MetLife 2013 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

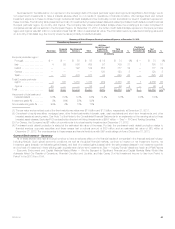

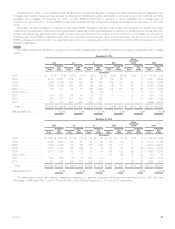

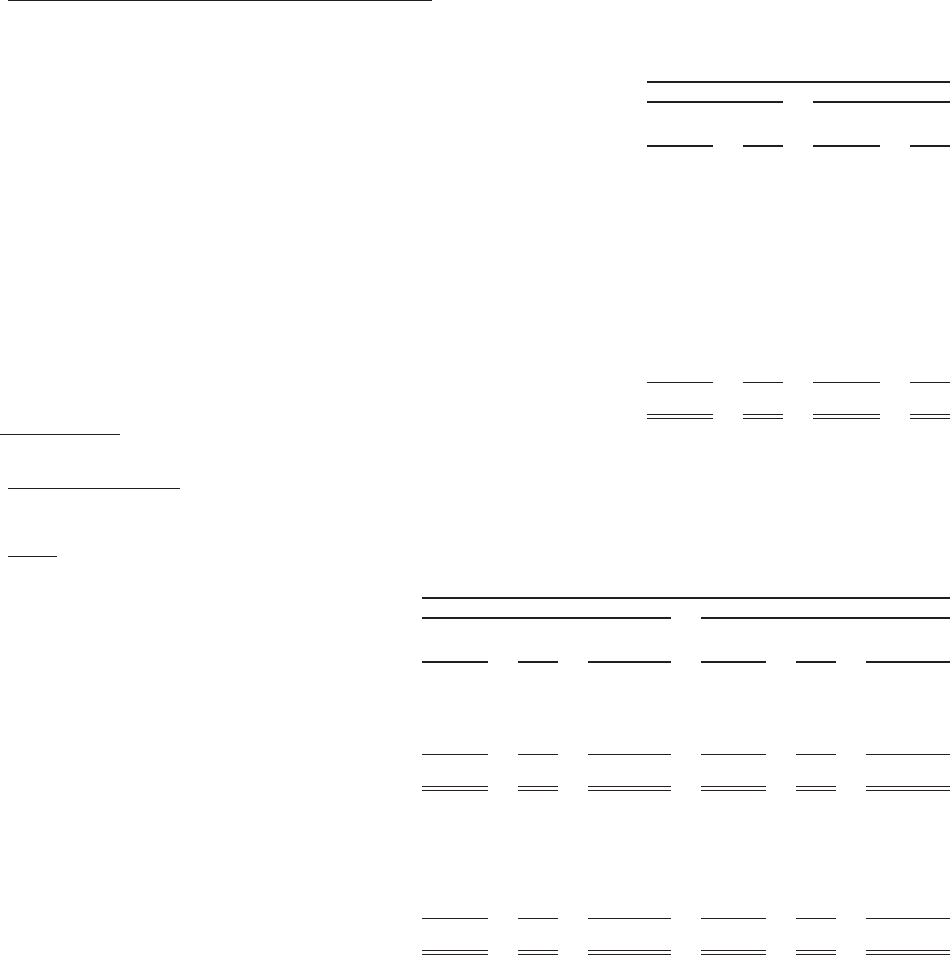

U.S. and Foreign Corporate Fixed Maturity Securities

We maintain a diversified portfolio of corporate fixed maturity securities across industries and issuers. This portfolio does not have any exposure to

any single issuer in excess of 1% of total investments and the top ten holdings comprise 2% of total investments at both December 31, 2013 and

2012. The tables below present our U.S. and foreign corporate securities holdings at:

December 31,

2013 2012

Estimated

Fair

Value %of

Total

Estimated

Fair

Value %of

Total

(In millions) (In millions)

Corporate fixed maturity securities — by sector:

Foreign corporate(1) ................................................ $ 63,152 37.2% $ 67,184 37.1%

