MetLife 2013 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

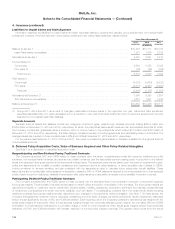

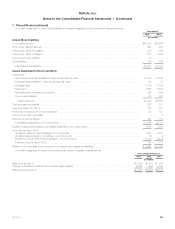

8. Investments (continued)

process include, but are not limited to: (i) the length of time and the extent to which the estimated fair value has been below cost or amortized cost;

(ii) the potential for impairments when the issuer is experiencing significant financial difficulties; (iii) the potential for impairments in an entire industry

sector or sub-sector; (iv) the potential for impairments in certain economically depressed geographic locations; (v) the potential for impairments where

the issuer, series of issuers or industry has suffered a catastrophic loss or has exhausted natural resources; (vi) with respect to fixed maturity

securities, whether the Company has the intent to sell or will more likely than not be required to sell a particular security before the decline in

estimated fair value below amortized cost recovers; (vii) with respect to structured securities, changes in forecasted cash flows after considering the

quality of underlying collateral, expected prepayment speeds, current and forecasted loss severity, consideration of the payment terms of the

underlying assets backing a particular security, and the payment priority within the tranche structure of the security; and (viii) other subjective factors,

including concentrations and information obtained from regulators and rating agencies.

The methodology and significant inputs used to determine the amount of credit loss on fixed maturity securities are as follows:

‰The Company calculates the recovery value by performing a discounted cash flow analysis based on the present value of future cash flows. The

discount rate is generally the effective interest rate of the security prior to impairment.

‰When determining collectability and the period over which value is expected to recover, the Company applies considerations utilized in its overall

impairment evaluation process which incorporates information regarding the specific security, fundamentals of the industry and geographic area in

which the security issuer operates, and overall macroeconomic conditions. Projected future cash flows are estimated using assumptions derived

from management’s best estimates of likely scenario-based outcomes after giving consideration to a variety of variables that include, but are not

limited to: payment terms of the security; the likelihood that the issuer can service the interest and principal payments; the quality and amount of

any credit enhancements; the security’s position within the capital structure of the issuer; possible corporate restructurings or asset sales by the

issuer; and changes to the rating of the security or the issuer by rating agencies.

‰Additional considerations are made when assessing the unique features that apply to certain structured securities including, but not limited to: the

quality of underlying collateral, expected prepayment speeds, current and forecasted loss severity, consideration of the payment terms of the

underlying loans or assets backing a particular security, and the payment priority within the tranche structure of the security.

‰When determining the amount of the credit loss for U.S. and foreign corporate securities, foreign government securities and state and political

subdivision securities, the estimated fair value is considered the recovery value when available information does not indicate that another value is

more appropriate. When information is identified that indicates a recovery value other than estimated fair value, management considers in the

determination of recovery value the same considerations utilized in its overall impairment evaluation process as described above, as well as any

private and public sector programs to restructure such securities.

With respect to securities that have attributes of debt and equity (perpetual hybrid securities), consideration is given in the OTTI analysis as to

whether there has been any deterioration in the credit of the issuer and the likelihood of recovery in value of the securities that are in a severe and

extended unrealized loss position. Consideration is also given as to whether any perpetual hybrid securities, with an unrealized loss, regardless of

credit rating, have deferred any dividend payments. When an OTTI loss has occurred, the OTTI loss is the entire difference between the perpetual

hybrid security’s cost and its estimated fair value with a corresponding charge to earnings.

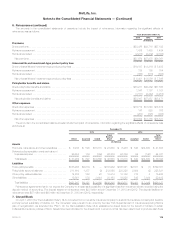

The cost or amortized cost of fixed maturity and equity securities is adjusted for OTTI in the period in which the determination is made. The

Company does not change the revised cost basis for subsequent recoveries in value.

In periods subsequent to the recognition of OTTI on a fixed maturity security, the Company accounts for the impaired security as if it had been

purchased on the measurement date of the impairment. Accordingly, the discount (or reduced premium) based on the new cost basis is accreted

over the remaining term of the fixed maturity security in a prospective manner based on the amount and timing of estimated future cash flows.

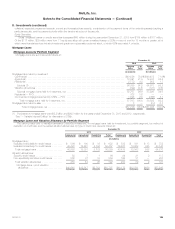

Current Period Evaluation

Based on the Company’s current evaluation of its AFS securities in an unrealized loss position in accordance with its impairment policy, and the

Company’s current intentions and assessments (as applicable to the type of security) about holding, selling and any requirements to sell these

securities, the Company has concluded that these securities are not other-than-temporarily impaired at December 31, 2013. Future OTTI will depend

primarily on economic fundamentals, issuer performance (including changes in the present value of future cash flows expected to be collected), and

changes in credit ratings, collateral valuation, interest rates and credit spreads. If economic fundamentals deteriorate or if there are adverse changes

in the above factors, OTTI may be incurred in upcoming periods.

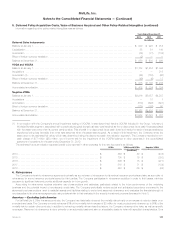

Gross unrealized losses on fixed maturity securities increased $2.9 billion during the year ended December 31, 2013 from $1.7 billion to

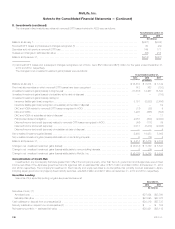

$4.6 billion. The increase in gross unrealized losses for the year ended December 31, 2013, was primarily attributable to an increase in interest rates,

partially offset by narrowing credit spreads.

At December 31, 2013, $296 million of the total $4.6 billion of gross unrealized losses were from 95 fixed maturity securities with an unrealized

loss position of 20% or more of amortized cost for six months or greater.

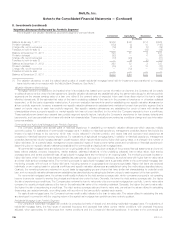

Investment Grade Fixed Maturity Securities

Of the $296 million of gross unrealized losses on fixed maturity securities with an unrealized loss of 20% or more of amortized cost for six months

or greater, $165 million, or 56%, are related to gross unrealized losses on 64 investment grade fixed maturity securities. Unrealized losses on

investment grade fixed maturity securities are principally related to widening credit spreads and, with respect to fixed-rate fixed maturity securities,

rising interest rates since purchase.

Below Investment Grade Fixed Maturity Securities

Of the $296 million of gross unrealized losses on fixed maturity securities with an unrealized loss of 20% or more of amortized cost for six months

or greater, $131 million, or 44%, are related to gross unrealized losses on 31 below investment grade fixed maturity securities. Unrealized losses on

below investment grade fixed maturity securities are principally related to non-agency RMBS (primarily alternative residential mortgage loans) and ABS

(primarily foreign ABS) and are the result of significantly wider credit spreads resulting from higher risk premiums since purchase, largely due to

economic and market uncertainties including concerns over unemployment levels and valuations of residential real estate supporting non-agency

RMBS. Management evaluates non-agency RMBS and ABS based on actual and projected cash flows after considering the quality of underlying

124 MetLife, Inc.