MetLife 2011 Annual Report Download - page 21

Download and view the complete annual report

Please find page 21 of the 2011 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

|

|

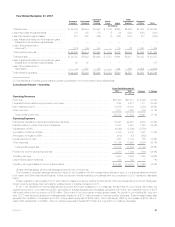

and other postretirement benefit plans that was 100 basis points higher or 100 basis points lower than the rates we assumed, the change in our net

periodic costs would have been a decrease of $75 million and an increase of $75 million, respectively. This considers only changes in our assumed

long-term rate of return given the level and mix of invested assets at the beginning of the year, without consideration of possible changes in any of the

other assumptions described above that could ultimately accompany any changes in our assumed long-term rate of return.

We determine our discount rates used to value the pension and postretirement obligations, based upon rates commensurate with current yields on

high quality corporate bonds. Given the amount of pension and postretirement obligations as of December 31, 2010, the beginning of the measurement

year, if we had assumed a discount rate for both our pension and postretirement benefit plans that was 100 basis points higher or 100 basis points

lower than the rates we assumed, the change in our net periodic costs would have been a decrease of $122 million and an increase of $142 million,

respectively. This considers only changes in our assumed discount rates without consideration of possible changes in any of the other assumptions

described above that could ultimately accompany any changes in our assumed discount rate. The assumptions used may differ materially from actual

results due to, among other factors, changing market and economic conditions and changes in participant demographics. These differences may have

a significant effect on the Company’s consolidated financial statements and liquidity.

See Note 17 of the Notes to the Consolidated Financial Statements for additional assumptions used in measuring liabilities relating to the Company’s

employee benefit plans.

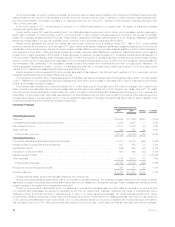

Litigation Contingencies

The Company is a party to a number of legal actions and is involved in a number of regulatory investigations. Given the inherent unpredictability of

these matters, it is difficult to estimate the impact on the Company’s financial position. Liabilities are established when it is probable that a loss has been

incurred and the amount of the loss can be reasonably estimated. Liabilities related to certain lawsuits, including the Company’s asbestos-related

liability, are especially difficult to estimate due to the limitation of available data and uncertainty regarding numerous variables that can affect liability

estimates. The data and variables that impact the assumptions used to estimate the Company’s asbestos-related liability include the number of future

claims, the cost to resolve claims, the disease mix and severity of disease in pending and future claims, the impact of the number of new claims filed in

a particular jurisdiction and variations in the law in the jurisdictions in which claims are filed, the possible impact of tort reform efforts, the willingness of

courts to allow plaintiffs to pursue claims against the Company when exposure to asbestos took place after the dangers of asbestos exposure were well

known, and the impact of any possible future adverse verdicts and their amounts. On a quarterly and annual basis, the Company reviews relevant

information with respect to liabilities for litigation, regulatory investigations and litigation-related contingencies to be reflected in the Company’s

consolidated financial statements. It is possible that an adverse outcome in certain of the Company’s litigation and regulatory investigations, including

asbestos-related cases, or the use of different assumptions in the determination of amounts recorded could have a material effect upon the Company’s

consolidated net income or cash flows in particular quarterly or annual periods.

See Note 16 of the Notes to the Consolidated Financial Statements for additional information regarding the Company’s assessment of litigation

contingencies.

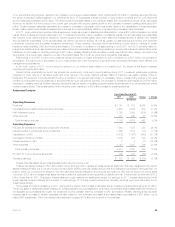

Economic Capital

Economic capital is an internally developed risk capital model, the purpose of which is to measure the risk in the business and to provide a basis

upon which capital is deployed. The economic capital model accounts for the unique and specific nature of the risks inherent in the Company’s

business.

Effective January 1, 2011, the Company updated its economic capital model to align segment allocated equity with emerging standards and

consistent risk principles. Such changes to the Company’s economic capital model are applied prospectively. Segment net investment income is also

credited or charged based on the level of allocated equity; however, changes in allocated equity do not impact the Company’s consolidated net

investment income, operating earnings or income (loss) from continuing operations, net of income tax.

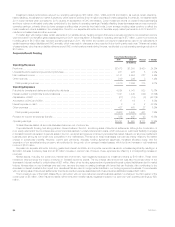

Acquisitions and Dispositions

See Note 2 of the Notes to the Consolidated Financial Statements.

During 2011, a local operating subsidiary of American Life closed on the purchase of a 99.86% stake in a Turkish life insurance and pension

company and at the same time entered into an exclusive 15-year distribution arrangement with the seller to distribute the company’s products in Turkey.

Also in 2011, American Life agreed to sell certain closed blocks of business in the United Kingdom (“U.K.”). Finally, in 2011, Punjab National Bank

(“PNB”) agreed to acquire a 30% stake in MetLife India Insurance Company Limited (“MetLife India”) and to enter into a separate exclusive 10-year

distribution arrangement to sell MetLife India’s products through PNB’s branch network. PNB’s acquisition of the 30% stake in MetLife India is subject to,

among other things, regulatory approval and final agreements among PNB and the existing shareholders of MetLife India. If such agreements are not

obtained, or the transaction does not receive regulatory approval, PNB may request to amend or cancel the distribution agreement.

In addition, in 2012, local operating subsidiaries of MetLife, Inc. agreed to acquire, from members of the Aviva Plc group (“Aviva”), Aviva’s life

insurance business in the Czech Republic and Hungary and Aviva’s life insurance and pensions business in Romania. The closing of each of these

transactions is subject to regulatory and other approvals.

Recent Development

In January 2012, MetLife submitted to the Federal Reserve a comprehensive capital plan, as mandated by the Federal Reserve’s capital plans rule,

and additional information required by the 2012 Comprehensive Capital Analysis and Review of the 19 largest bank holding companies (“CCAR”). The

capital plan proposed, among other things, $2 billion of stock repurchases and an increase in the annual dividend from $0.74 per share to $1.10 per

share. In March 2012, the Federal Reserve informed MetLife that it objected to MetLife’s proposed capital plan. As a result, MetLife is currently not able

to engage in share repurchases or to pay an annual common stock dividend of more than $0.74 per share. See “Business.”

MetLife, Inc. 17