U.S. corporate fixed maturity securities — by industry:

Consumer ........................................................ 27,953 16.5 29,852 16.4

Industrial ......................................................... 27,462 16.2 29,324 16.2

Finance .......................................................... 20,135 11.9 21,857 12.1

Utility ............................................................ 19,066 11.2 20,216 11.1

Communications ................................................... 8,074 4.8 9,084 5.0

Other ............................................................ 3,779 2.2 3,793 2.1

Total .......................................................... $169,621 100.0% $181,310 100.0%

(1) Includes both U.S. dollar and foreign denominated securities.

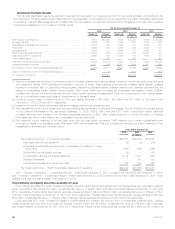

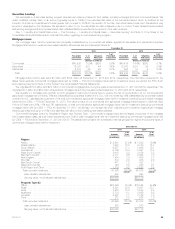

Structured Securities

We held $67.2 billion and $72.6 billion of structured securities, at estimated fair value, at December 31, 2013 and 2012, respectively, as

presented in the RMBS, CMBS and ABS sections below.

RMBS

The table below presents our RMBS holdings at:

December 31,

2013 2012

Estimated

Fair

Value %of

Total

Net

Unrealized

Gains (Losses)

Estimated

Fair

Value %of

Total

Net

Unrealized

Gains (Losses)

(In millions) (In millions) (In millions) (In millions)

By security type:

Collateralized mortgage obligations .......... $19,046 54.3% $705 $20,567 54.9% $ 889

Pass-through securities ................... 16,009 45.7 183 16,912 45.1 924

Total RMBS .......................... $35,055 100.0% $888 $37,479 100.0% $1,813

By risk profile:

Agency ............................... $23,686 67.6% $762 $26,369 70.4% $1,944

Prime ................................. 2,935 8.4 71 4,206 11.2 101

Alt-A .................................. 4,986 14.2 (25) 4,950 13.2 (154)

Sub-prime ............................. 3,448 9.8 80 1,954 5.2 (78)

Total RMBS .......................... $35,055 100.0% $888 $37,479 100.0% $1,813

Ratings profile:

Rated Aaa/AAA ......................... $24,764 70.6% $26,555 70.9%

Rated NAIC 1 ........................... $31,385 89.5% $32,377 86.4%

Collateralized mortgage obligations are a type of mortgage-backed security structured by dividing the cash flows of mortgages into separate pools

or tranches of risk that create multiple classes of bonds with varying maturities and priority of payments. Pass-through mortgage-backed securities are

a type of asset-backed security that are secured by a mortgage or collection of mortgages. The monthly mortgage payments from homeowners pass

from the originating bank through an intermediary, such as a government agency or investment bank, which collects the payments and, for a fee,

remits or passes these payments through to the holders of the pass-through securities.

The majority of our RMBS holdings were rated Aaa/AAA by Moody’s, S&P or Fitch; and were rated NAIC 1 by the NAIC at December 31, 2013 and

2012. Agency RMBS were guaranteed or otherwise supported by Federal National Mortgage Association, Federal Home Loan Mortgage Corporation

or Government National Mortgage Association. Non-agency RMBS include prime, Alt-A and sub-prime RMBS. Prime residential mortgage lending

includes the origination of residential mortgage loans to the most creditworthy borrowers with high quality credit profiles. Alt-A is a classification of

mortgage loans where the risk profile of the borrower falls between prime and sub-prime. Sub-prime mortgage lending is the origination of residential

mortgage loans to borrowers with weak credit profiles. Included within prime and Alt-A RMBS are re-securitization of real estate mortgage investment

conduit (“Re-REMIC”) securities. Re-REMIC RMBS involve the pooling of previous issues of prime and Alt-A RMBS and restructuring the combined

pools to create new senior and subordinated securities. The credit enhancement on the senior tranches is improved through the re-securitization.

46 MetLife, Inc.