MetLife 2013 Annual Report Download - page 152

Download and view the complete annual report

Please find page 152 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

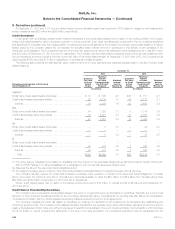

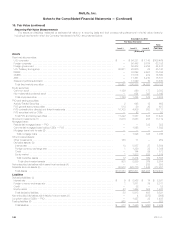

9. Derivatives (continued)

At December 31, 2013 and 2012, the cumulative foreign currency translation gain (loss) recorded in AOCI related to hedges of net investments in

foreign operations was $233 million and ($98) million, respectively.

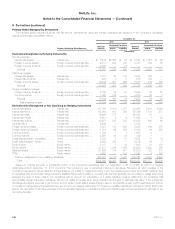

Credit Derivatives

In connection with synthetically created credit investment transactions and credit default swaps held in relation to the trading portfolio, the Company

writes credit default swaps for which it receives a premium to insure credit risk. Such credit derivatives are included within the non-qualifying derivatives

and derivatives for purposes other than hedging table. If a credit event occurs, as defined by the contract, the contract may be cash settled or it may be

settled gross by the Company paying the counterparty the specified swap notional amount in exchange for the delivery of par quantities of the

referenced credit obligation. The Company’s maximum amount at risk, assuming the value of all referenced credit obligations is zero, was $9.1 billion

and $8.9 billion at December 31, 2013 and 2012, respectively. The Company can terminate these contracts at any time through cash settlement with

the counterparty at an amount equal to the then current fair value of the credit default swaps. At December 31, 2013 and 2012, the Company would

have received $165 million and $74 million, respectively, to terminate all of these contracts.

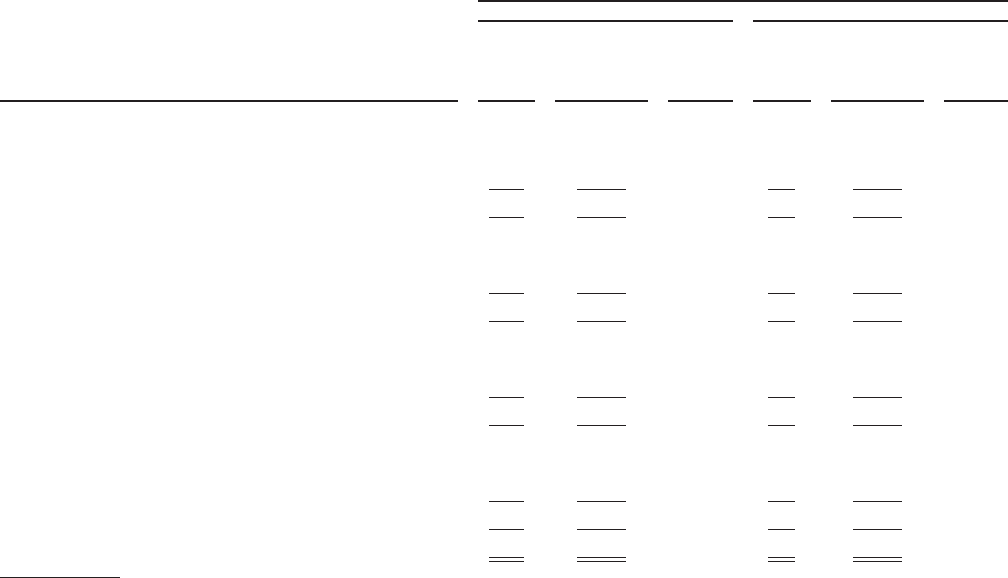

The following table presents the estimated fair value, maximum amount of future payments and weighted average years to maturity of written credit

default swaps at:

December 31,

2013 2012

Rating Agency Designation of Referenced

Credit Obligations (1)

Estimated

Fair Value

of Credit

Default

Swaps

Maximum

Amount

of Future

Payments under

Credit Default

Swaps (2)

Weighted

Average

Years to

Maturity (3)

Estimated

Fair Value

of Credit

Default

Swaps

Maximum

Amount

of Future

Payments under

Credit Default

Swaps (2)

Weighted

Average

Years to

Maturity (3)

(In millions) (In millions)

Aaa/Aa/A

Single name credit default swaps (corporate) ................... $ 10 $ 545 2.6 $10 $ 777 2.7

Credit default swaps referencing indices ...................... 26 2,739 1.5 42 2,713 2.1

Subtotal .............................................. 36 3,284 1.6 52 3,490 2.2

Baa

Single name credit default swaps (corporate) ................... 24 1,320 3.1 8 1,314 3.4

Credit default swaps referencing indices ...................... 73 4,071 4.7 11 3,750 4.9

Subtotal .............................................. 97 5,391 4.3 19 5,064 4.5

Ba

Single name credit default swaps (corporate) ................... — 5 3.8 — 25 2.7

Credit default swaps referencing indices ...................... — — — — — —

Subtotal .............................................. — 5 3.8 — 25 2.7

B

Single name credit default swaps (corporate) ................... — — — — — —

Credit default swaps referencing indices ...................... 32 375 4.9 3 300 4.9

Subtotal .............................................. 32 375 4.9 3 300 4.9

Total .............................................. $165 $9,055 3.4 $74 $8,879 3.6

(1) The rating agency designations are based on availability and the midpoint of the applicable ratings among Moody’s Investors Service (“Moody’s”),

S&P and Fitch Ratings. If no rating is available from a rating agency, then an internally developed rating is used.

(2) Assumes the value of the referenced credit obligations is zero.

(3) The weighted average years to maturity of the credit default swaps is calculated based on weighted average notional amounts.

The Company has also entered into credit default swaps to purchase credit protection on certain of the referenced credit obligations in the table

above. As a result, the maximum amounts of potential future recoveries available to offset the $9.1 billion and $8.9 billion from the table above were

$90 million and $150 million at December 31, 2013 and 2012, respectively.

Written credit default swaps held in relation to the trading portfolio amounted to $10 million in notional and $0 in fair value at both December 31,

2013 and 2012.

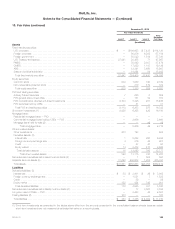

Credit Risk on Freestanding Derivatives

The Company may be exposed to credit-related losses in the event of nonperformance by counterparties to derivatives. Generally, the current credit

exposure of the Company’s derivatives is limited to the net positive estimated fair value of derivatives at the reporting date after taking into consideration

the existence of master netting or similar agreements and any collateral received pursuant to such agreements.

The Company manages its credit risk related to derivatives by entering into transactions with creditworthy counterparties and establishing and

monitoring exposure limits. The Company’s OTC-bilateral derivative transactions are generally governed by ISDA Master Agreements which provide for

legally enforceable set-off and close-out netting of exposures to specific counterparties in the event of early termination of a transaction, which includes,

but is not limited to, events of default and bankruptcy. In the event of an early termination, the Company is permitted to set-off receivables from the

144 MetLife, Inc.