MetLife 2013 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

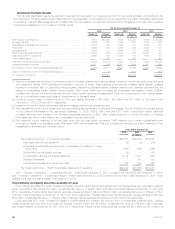

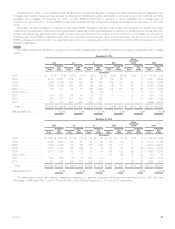

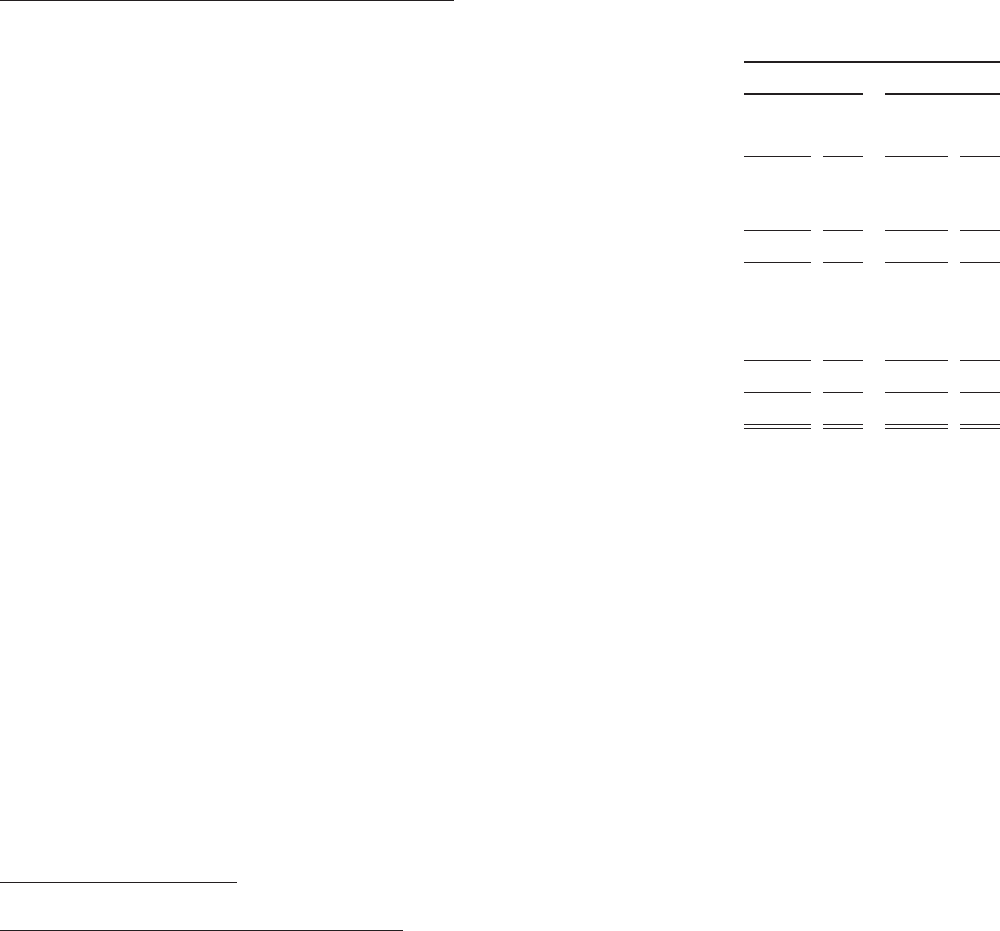

Fair Value of Fixed Maturity and Equity Securities — AFS

Fixed maturity and equity securities AFS measured at estimated fair value on a recurring basis and their corresponding fair value pricing sources are

as follows:

December 31, 2013

Fixed Maturity

Securities Equity

Securities

(In millions) (In millions)

Level 1:

Quoted prices in active markets for identical assets ............................................. $ 25,061 7.2% $ 1,186 34.9%

Level 2:

Independent pricing source ................................................................ 264,703 75.6 715 21.0

Internal matrix pricing or discounted cash flow techniques ......................................... 36,125 10.3 929 27.3

Significant other observable inputs ......................................................... 300,828 85.9 1,644 48.3

Level 3:

Independent pricing source ................................................................ 7,969 2.2 448 13.2

Internal matrix pricing or discounted cash flow techniques ......................................... 13,220 3.8 106 3.1

Independent broker quotations ............................................................. 3,109 0.9 18 0.5

Significant unobservable inputs ........................................................... 24,298 6.9 572 16.8

Total estimated fair value .................................................................... $350,187 100.0% $ 3,402 100.0%

See Note 10 of the Notes to the Consolidated Financial Statements for the fixed maturity securities and equity securities AFS fair value hierarchy.

