MetLife 2013 Annual Report Download - page 193

Download and view the complete annual report

Please find page 193 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

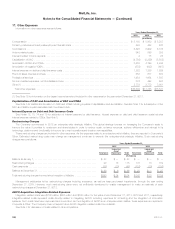

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

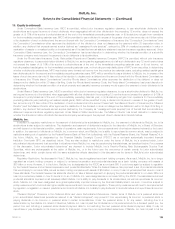

16. Equity (continued)

Under Connecticut State Insurance Law, MICC is permitted, without prior insurance regulatory clearance, to pay stockholder dividends to its

stockholders as long as the amount of such dividends, when aggregated with all other dividends in the preceding 12 months, does not exceed the

greater of: (i) 10% of its surplus to policyholders as of the end of the immediately preceding calendar year; or (ii) its statutory net gain from operations

for the immediately preceding calendar year. MICC will be permitted to pay a dividend in excess of the greater of such two amounts only if it files notice

of its declaration of such a dividend and the amount thereof with the Connecticut Commissioner of Insurance (the “Connecticut Commissioner”) and

the Connecticut Commissioner either approves the distribution of the dividend or does not disapprove the payment within 30 days after notice. In

addition, any dividend that exceeds earned surplus (defined as “unassigned funds (surplus)”, reduced by 25% of unrealized appreciation in value or

revaluation of assets or unrealized profits on investments) as of the last filed annual statutory statement requires insurance regulatory approval. Under

Connecticut State Insurance Law, the Connecticut Commissioner has broad discretion in determining whether the financial condition of a stock life

insurance company would support the payment of such dividends to its stockholders.

Under the Rhode Island Insurance Code, Metropolitan Property and Casualty Insurance Company (“MPC”) is permitted, without prior insurance

regulatory clearance, to pay a stockholder dividend to MetLife, Inc. as long as the aggregate amount of all such dividends in any 12 month period does

not exceed the lesser of: (i) 10% of its surplus to policyholders as of the end of the immediately preceding calendar year; or (ii) net income, not

including realized capital gains, for the immediately preceding calendar year, not including pro rata distributions of MPC’s own securities. In determining

whether a dividend is extraordinary, MPC may include carry forward net income from the previous two calendar years, excluding realized capital gains

less dividends paid in the second and immediately preceding calendar years. MPC will be permitted to pay a dividend to MetLife, Inc. in excess of the

lesser of such two amounts only if it files notice of its intention to declare such a dividend and the amount thereof with the Rhode Island Commissioner

of Insurance (the “Rhode Island Commissioner”) and the Rhode Island Commissioner either approves the distribution of the dividend or does not

disapprove the distribution within 30 days of its filing. Under the Rhode Island Insurance Code, the Rhode Island Commissioner has broad discretion in

determining whether the financial condition of a stock property and casualty insurance company would support the payment of such dividends to its

stockholders.

Under Missouri State Insurance Law, MLIIC is permitted, without prior insurance regulatory clearance, to pay a stockholder dividend to MetLife, Inc.

as long as the amount of the dividend when aggregated with all other dividends in the preceding 12 months does not exceed the greater of: (i) 10% of

its surplus to policyholders as of the end of the immediately preceding calendar year; or (ii) its statutory net gain from operations for the immediately

preceding calendar year (excluding net realized capital gains). MLIIC will be permitted to pay a dividend to its parent in excess of the greater of such

two amounts only if it files notice of the declaration of such a dividend and the amount thereof with the Missouri Director of Insurance (the “Missouri

Director”) and the Missouri Director either approves the distribution of the dividend or does not disapprove the distribution within 30 days of its filing. In

addition, any dividend that exceeds earned surplus (defined by the Company as “unassigned funds (surplus)”) as of the last filed annual statutory

statement requires insurance regulatory approval. Under Missouri State Insurance Law, the Missouri Director has broad discretion in determining

whether the financial condition of a stock life insurance company would support the payment of such dividends to its stockholders.

MetLife, Inc.

In addition to regulatory restrictions on the payment of dividends by its subsidiaries to MetLife, Inc., the payment of dividends by MetLife, Inc. to its

stockholders is also subject to restrictions. The declaration and payment of dividends is subject to the discretion of MetLife, Inc.’s Board of Directors,

and will depend on its financial condition, results of operations, cash requirements, future prospects and other factors deemed relevant by the board.

In addition, the payment of dividends on MetLife, Inc.’s common stock, and MetLife, Inc.’s ability to repurchase its common stock, may be subject to

restrictions arising out of regulation by the Federal Reserve Bank of New York (collectively, with the Federal Reserve Board, the “Federal Reserve”) if, in

the future, MetLife, Inc. is designated by the Financial Stability Oversight Council (“FSOC”) as a non-bank systemically important financial

institution (“non-bank SIFI”), as described below. They are also subject to restrictions under the terms of MetLife, Inc.’s preferred stock, junior

subordinated debentures and trust securities in situations where MetLife, Inc. may be experiencing financial stress, as described below. For purposes

of this discussion, “junior subordinated debentures” are deemed to include MetLife, Inc.’s Fixed-to-Floating Rate Exchangeable Surplus Trust

Securities, which are exchangeable at the option of MetLife, Inc., or in the future upon the occurrence of certain events, for junior subordinated

debentures, and which contain terms with the same substantive effects described in this discussion as the terms in MetLife’s junior subordinated

debentures.

Regulatory Restrictions. As discussed in Note 3, MetLife, Inc. has de-registered as a bank holding company. As a result, MetLife, Inc. is no longer

regulated as a bank holding company or subject to enhanced supervision and prudential standards as a bank holding company with assets of

$50 billion or more. However, if, in the future, MetLife, Inc. is designated by the FSOC as a non-bank SIFI, it could once again be subject to regulation

by the Federal Reserve and enhanced supervision and prudential standards. While the Federal Reserve has proposed a set of prudential standards

that would apply to non-bank SIFIs, as well as bank holding companies with assets of $50 billion or more, it has not yet adopted final rules for most of

these standards. The Federal Reserve has stated its intention to take a tailored approach to applying the prudential standards to non-bank SIFIs, but

has not provided any details on how it intends to do so. If MetLife, Inc. were designated as a non-bank SIFI by the FSOC, the associated enhanced

prudential standards imposed could adversely affect MetLife, Inc.’s ability to pay dividends to its stockholders, as well as repurchase its common

stock. MetLife, Inc. has been designated as a global systemically important insurer by the Financial Stability Board. As such, it could be subject to

policy measures which could include higher capital requirements and more intensive regulation. These policy measures would need to be implemented

by regulation or legislation in relevant jurisdictions but could limit MetLife, Inc.’s ability to pay dividends to its stockholders and repurchase its common

stock.

“Dividend Stopper” Provisions in the Preferred Stock and Junior Subordinated Debentures. Certain terms of MetLife, Inc.’s preferred stock and

junior subordinated debentures (sometimes referred to as “dividend stoppers”) may prevent it from repurchasing its common or preferred stock or

paying dividends on its common or preferred stock in certain circumstances. Under the preferred stock, if, for any reason, including due to a

determination by the MetLife, Inc. Board of Directors, MetLife, Inc. has not paid the full dividends on its preferred stock for a dividend period (i.e., the

period from and including a preferred stock dividend payment date to, but excluding the next preferred stock dividend payment date), it may not

repurchase or pay dividends on its common stock for that period. Under the junior subordinated debentures, if MetLife, Inc. has not paid in full the

MetLife, Inc. 185