate & Other, was as follows at:

MetLife, Inc. 109