MetLife 2013 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

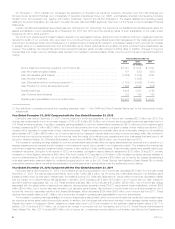

|

|

provided to them, or that financial institutions with significant holdings of sovereign or private debt issued by borrowers in Europe’s perimeter region or

Cyprus could experience financial stress, any of which could have significant adverse effects on the European and global economies and on financial

markets, generally. In September 2012, the ECB announced a new bond buying program, Outright Monetary Transactions (“OMT”), intended to stabilize

the European financial crisis. This program involves the potential purchase by the ECB of unlimited quantities of sovereign bonds with maturities of one

to three years. These large scale purchases of sovereign bonds are intended to provide a buyer of last resort in the event of market stress, raising the

price of the bonds, and lowering their interest rates, making it less expensive for certain countries to borrow money. In the absence of the OMT,

concerns over sovereign debt sustainability could arise, and private demand for sovereign debt could decrease, putting further upward pressure on

sovereign yields. Countries must agree to strict levels of economic reform and oversight as a condition to participate in this program. The OMT has not

been activated to date, but the possibility of its use by the ECB has succeeded in reducing investor concerns over the possible withdrawal of one or

more countries from the Euro zone and has helped to lower sovereign yields in Europe’s perimeter region and Cyprus. The Euro zone has emerged from

its recession, but economic growth is expected to remain relatively muted, with concerns over low inflation becoming more pronounced as countries in

Europe’s perimeter region and Cyprus in particular continue to pursue policies to reduce their macroeconomic imbalances. See “Risk Factors —

Economic Environment and Capital Markets-Related Risks — We Are Exposed to Significant Financial and Capital Markets Risks Which May Adversely

Affect Our Results of Operations, Financial Condition and Liquidity, and May Cause Our Net Investment Income to Vary from Period to Period,” and “Risk

Factors — Economic Environment and Capital Markets-Related Risks — If Difficult Conditions in the Global Capital Markets and the Economy Generally

Persist, They May Materially Adversely Affect Our Business and Results of Operations” in the 2013 Form 10-K.

We face substantial exposure to the Japanese economy given our operations there. Despite a broad recovery in GDP growth and rising inflation over

the last year, structural weaknesses and debt sustainability have yet to be addressed effectively. This leaves the economy vulnerable to further

disruption. The global financial crisis and March 2011 earthquake and related events further pressured Japan’s budget outcomes and public debt

levels. Going forward, Japan’s structural and demographic challenges may continue to limit its potential growth unless reforms that boost productivity

are put into place. Japan’s high public sector debt levels are mitigated by low refinancing risks and its nominal yields on government debt have

remained at a lower level than that of any other advanced country. However, frequent changes in government have prevented policy makers from

implementing fiscal reform measures to put public finances on a sustainable path. In January 2013, the government and the Bank of Japan pledged to

strengthen policy coordination to end deflation and to achieve sustainable economic growth. This was followed by the announcement of a

supplementary budget stimulus program totaling 2% of GDP and the adoption of a 2% inflation target by the Bank of Japan. In early April 2013, the Bank

of Japan announced a new round of monetary easing measures including increased government bond purchases at longer maturities. In October 2013,

the government agreed to raise the consumption tax from 5% to 8% effective April 1, 2014. While this was a positive step, the fiscal impact is likely to be

neutral given the accompanying stimulus spending package. Although the yen has weakened, deflationary pressures have eased and the stock market

has rallied on the back of these announcements, it is too soon to tell whether these actions will have a sustained impact on Japan’s economy. Japan’s

public debt trajectory could continue to rise until a strategy to consolidate public finances and growth-enhancing reforms are implemented.

Impact of a Sustained Low Interest Rate Environment

As a global insurance company, we are affected by the monetary policy of central banks around the world, as well as the monetary policy of the

Board of Governors of the Federal Reserve System (the “Federal Reserve Board”) in the United States. The Federal Reserve Board has taken a number

of actions in recent years to spur economic activity by keeping interest rates low and may take further actions to influence interest rates in the future,

which may have an impact on the pricing levels of risk-bearing investments, and may adversely impact the level of product sales.

On December 18, 2013, the Federal Reserve Board’s Federal Open Market Committee (“FOMC”) decided to modestly reduce the pace of its

purchases of agency mortgage-backed securities from $40 billion per month to $35 billion per month and the pace of its purchases of longer-term U.S.

Treasury securities from $45 billion per month to $40 billion per month. On January 29, 2014, noting cumulative progress toward maximum employment

and the improved outlook for the labor market, the FOMC determined to make a further measured reduction in the pace of its purchases of agency

mortgage-backed securities from $35 billion per month to $30 billion per month and the pace of its purchases of longer-term U.S. Treasury securities from

$40 billion per month to $35 billion per month, beginning in February 2014. These quantitative easing measures are intended to stimulate the economy by

keeping interest rates at low levels. The FOMC will closely monitor economic and financial developments in determining when to further moderate these

quantitative easing measures, including with respect to the rates of unemployment, inflation and long-term inflation. The FOMC has stated that it will likely

reduce the pace of its bond purchases in further measured steps at future meetings if subsequent economic data remains broadly aligned with its current

expectations for a strengthening in the U.S. economy. Any additional action by the Federal Reserve Board to reduce its quantitative easing program could

potentially increase U.S. interest rates from recent historically low levels, with uncertain impacts on U.S. risk markets, and may affect interest rates and risk

markets in other developed and emerging economies. Even after the quantitative easing program ends and the economy strengthens, the FOMC

reaffirmed that it anticipates keeping the target range for the federal funds rate at 0 to .25%, again subject to certain unemployment, inflation and long-term

inflation thresholds. While Janet Yellen, appointed on January 6, 2014 as the new Chairman of the Federal Reserve Board, has pledged continuity in the

Federal Reserve Board’s monetary policy, it is possible that the course of such policy could change under a new Chairman.

Despite recent actions by central banks in Turkey, Brazil and India to raise interest rates in an effort to contain inflation and attract foreign investors,

central banks in other parts of the world, including the ECB, the Bank of England, the Bank of Australia and the Central Bank of China, have followed the

actions of the Federal Reserve Board to lower interest rates. The collective effort globally to lower interest rates was in response to concerns about

Europe’s sovereign debt crisis and slowing global economic growth. We cannot predict with certainty the effect of these programs and policies on

interest rates or the impact on the pricing levels of risk-bearing investments at this time. See “— Investments — Current Environment.”

In periods of declining interest rates, we may have to invest insurance cash flows and reinvest the cash flows we received as interest or return of

principal on our investments in lower yielding instruments. Moreover, borrowers may prepay or redeem the fixed income securities, commercial,

agricultural or residential mortgage loans and mortgage-backed securities in our investment portfolio with greater frequency in order to borrow at lower

market rates. Therefore, some of our products expose us to the risk that a reduction in interest rates will reduce the difference between the amounts that

we are required to credit on contracts in our general account and the rate of return we are able to earn on investments intended to support obligations

under these contracts. This difference between interest earned and interest credited, or margin, is a key metric for the management of, and reporting for,

many of our businesses.

Our expectations regarding future margins are an important component impacting the amortization of certain intangible assets such as DAC and

value of business acquired (“VOBA”). Significantly lower margins may cause us to accelerate the amortization, thereby reducing net income in the

affected reporting period. Additionally, lower margins may also impact the recoverability of intangible assets such as goodwill, require the establishment

of additional liabilities or trigger loss recognition events on certain policyholder liabilities. We review this long-term margin assumption, along with other

10 MetLife, Inc.