MetLife 2012 Annual Report Download - page 183

Download and view the complete annual report

Please find page 183 of the 2012 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

|

|

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

billion and $4.5 billion for the years ended December 31, 2012 and 2011, respectively. MRV’s RBC would have triggered a regulatory event without the

use of the state prescribed practice. The statutory net income (loss) of MetLife, Inc.’s domestic captive life reinsurance subsidiaries was ($154) million,

($130) million and ($621) million for the years ended December 2012, 2011 and 2010, respectively, and the statutory capital and surplus, including the

aforementioned prescribed practice, was $4.2 billion and $3.4 billion at December 31, 2012 and 2011, respectively.

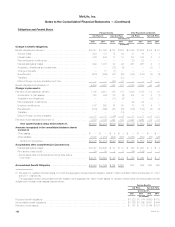

Dividend Restrictions

Insurance Operations

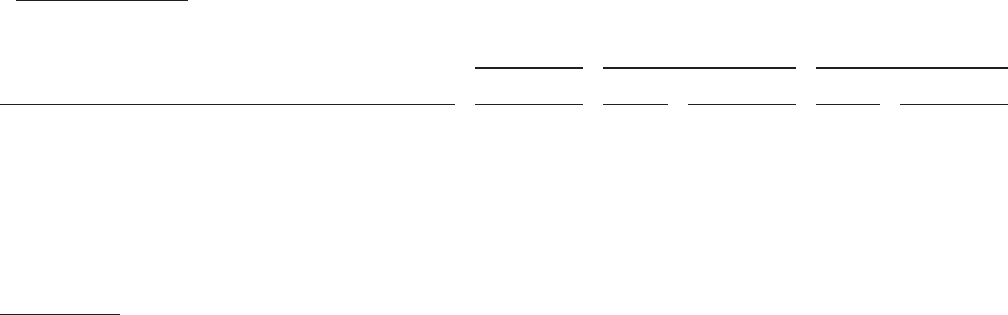

The table below sets forth the dividends permitted to be paid by the respective insurance subsidiary without insurance regulatory approval and the

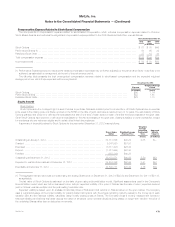

respective dividends paid:

2013 2012 2011

Company Permitted w/o

Approval (1) Paid (2) Permitted w/o

Approval (3) Paid (2) Permitted w/o

Approval (3)

(In millions)

Metropolitan Life Insurance Company ........................ $1,428 $ 1,023 $1,350 $ 1,321 (4) $1,321

American Life Insurance Company ........................... $ 523 $ 1,300 (5) $ 168 $ 661 $ 661

MetLife Insurance Company of Connecticut ................... $1,330 $ 706 (6) $ 504 $ 517 $ 517

Metropolitan Property and Casualty Insurance Company .......... $ 74 $ 100 $ — $ 30 $ —

Metropolitan Tower Life Insurance Company ................... $ 77 $ 82 $ 82 $ 80 $ 80

MetLife Investors Insurance Company ........................ $ 129 $ 18 $ 18 $ — $ —

Delaware American Life Insurance Company ................... $ 7 $ — $ 12 $ — $ —

(1) Reflects dividend amounts that may be paid during 2013 without prior regulatory approval. However, because dividend tests may be based on

dividends previously paid over rolling 12-month periods, if paid before a specified date during 2013, some or all of such dividends may require

regulatory approval.

(2) Reflects all amounts paid, including those requiring regulatory approval.

(3) Reflects dividend amounts that could have been paid during the relevant year without prior regulatory approval.

(4) Includes securities transferred to MetLife, Inc. of $170 million during the year ended December 31, 2011.

(5) During May 2012, American Life received regulatory approval to pay an extraordinary dividend for an amount up to the funds remitted in connection

with the restructuring of American Life’s business in Japan. Subsequently, $1.5 billion was remitted to American Life. See Note 19. Of this approved

amount, $1.3 billion was paid to MetLife, Inc. as an extraordinary dividend.

(6) During June 2012, MICC distributed shares of an affiliate to its stockholders as an in-kind extraordinary dividend of $202 million as calculated ona

statutory basis. Regulatory approval for this extraordinary dividend was obtained due to the timing of payment. During December 2012, MICC paid a

dividend to its stockholders in the amount of $504 million, which represented its ordinary dividend capacity at year-end 2012. Due to the June 2012

in-kind dividend, a portion of this was extraordinary and regulatory approval was obtained.

Under New York State Insurance Law, MLIC is permitted, without prior insurance regulatory clearance, to pay stockholder dividends to MetLife, Inc.

as long as the aggregate amount of all such dividends in any calendar year does not exceed the lesser of: (i) 10% of its surplus to policyholders as of

the end of the immediately preceding calendar year or (ii) its statutory net gain from operations for the immediately preceding calendar year (excluding

realized capital gains). MLIC will be permitted to pay a dividend to MetLife, Inc. in excess of the lesser of such two amounts only if it files notice of its

intention to declare such a dividend and the amount thereof with the New York Superintendent of Insurance (the “Superintendent”) and the

Superintendent either approves the distribution of the dividend or does not disapprove the dividend within 30 days of its filing. Under New York State

Insurance Law, the Superintendent has broad discretion in determining whether the financial condition of a stock life insurance company would support

the payment of such dividends to its stockholders.

Under Delaware State Insurance Law, each of American Life, DelAm and Metropolitan Tower Life Insurance Company (“MTL”) is permitted, without

prior insurance regulatory clearance, to pay a stockholder dividend to MetLife, Inc. as long as the amount of the dividend, when aggregated with all

other dividends in the preceding 12 months, does not exceed the greater of: (i) 10% of its surplus to policyholders as of the end of the immediately

preceding calendar year; or (ii) its net statutory gain from operations for the immediately preceding calendar year (excluding realized capital gains). Each

of American Life, DelAm and MTL will be permitted to pay a dividend to MetLife, Inc. in excess of the greater of such two amounts only if it files notice of

the declaration of such a dividend and the amount thereof with the Delaware Commissioner of Insurance (the “Delaware Commissioner”) and the

Delaware Commissioner either approves the distribution of the dividend or does not disapprove the distribution within 30 days of its filing. In addition,

any dividend that exceeds earned surplus (defined as “unassigned funds (surplus)”) as of the immediately preceding calendar year requires insurance

regulatory approval. Under Delaware State Insurance Law, the Delaware Commissioner has broad discretion in determining whether the financial

condition of a stock life insurance company would support the payment of such dividends to its stockholders.

Under Connecticut State Insurance Law, MICC is permitted, without prior insurance regulatory clearance, to pay stockholder dividends to its

stockholders as long as the amount of such dividends, when aggregated with all other dividends in the preceding 12 months, does not exceed the

greater of: (i) 10% of its surplus to policyholders as of the end of the immediately preceding calendar year; or (ii) its statutory net gain from operations for

the immediately preceding calendar year. MICC will be permitted to pay a dividend in excess of the greater of such two amounts only if it files notice of

its declaration of such a dividend and the amount thereof with the Connecticut Commissioner of Insurance (the “Connecticut Commissioner”) and the

Connecticut Commissioner either approves the distribution of the dividend or does not disapprove the payment within 30 days after notice. In addition,

any dividend that exceeds earned surplus (defined as “unassigned funds (surplus)”, reduced by 25% of unrealized appreciation in value or revaluationof

MetLife, Inc. 177