MetLife 2011 Annual Report Download - page 163

Download and view the complete annual report

Please find page 163 of the 2011 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

|

|

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

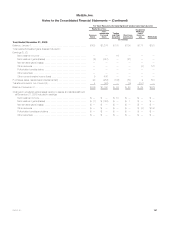

Option-based — Significant unobservable inputs may include the extrapolation beyond observable limits of dividend yield curves, equity volatility and

unobservable correlations between model inputs. Certain of these derivatives are valued based on independent non-binding broker quotations.

Direct and Assumed Guaranteed Minimum Benefits

These embedded derivatives are principally valued using an income approach. Valuations are based on option pricing techniques, which utilize

significant inputs that may include swap yield curve, currency exchange rates and implied volatilities. These embedded derivatives result in Level 3

classification because one or more of the significant inputs are not observable in the market or cannot be derived principally from, or corroborated by,

observable market data. Significant unobservable inputs generally include: the extrapolation beyond observable limits of the swap yield curve and

implied volatilities, actuarial assumptions for policyholder behavior and mortality and the potential variability in policyholder behavior and mortality,

nonperformance risk and cost of capital for purposes of calculating the risk margin.

Reinsurance Ceded on Certain Guaranteed Minimum Benefits

These embedded derivatives are principally valued using an income approach. The valuation techniques and significant market standard

unobservable inputs used in their valuation are similar to those previously described under “Direct and Assumed Guaranteed Minimum Benefits” and

also include counterparty credit spreads.

Embedded Derivatives Within Funds Withheld Related to Certain Ceded Reinsurance

These embedded derivatives are principally valued using an income approach. Valuations are based on present value techniques, which utilize

significant inputs that may include the swap yield curve and the fair value of assets within the reference portfolio. These embedded derivatives result in

Level 3 classification because one or more of the significant inputs are not observable in the market or cannot be derived principally from, or

corroborated by, observable market data. Significant unobservable inputs generally include: the fair value of certain assets within the reference portfolio

which are not observable in the market and cannot be derived principally from, or corroborated by, observable market data.

Separate Account Assets

These assets are comprised of investments that are similar in nature to the fixed maturity securities, equity securities and derivative assets referred to

above. Separate account assets within this level also include mortgage loans and other limited partnership interests. The estimated fair value of

mortgage loans is determined by discounting expected future cash flows, using current interest rates for similar loans with similar credit risk. Other

limited partnership interests are valued giving consideration to the value of the underlying holdings of the partnerships and by applying a premium or

discount, if appropriate, for factors such as liquidity, bid/ask spreads, the performance record of the fund manager or other relevant variables which may

impact the exit value of the particular partnership interest.

Long-term Debt of CSEs

The estimated fair value of the long-term debt of the Company’s CSEs are priced principally through independent broker quotations or market

standard valuation methodologies using inputs that are not market observable or cannot be derived from or corroborated by observable market data.

Liability Related to Securitized Reverse Residential Mortgage Loans

The estimated fair value of the liability related to securitized reverse residential mortgage loans is based on quoted prices when traded as assets in

less active markets or, if not available, based on market standard valuation methodologies using unobservable inputs, consistent with the Company’s

methods and assumptions used to estimate the fair value of comparable financial instruments.

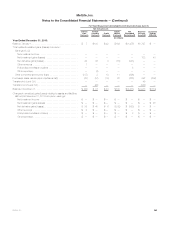

Transfers between Levels 1 and 2:

During the years ended December 31, 2011 and 2010, transfers between Levels 1 and 2 were not significant.

Transfers into or out of Level 3:

Overall, transfers into and/or out of Level 3 are attributable to a change in the observability of inputs. Assets and liabilities are transferred into Level 3

when a significant input cannot be corroborated with market observable data. This occurs when market activity decreases significantly and underlying

inputs cannot be observed, current prices are not available, and/or when there are significant variances in quoted prices, thereby affecting transparency.

Assets and liabilities are transferred out of Level 3 when circumstances change such that a significant input can be corroborated with market observable

data. This may be due to a significant increase in market activity, a specific event, or one or more significant input(s) becoming observable. Transfers

into and/or out of any level are assumed to occur at the beginning of the period. Significant transfers into and/or out of Level 3 assets and liabilities for

the years ended December 31, 2011 and 2010 are summarized below.

Transfers into Level 3 were due primarily to a lack of trading activity, decreased liquidity and credit ratings downgrades (e.g., from investment grade

to below investment grade), which have resulted in decreased transparency of valuations and an increased use of broker quotations and unobservable

inputs to determine estimated fair value.

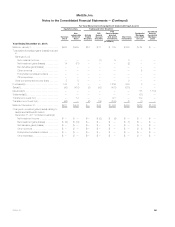

During the year ended December 31, 2011, transfers into Level 3 for fixed maturity securities of $599 million and for separate account assets of

$19 million, were principally comprised of certain U.S. and foreign corporate securities and foreign government securities. During the year ended

December 31, 2010, transfers into Level 3 for fixed maturity securities of $1.7 billion and for separate account assets of $46 million were principally

comprised of certain U.S. and foreign corporate securities and CMBS.

Transfers out of Level 3 resulted primarily from increased transparency of both new issuances that subsequent to issuance and establishment of

trading activity, became priced by independent pricing services and existing issuances that, over time, the Company was able to obtain pricing from, or

corroborate pricing received from, independent pricing services with observable inputs, or increases in market activity and upgraded credit ratings. With

respect to derivatives, transfers out of Level 3 resulted primarily from increased transparency related to the observable portion of the equity volatility

surface.

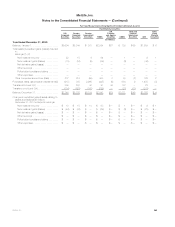

During the year ended December 31, 2011, transfers out of Level 3 for fixed maturity securities of $6.7 billion and for separate account assets of

$257 million, were principally comprised of certain ABS, foreign government securities, U.S. and foreign corporate securities, RMBS and CMBS. During

the year ended December 31, 2011, transfers out of Level 3 for derivatives of $75 million were principally comprised of equity options. During the year

ended December 31, 2010, transfers out of Level 3 for fixed maturity securities of $1.7 billion and for separate account assets of $234 million were

principally comprised of certain U.S. and foreign corporate securities, RMBS and ABS.

MetLife, Inc. 159