MetLife 2013 Annual Report Download - page 200

Download and view the complete annual report

Please find page 200 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

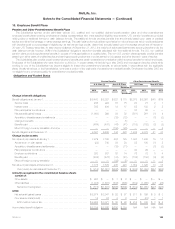

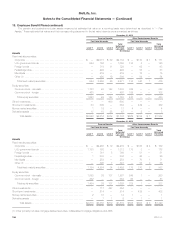

18. Employee Benefit Plans (continued)

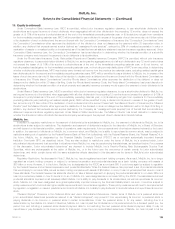

(1) Reflects those assumptions that were most appropriate for the local economic environments of each of the Subsidiaries providing such benefits.

The weighted average discount rate for the U.S. plans is determined annually based on the yield, measured on a yield to worst basis, of a

hypothetical portfolio constructed of high quality debt instruments available on the valuation date, which would provide the necessary future cash flows

to pay the aggregate projected benefit obligation when due.

The weighted average discount rate for non-U.S. pension plans is based on the duration of liabilities on a country by country basis. The rate was

selected by reference to high quality corporate bonds in developed markets or local government bonds where markets were less robust or

nonexistent.

The weighted average expected rate of return on plan assets for the U.S. plans is based on anticipated performance of the various asset sectors in

which the plans invest, weighted by target allocation percentages. Anticipated future performance is based on long-term historical returns of the plan

assets by sector, adjusted for the Subsidiaries’ long-term expectations on the performance of the markets. While the precise expected rate of return

derived using this approach will fluctuate from year to year, the policy of most of the Subsidiaries’ is to hold this long-term assumption constant as long

as it remains within reasonable tolerance from the derived rate.

The weighted average expected long-term rate of return for the non-U.S. pension plans is an aggregation of each country’s expected rate of return

within each asset class. For each country, the rate of return with respect to each asset class was developed based on a building block approach that

considers historical returns, current market conditions, asset volatility and the expectations for future market returns. While the assessment of the

expected rate of return is long-term and not expected to change annually, significant changes in investment strategy or economic conditions may

warrant such a change. The expected rate of return within each asset class, together with any contributions made, are expected to maintain the plans’

ability to meet all required benefit obligations.

The weighted average expected rate of return on plan assets for use in that plan’s valuation in 2014 is currently anticipated to be 6.24% for U.S.

pension benefits and 5.64% for U.S. other postretirement benefits. The weighted average expected rate of return on plan assets for use in that plan’s

valuation in 2014 is currently anticipated to be 3.01% for non-U.S. pension benefits and 7.25% for non-U.S. other postretirement benefits.

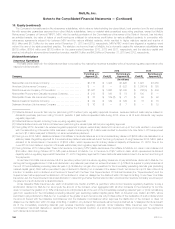

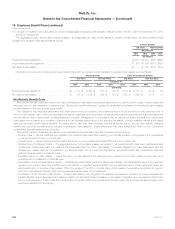

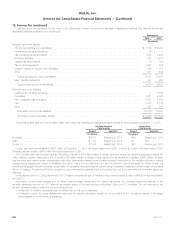

The assumed healthcare costs trend rates used in measuring the APBO and net periodic benefit costs were as follows:

December 31,

2013 2012

Pre-and Post-Medicare eligible claims .......... 6.4% in 2014, gradually decreasing each year

until 2094 reaching the ultimate rate of 4.4%

for Pre-Medicare and 4.6% for

Post-Medicare.

7.8% in 2013, gradually decreasing each year

until 2094 reaching the ultimate rate of 4.4%

for Pre-Medicare and 4.6% for

Post-Medicare.

Assumed healthcare costs trend rates may have a significant effect on the amounts reported for healthcare plans. A 1% change in assumed

healthcare costs trend rates would have the following effects as of December 31, 2013:

U.S. Plans Non-U.S. Plans

One Percent

Increase One Percent

Decrease One Percent

Increase One Percent

Decrease

(In millions)

Effect on total of service and interest costs components ................................ $ 16 $ (13) $— $—

Effect of accumulated postretirement benefit obligations ................................ $235 $(193) $ 1 $ (1)

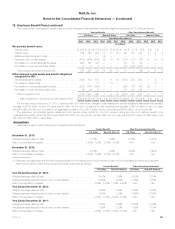

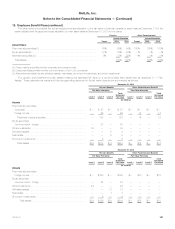

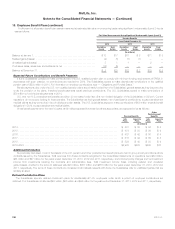

Plan Assets

The pension and other postretirement benefit plan assets are categorized into a three-level fair value hierarchy, as defined in Note 10, based upon

the significant input with the lowest level in its valuation. The following summarizes the types of assets included within the three-level fair value hierarchy

presented below.

Level 1 This category includes separate accounts that are invested in fixed maturity securities, equity securities, derivative assets and short-term

investments which have unadjusted quoted market prices in active markets for identical assets and liabilities.

Level 2 This category includes certain separate accounts that are primarily invested in liquid and readily marketable securities. The estimated fair value

of such separate account is based upon reported NAV provided by fund managers and this value represents the amount at which transfers into

and out of the respective separate account are effected. These separate accounts provide reasonable levels of price transparency and can be

corroborated through observable market data.

Certain separate accounts are invested in investment partnerships designated as hedge funds. The values for these separate accounts is

determined monthly based on the NAV of the underlying hedge fund investment. Additionally, such hedge funds generally contain lock out or

other waiting period provisions for redemption requests to be filled. While the reporting and redemption restrictions may limit the frequency of

trading activity in separate accounts invested in hedge funds, the reported NAV, and thus the referenced value of the separate account,

provides a reasonable level of price transparency that can be corroborated through observable market data.

Directly held investments are primarily invested in U.S. and foreign government and corporate securities.

Level 3 This category includes separate accounts that are invested in fixed maturity securities, equity securities, derivative assets and other investments

that provide little or no price transparency due to the infrequency with which the underlying assets trade and generally require additional time to

liquidate in an orderly manner. Accordingly, the values for separate accounts invested in these alternative asset classes are based on inputs

that cannot be readily derived from or corroborated by observable market data.

192 MetLife, Inc.