MetLife 2011 Annual Report Download - page 14

Download and view the complete annual report

Please find page 14 of the 2011 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

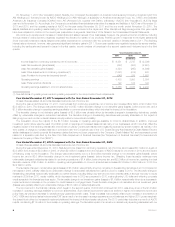

|

|

Competitive Pressures. The life insurance industry remains highly competitive. The product development and product life-cycles have shortened in

many product segments, leading to more intense competition with respect to product features. Larger companies have the ability to invest in brand

equity, product development, technology and risk management, which are among the fundamentals for sustained profitable growth in the life insurance

industry. In addition, several of the industry’s products can be quite homogeneous and subject to intense price competition. Sufficient scale, financial

strength and financial flexibility are becoming prerequisites for sustainable growth in the life insurance industry. Larger market participants tend to have

the capacity to invest in additional distribution capability and the information technology needed to offer the superior customer service demanded by an

increasingly sophisticated industry client base. We believe that the turbulence in financial markets that began in the second half of 2007, its impacton

the capital position of many competitors, and subsequent actions by regulators and rating agencies have highlighted financial strength as a significant

differentiator from the perspective of customers and certain distributors. In addition, the financial market turbulence and the economic recession have

led many companies in our industry to re-examine the pricing and features of the products they offer and may lead to consolidation in the life insurance

industry.

Regulatory Changes. The U.S. life insurance industry is regulated primarily at the state level, with some products and services also subject to

Federal regulation. As life insurers introduce new and often more complex products, regulators refine capital requirements and introduce new reserving

standards for the life insurance industry. Regulations recently adopted or currently under review can potentially impact the statutory reserve and capital

requirements of the industry. In addition, regulators have undertaken market and sales practices reviews of several markets or products, including

equity-indexed annuities, variable annuities and group products. The regulation of the financial services industry in the U.S. and internationally has

received renewed scrutiny as a result of the disruptions in the financial markets. Significant regulatory reforms have been recently adopted and additional

reforms proposed, and these or other reforms could be implemented. See “Business — U.S. Regulation,” “Business – International Regulation,” “Risk

Factors — Our Insurance, Brokerage and Banking Businesses Are Highly Regulated, and Changes in Regulation and in Supervisory and Enforcement

Policies May Reduce Our Profitability and Limit Our Growth” and “Risk Factors — Changes in U.S. Federal and State Securities Laws and Regulations,

and State Insurance Regulations Regarding Suitability of Annuity Product Sales, May Affect Our Operations and Our Profitability” in the 2011 Form 10-K.

The Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank”), which was signed by President Obama in July 2010, effected the

most far-reaching overhaul of financial regulation in the U.S. in decades. The full impact of Dodd-Frank on us will depend on the numerous rulemaking

initiatives required or permitted by Dodd-Frank which are scheduled to be completed over the next few years. See “Business — U.S. Regulation —

Dodd-Frank and Other Legislative and Regulatory Developments” and “Risk Factors — Various Aspects of Dodd-Frank Could Impact Our Business

Operations, Capital Requirements and Profitability and Limit Our Growth” in the 2011 Form 10-K.

As a federally chartered national banking association, MetLife Bank is subject to a wide variety of banking laws, regulations and guidelines, as is

MetLife, Inc., as a bank holding company. See “Business – U.S. Regulation – Banking Regulation” and “Business – U.S. Regulation – Financial Holding

Company Regulation” in the 2011 Form 10-K. In December 2011, MetLife Bank and MetLife, Inc. entered into a definitive agreement to sell most of the

depository business of MetLife Bank. In January 2012, MetLife, Inc. announced it is exiting the business of originating forward residential mortgages.

