MetLife 2011 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2011 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

|

|

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

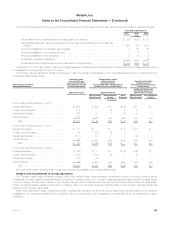

Credit Risk on Freestanding Derivatives

The Company may be exposed to credit-related losses in the event of nonperformance by counterparties to derivative financial instruments.

Generally, the current credit exposure of the Company’s derivative contracts is limited to the net positive estimated fair value of derivative contracts at

the reporting date after taking into consideration the existence of netting agreements and any collateral received pursuant to credit support annexes.

The Company manages its credit risk related to OTC derivatives by entering into transactions with creditworthy counterparties, maintaining collateral

arrangements and through the use of master agreements that provide for a single net payment to be made by one counterparty to another at each due

date and upon termination. Because exchange-traded futures and options are effected through regulated exchanges, and positions are marked to

market on a daily basis, the Company has minimal exposure to credit-related losses in the event of nonperformance by counterparties to such derivative

instruments. See Note 5 for a description of the impact of credit risk on the valuation of derivative instruments.

The Company enters into various collateral arrangements which require both the pledging and accepting of collateral in connection with its OTC

derivative instruments. At December 31, 2011 and 2010, the Company was obligated to return cash collateral under its control of $9.5 billion and

$2.6 billion, respectively. This cash collateral is included in cash and cash equivalents or in short-term investments and the obligation to return itis

included in payables for collateral under securities loaned and other transactions in the consolidated balance sheets. At December 31, 2011 and 2010,

the Company had received collateral consisting of various securities with a fair market value of $2.5 billion and $984 million, respectively, which were

held in separate custodial accounts. Subject to certain constraints, the Company is permitted by contract to sell or repledge this collateral, but at

December 31, 2011, none of the collateral had been sold or repledged.

The Company’s collateral arrangements for its OTC derivatives generally require the counterparty in a net liability position, after considering the effect

of netting agreements, to pledge collateral when the fair value of that counterparty’s derivatives reaches a pre-determined threshold. Certain of these

arrangements also include credit-contingent provisions that provide for a reduction of these thresholds (on a sliding scale that converges toward zero) in

the event of downgrades in the credit ratings of the Company and/or the counterparty. In addition, certain of the Company’s netting agreements for

derivative instruments contain provisions that require the Company to maintain a specific investment grade credit rating from at least one of the major

credit rating agencies. If the Company’s credit ratings were to fall below that specific investment grade credit rating, it would be in violation of these

provisions, and the counterparties to the derivative instruments could request immediate payment or demand immediate and ongoing full overnight

collateralization on derivative instruments that are in a net liability position after considering the effect of netting agreements.

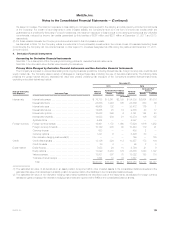

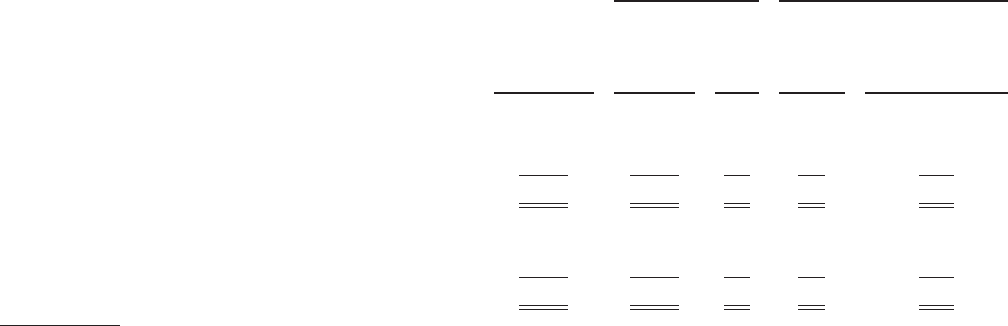

The following table presents the estimated fair value of the Company’s OTC derivatives that are in a net liability position after considering the effect of

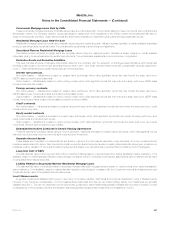

netting agreements, together with the estimated fair value and balance sheet location of the collateral pledged. The table also presents the incremental

collateral that the Company would be required to provide if there was a one notch downgrade in the Company’s credit rating at the reporting date or if

the Company’s credit rating sustained a downgrade to a level that triggered full overnight collateralization or termination of the derivative position at the

reporting date. Derivatives that are not subject to collateral agreements are not included in the scope of this table.

Estimated

Fair Value(1) of

Derivatives in Net

Liability Position

Estimated

Fair Value of

Collateral

Provided: Fair Value of Incremental Collateral

Provided Upon:

Fixed Maturity

Securities(2) Cash(3)

One Notch

Downgrade

in the

Company’s

Credit

Rating

Downgrade in the

Company’s Credit Rating

to a Level that Triggers

Full Overnight

Collateralization or

Termination of

the Derivative Position

(In millions)

December 31, 2011:

Derivatives subject to credit-contingent provisions ................. $ 447 $ 405 $ 4 $48 $104

Derivatives not subject to credit-contingent provisions .............. 28 11 4 — —

Total .................................................. $ 475 $ 416 $ 8 $48 $104

December 31, 2010:

Derivatives subject to credit-contingent provisions ................. $1,167 $1,024 $ — $99 $231

Derivatives not subject to credit-contingent provisions .............. 22 — 43 — —

Total .................................................. $1,189 $1,024 $43 $99 $231

(1) After taking into consideration the existence of netting agreements.

(2) Included in fixed maturity securities in the consolidated balance sheets. Subject to certain constraints, the counterparties are permitted by contract to

sell or repledge this collateral.

(3) Included in premiums, reinsurance and other receivables in the consolidated balance sheets.

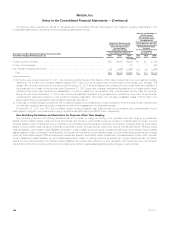

Without considering the effect of netting agreements, the estimated fair value of the Company’s OTC derivatives with credit-contingent provisions

that were in a gross liability position at December 31, 2011 was $777 million. At December 31, 2011, the Company provided collateral of $409 million

in connection with these derivatives. In the unlikely event that both: (i) the Company’s credit rating was downgraded to a level that triggers full overnight

collateralization or termination of all derivative positions; and (ii) the Company’s netting agreements were deemed to be legally unenforceable, then the

additional collateral that the Company would be required to provide to its counterparties in connection with its derivatives in a gross liability position at

December 31, 2011 would be $368 million. This amount does not consider gross derivative assets of $330 million for which the Company has the

contractual right of offset.

MetLife, Inc. 149