MetLife 2013 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

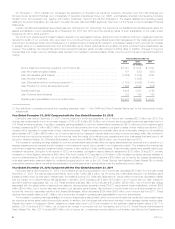

statements of operations and comprehensive income for the year ended December 31, 2012. For a discussion of potential effects of these inquiries on

the Company’s results of operations and the status of the inquiries made by the Department of Financial Services and the NAIC, see “Business — U.S.

Regulation — Holding Company Regulation — Insurance Regulatory Examinations” in the 2013 Form 10-K.

We apply significant judgment when determining the estimated fair value of our reporting units and when assessing the relationship of market

capitalization to the aggregate estimated fair value of our reporting units. The valuation methodologies utilized are subject to key judgments and

assumptions that are sensitive to change. Estimates of fair value are inherently uncertain and represent only management’s reasonable expectation

regarding future developments. These estimates and the judgments and assumptions upon which the estimates are based will, in all likelihood, differ in

some respects from actual future results. Declines in the estimated fair value of our reporting units could result in goodwill impairments in future periods

which could materially adversely affect our results of operations or financial position.

See Note 11 of the Notes to the Consolidated Financial Statements for additional information on our goodwill.

Employee Benefit Plans

Certain subsidiaries of MetLife, Inc. sponsor and/or administer various plans that provide defined benefit pension and other postretirement benefits

covering eligible employees and sales representatives. The calculation of the obligations and expenses associated with these plans requires an

extensive use of assumptions such as the discount rate, expected rate of return on plan assets, rate of future compensation increases and healthcare

cost trend rates, as well as assumptions regarding participant demographics such as rate and age of retirements, withdrawal rates and mortality. In

consultation with external actuarial firms, we determine these assumptions based upon a variety of factors such as historical experience of the plan and

its assets, currently available market and industry data, and expected benefit payout streams.

We determine the expected rate of return on plan assets based upon an approach that considers inflation, real return, term premium, credit spreads,

equity risk premium and capital appreciation, as well as expenses, expected asset manager performance, asset weights and the effect of rebalancing.

Given the amount of plan assets as of December 31, 2012, the beginning of the measurement year, if we had assumed an expected rate of return for

both our pension and other postretirement benefit plans that was 100 basis points higher or 100 basis points lower than the rates we assumed, the

change in our net periodic benefit costs would have been a decrease of $93 million and an increase of $93 million, respectively, in 2013. This

considers only changes in our assumed long-term rate of return given the level and mix of invested assets at the beginning of the year, without

consideration of possible changes in any of the other assumptions described above that could ultimately accompany any changes in our assumed

long-term rate of return.

We determine the discount rates used to value the pension and postretirement obligations, based upon rates commensurate with current yields on

high quality corporate bonds. Given our pension and postretirement obligations as of December 31, 2012, the beginning of the measurement year, if

we had assumed a discount rate for both our pension and postretirement benefit plans that was 100 basis points higher or 100 basis points lower than

the rates we assumed, the change in our net periodic benefit costs would have been a decrease of $146 million and an increase of $168 million,

respectively, in 2013. This considers only changes in our assumed discount rates without consideration of possible changes in any of the other

assumptions described above that could ultimately accompany any changes in our assumed discount rate. The assumptions used may differ materially

from actual results due to, among other factors, changing market and economic conditions and changes in participant demographics. These

differences may have a significant effect on the Company’s consolidated financial statements and liquidity.

See Note 18 of the Notes to the Consolidated Financial Statements for additional discussion of assumptions used in measuring liabilities relating to

our employee benefit plans.

Income Taxes

We provide for federal, state and foreign income taxes currently payable, as well as those deferred due to temporary differences between the financial

reporting and tax bases of assets and liabilities. Our accounting for income taxes represents our best estimate of various events and transactions. These

tax laws are complex and are subject to differing interpretations by the taxpayer and the relevant governmental taxing authorities. In establishing aprovision

for income tax expense, we must make judgments and interpretations about the application of these inherently complex tax laws. We must also make

estimates about when in the future certain items will affect taxable income in the various tax jurisdictions, both domestic and foreign.

The realization of deferred tax assets depends upon the existence of sufficient taxable income within the carryback or carryforward periods under the

tax law in the applicable tax jurisdiction. Valuation allowances are established when management determines, based on available information, that it is

more likely than not that deferred income tax assets will not be realized. Factors in management’s determination include the performance of the

business and its ability to generate capital gains. Significant judgment is required in determining whether valuation allowances should be established, as

well as the amount of such allowances. When making such determination, consideration is given to, among other things, the following:

(i) future taxable income exclusive of reversing temporary differences and carryforwards;

(ii) future reversals of existing taxable temporary differences;

(iii) taxable income in prior carryback years; and

(iv) tax planning strategies.

Disputes over interpretations of the tax laws may be subject to review and adjudication by the court systems of the various tax jurisdictions or may

be settled with the taxing authority upon audit. We determine whether it is more likely than not that a tax position will be sustained upon examination by

the appropriate taxing authorities before any part of the benefit is recorded in the financial statements. We may be required to change our provision for

income taxes when estimates used in determining valuation allowances on deferred tax assets significantly change, or when receipt of new information

indicates the need for adjustment in valuation allowances. Additionally, future events, such as changes in tax laws, tax regulations, or interpretations of

such laws or regulations, could have an impact on the provision for income tax and the effective tax rate. Any such changes could significantly affect the

amounts reported in the financial statements in the year these changes occur.

See Note 19 of the Notes to the Consolidated Financial Statements for additional information on our income taxes.

Litigation Contingencies

We are a party to a number of legal actions and are involved in a number of regulatory investigations. Given the inherent unpredictability of these

matters, it is difficult to estimate the impact on our financial position. Liabilities are established when it is probable that a loss has been incurred and the

amount of the loss can be reasonably estimated. Liabilities related to certain lawsuits, including our asbestos-related liability, are especially difficult to

estimate due to the limitation of available data and uncertainty regarding numerous variables that can affect liability estimates. The data and variables that

impact the assumptions used to estimate our asbestos-related liability include the number of future claims, the cost to resolve claims, the disease mix

and severity of disease in pending and future claims, the impact of the number of new claims filed in a particular jurisdiction and variations in the law in

the jurisdictions in which claims are filed, the possible impact of tort reform efforts, the willingness of courts to allow plaintiffs to pursue claims against us

18 MetLife, Inc.