Once MetLife Bank has completely exited its depository business, MetLife, Inc. plans to terminate MetLife Bank’s FDIC insurance, putting MetLife, Inc. in

a position to be able to deregister as a bank holding company. Upon completion of the foregoing, MetLife, Inc. will no longer be regulated as a bank

holding company or subject to enhanced supervision and prudential standards as a bank holding company with assets of $50 billion or more. However,

if, in the future, MetLife, Inc. is designated by the Financial Stability Oversight Council (“FSOC”) as a non-bank systemically important financial institution

(as discussed below), it could once again be subject to regulation by the Federal Reserve and enhanced supervision and prudential standards, such as

Regulation YY (as discussed below). In October 2011, the FSOC issued a notice of proposed rulemaking, outlining the process it will follow and the

criteria it will use to assess whether a non-bank financial company should be subject to enhanced supervision by the Federal Reserve as a non-bank

systemically important financial institution. If MetLife, Inc. meets the quantitative thresholds set forth in the proposal, the FSOC will continue with a further

analysis using qualitative and quantitative factors.

In December 2010, the Basel Committee on Banking Supervision (the “Basel Committee”) published its final rules for increased capital and liquidity

requirements (commonly referred to as “Basel III”) for bank holding companies, such as MetLife, Inc. Assuming these requirements are endorsed and

adopted by the U.S. banking regulators, they are to be phased in beginning January 1, 2013. It is possible that even more stringent capital and liquidity

requirements could be imposed under Basel III, Dodd-Frank and Regulation YY, as long as MetLife, Inc. remains a bank holding company or if, in the

future, it is designated by the FSOC as a non-bank systemically important financial institution. The Basel Committee has also published rules requiring a

capital surcharge for globally systemically important banks, which are to be phased in beginning January 2016 if they are endorsed and adopted by the

U.S. banking regulators. As currently proposed, this surcharge would not apply to global non-bank systemically important financial institutions. However,

international regulatory bodies are currently engaged in evaluating standards to identify such companies and to develop a regulatory regime that would

apply to them, which may include enhanced capital requirements or other measures. The ability of MetLife Bank and MetLife, Inc. to pay dividends,

repurchase common stock or other securities or engage in other transactions that could affect its capital or need for capital could be reduced by any

additional capital requirements that might be imposed as a result of the enactment of Dodd-Frank, Regulation YY and/or the endorsement and adoption

by the U.S. of Basel III and other regulatory initiatives. See “Risk Factors – Our Insurance, Brokerage and Banking Businesses Are Highly Regulated, and

Changes in Regulation and in Supervisory and Enforcement Policies May Reduce Our Profitability and Limit Our Growth” in the 2011 Form 10-K.

In April 2011, the Federal Reserve Board and the FDIC proposed a rule regarding the implementation of the Dodd-Frank requirement that (i) each

non-bank financial company designated by the FSOC for enhanced supervision by the Federal Reserve Board (a “non-bank systemically important

financial institution” or “non-bank SIFI”) and each bank holding company with assets of $50 billion or more report periodically to the Federal Reserve

Board, the FDIC and the FSOC the plan of such company for rapid and orderly resolution in the event of material financial distress or failure, and (ii) that

each such company report on the nature and extent of credit exposures of such company to significant bank holding companies and significant

non-bank financial companies and the nature and extent of credit exposures of significant bank holding companies and significant non-bank financial

companies to such covered company. In November 2011, the Federal Reserve Board and the FDIC adopted a final rule implementing the resolution

plan requirement, effective November 30, 2011, but deferred finalizing the credit exposure reporting requirement until a later date. If MetLife, Inc. remains

a bank holding company on July 1, 2012, or if, in the future, it is designated by the FSOC as a non-bank SIFI, it would be required to submit a resolution

plan. See “Business — U.S. Regulation — Dodd-Frank and Other Legislative and Regulatory Developments – Orderly Liquidation Authority” in the 2011

Form 10-K.

In December 2011, the Federal Reserve Board issued a release proposing the adoption of enhanced prudential standards required by Dodd-Frank

(“Regulation YY”). Regulation YY would apply to bank holding companies with assets of $50 billion or more and non-bank SIFIs. Regulation YY would

impose (i) enhanced risk-based capital (“RBC”) requirements, (ii) leverage limits, (iii) liquidity requirements, (iv) single counterparty exposure limits,

(v) governance requirements for risk management, (vi) stress test requirements, and (vii) special debt-to-equity limits for certain companies, and would

10 MetLife, Inc.