MetLife 2011 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2011 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

|

|

standards. In October 2011, the FSOC issued a notice of proposed rulemaking outlining the process it will follow and the criteria it will use to assess

whether a non-bank financial company should be so subject. If MetLife, Inc. meets the quantitative thresholds set forth in the proposal, the FSOC will

continue with a further analysis using qualitative and quantitative factors. For further information, see “— Industry Trends.”

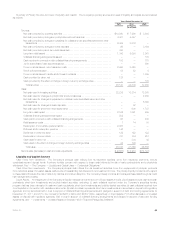

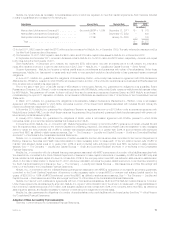

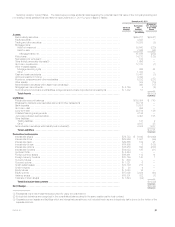

The following table contains the RBC ratios and the regulatory requirements for MetLife, Inc., as a bank holding company, and MetLife Bank:

MetLife, Inc.

RBC Ratios — Bank Holding Company

December 31, Regulatory

Requirements

Minimum

Regulatory

Requirements

“Well Capitalized”2011 2010

Total RBC Ratio ................................................. 10.25% 8.52% 8.00% 10.00%

Tier 1 RBC Ratio ................................................ 9.98% 8.21% 4.00% 6.00%

Tier 1 Leverage Ratio ............................................ 5.32% 5.11% 4.00% N/A

Tier 1 Common Ratio ............................................ 9.39% 6.97% N/A N/A

MetLife Bank

RBC Ratios — Bank

December 31, Regulatory

Requirements

Minimum

Regulatory

Requirements

“Well Capitalized”2011 2010

Total RBC Ratio ................................................ 12.55% 15.00% 8.00% 10.00%

Tier 1 RBC Ratio ............................................... 12.54% 14.16% 4.00% 6.00%

Tier 1 Leverage Ratio ........................................... 5.27% 7.14% 4.00% 5.00%

Tier 1 Common Ratio ........................................... 9.72% 13.56% N/A N/A

Summary of Primary Sources and Uses of Liquidity and Capital. For information regarding the primary sources and uses of MetLife, Inc.’s liquidity

and capital, see “— The Company — Capital — Summary of Primary Sources and Uses of Liquidity and Capital.”

Liquidity and Capital

Liquidity and capital are managed to preserve stable, reliable and cost-effective sources of cash to meet all current and future financial obligations

and are provided by a variety of sources, including a portfolio of liquid assets, a diversified mix of short- and long-term funding sources from the

wholesale financial markets and the ability to borrow through credit and committed facilities. MetLife, Inc. is an active participant in the global financial

markets through which it obtains a significant amount of funding. These markets, which serve as cost-effective sources of funds, are critical

components of MetLife, Inc.’s liquidity and capital management. Decisions to access these markets are based upon relative costs, prospective views of

balance sheet growth and a targeted liquidity profile and capital structure. A disruption in the financial markets could limit MetLife, Inc.’s accessto

liquidity.

MetLife, Inc.’s ability to maintain regular access to competitively priced wholesale funds is fostered by its current credit ratings from the major credit

rating agencies. We view our capital ratios, credit quality, stable and diverse earnings streams, diversity of liquidity sources and our liquidity monitoring

procedures as critical to retaining such credit ratings. See “— The Company — Capital — Rating Agencies.”

Liquidity is monitored through the use of internal liquidity risk metrics, including the composition and level of the liquid asset portfolio, timing

differences in short-term cash flow obligations, access to the financial markets for capital and debt transactions and exposure to contingent draws on

MetLife, Inc.’s liquidity.

Liquidity and Capital Sources

Dividends from Subsidiaries. MetLife, Inc. relies in part on dividends from its subsidiaries to meet its cash requirements. MetLife, Inc.’s insurance

subsidiaries are subject to regulatory restrictions on the payment of dividends imposed by the regulators of their respective domiciles. The dividend

limitation for U.S. insurance subsidiaries is generally based on the surplus to policyholders at the end of the immediately preceding calendar year and

statutory net gain from operations for the immediately preceding calendar year. Statutory accounting practices, as prescribed by insurance regulators of

various states in which the Company conducts business, differ in certain respects from accounting principles used in financial statements prepared in

conformity with GAAP. The significant differences relate to the treatment of DAC, certain deferred income tax, required investment liabilities, statutory

reserve calculation assumptions, goodwill and surplus notes.

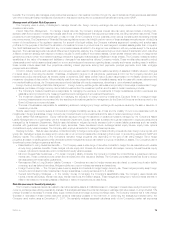

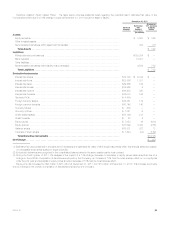

The table below sets forth the dividends permitted to be paid by the respective insurance subsidiary without insurance regulatory approval and the

respective dividends paid:

2012 2011 2010 2009

Company

Permitted

w/o

Approval(1) Paid(2)

Permitted

w/o

Approval(3) Paid(2)

Permitted

w/o

Approval(3) Paid(2)

Permitted

w/o

Approval(3)

(In millions)

Metropolitan Life Insurance Company ........................... $1,350 $1,321(4) $1,321 $631(4) $1,262 $ — $552

American Life Insurance Company .............................. $ 168(5) $ 661 $ 661(5) $ —(6) $ 511(5) $N/A $N/A

MetLife Insurance Company of Connecticut ...................... $ 504 $ 517 $ 517 $330 $ 659 $ — $714

Metropolitan Property and Casualty Insurance Company ............. $ — $ 30 $ — $260 $ — $300 $ 9

Metropolitan Tower Life Insurance Company ...................... $ 82 $ 80 $ 80 $569(7) $ 93 $ — $ 88

MetLife Investors Insurance Company ........................... $ 18 $ — $ — $ — $ — $ — $ —

Delaware American Life Insurance Company ...................... $ 12 $ — $ — $ — $ — $N/A $N/A

(1) Reflects dividend amounts that may be paid during 2012 without prior regulatory approval. However, because dividend tests may be based on

74 MetLife, Inc.