The composition of fair value pricing sources for and significant changes in Level 3 securities at December 31, 2013 are as follows:

‰The majority of the Level 3 fixed maturity and equity securities AFS were concentrated in five sectors: U.S. and foreign corporate securities, asset-

backed securities (“ABS”), residential mortgage-backed securities (“RMBS”), and foreign government securities.

‰Level 3 fixed maturity securities are priced principally through market standard valuation methodologies, independent pricing services and, to a

much lesser extent, independent non-binding broker quotations using inputs that are not market observable or cannot be derived principally from

or corroborated by observable market data. Level 3 fixed maturity securities consist of less liquid securities with very limited trading activity or

where less price transparency exists around the inputs to the valuation methodologies. Level 3 fixed maturity securities include: alternative

residential mortgage loan (“Alt-A”) and sub-prime RMBS; certain below investment grade private securities and less liquid investment grade

corporate securities (included in U.S. and foreign corporate securities); less liquid ABS and foreign government securities.

‰During the year ended December 31, 2013, Level 3 fixed maturity securities increased by $1.9 billion. The increase was driven by purchases in

excess of sales, partially offset by net transfers out of Level 3 and a decrease in estimated fair value recognized in other comprehensive income

(loss) (“OCI”). The purchases in excess of sales of fixed maturity securities were concentrated in U.S. and foreign corporate securities, ABS,

RMBS, and foreign government securities. The net transfers out of Level 3 were concentrated in U.S. and foreign corporate securities, ABS, and

commercial mortgage-backed securities (“CMBS”), and the decrease in estimated fair value recognized in OCI for fixed maturity securities was

concentrated in U.S. and foreign corporate securities and foreign government securities.

See Note 10 of the Notes to the Consolidated Financial Statements for a rollforward of the fair value measurements for fixed maturity securities and

equity securities AFS measured at estimated fair value on a recurring basis using significant unobservable (Level 3) inputs; analysis of transfers into and/

or out of Level 3; and further information about the valuation techniques and inputs by level by major classes of invested assets that affect the amounts

reported above. See “— Summary of Critical Accounting Estimates — Estimated Fair Value of Investments” for further information on the estimates and

assumptions that affect the amounts reported above.

Fixed Maturity Securities AFS

See Notes 1 and 8 of the Notes to the Consolidated Financial Statements for further information about fixed maturity securities AFS.

Fixed Maturity Securities Credit Quality — Ratings

The Securities Valuation Office of the NAIC evaluates the fixed maturity security investments of insurers for regulatory reporting and capital

assessment purposes and assigns securities to one of six credit quality categories called “NAIC designations.” If no designation is available from the

NAIC, then, as permitted by the NAIC, an internally developed designation is used. The NAIC designations are generally similar to the credit quality

ratings of the Nationally Recognized Statistical Ratings Organizations (“NRSRO”) for marketable fixed maturity securities, except for certain structured

securities as described below. Rating agency ratings are based on availability of applicable ratings from rating agencies on the NAIC credit rating

provider list, including Moody’s Investor Service (“Moody’s”), S&P, Fitch Ratings (“Fitch”), Dominion Bond Rating Service, A.M. Best Company, Kroll

Bond Rating Agency, Egan Jones Ratings Company and Morningstar, Inc. (“Morningstar”). If no rating is available from a rating agency, then an

internally developed rating is used.

The NAIC has adopted revised methodologies for certain structured securities comprised of non-agency RMBS, CMBS and ABS. The NAIC’s

objective with the revised methodologies for these structured securities was to increase the accuracy in assessing expected losses, and to use the

improved assessment to determine a more appropriate capital requirement for such structured securities. The revised methodologies reduce regulatory

reliance on rating agencies and allow for greater regulatory input into the assumption used to estimate expected losses from structured securities. We

apply the revised NAIC methodologies to structured securities held by MetLife, Inc.’s insurance subsidiaries that maintain the NAIC statutory basisof

accounting. The NAIC’s present methodology is to evaluate structured securities held by insurers using the revised NAIC methodologies on an annual

basis. If our insurance subsidiaries acquire structured securities that have not been previously evaluated by the NAIC, but are expected to be evaluated

by the NAIC in the upcoming annual review, an internally developed designation is used until a final designation becomes available.

44 MetLife, Inc.