MetLife 2013 Annual Report Download - page 178

Download and view the complete annual report

Please find page 178 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

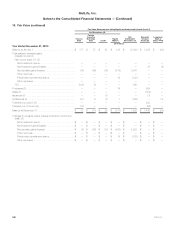

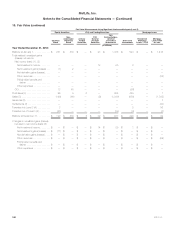

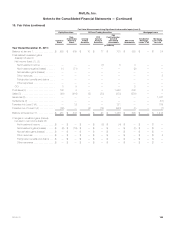

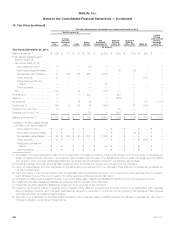

MetLife, Inc.

Notes to the Consolidated Financial Statements — (Continued)

10. Fair Value (continued)

Amounts recoverable under ceded reinsurance agreements, which the Company has determined do not transfer significant risk such that they are

accounted for using the deposit method of accounting, have been classified as Level 3. The valuation is based on discounted cash flow

methodologies using significant unobservable inputs. The estimated fair value is determined using interest rates determined to reflect the appropriate

credit standing of the assuming counterparty.

The amounts on deposit for derivative settlements, classified within Level 2, essentially represent the equivalent of demand deposit balances and

amounts due for securities sold are generally received over short periods such that the estimated fair value approximates carrying value.

Other Assets

These other assets are principally comprised of a receivable for cash paid to an unaffiliated financial institution under the MetLife Reinsurance

Company of Charleston (“MRC”) collateral financing arrangement described in Note 13. The estimated fair value of the receivable for the cash paid to

the unaffiliated financial institution under the MRC collateral financing arrangement is determined by discounting the expected future cash flows using a

discount rate that reflects the credit rating of the unaffiliated financial institution.

PABs

These PABs include investment contracts. Embedded derivatives on investment contracts and certain variable annuity guarantees accounted for as

embedded derivatives are excluded from this caption in the preceding tables as they are separately presented in “— Recurring Fair Value

Measurements.”

The investment contracts primarily include certain funding agreements, fixed deferred annuities, modified guaranteed annuities, fixed term payout

annuities and total control accounts. The valuation of these investment contracts is based on discounted cash flow methodologies using significant

unobservable inputs. The estimated fair value is determined using current market risk-free interest rates adding a spread to reflect the nonperformance

risk in the liability.

Bank Deposits

Due to the frequency of interest rate resets on customer bank deposits held in money market accounts, the Company believes that there is minimal

risk of a material change in interest rates such that the estimated fair value approximates carrying value. For time deposits, the Company has taken into

consideration the sale price for the disposition of the depository business of MetLife Bank to determine the estimated fair value of bank deposits. See

Note 3.

Long-term Debt, Collateral Financing Arrangements and Junior Subordinated Debt Securities

The estimated fair values of long-term debt and junior subordinated debt securities are principally determined using market standard valuation

methodologies. Capital leases, which are not required to be disclosed at estimated fair value are excluded from the preceding tables.

Valuations classified as Level 2 are based primarily on quoted prices in markets that are not active or using matrix pricing that use standard market

observable inputs such as quoted prices in markets that are not active and observable yields and spreads in the market. Instruments valued using

discounted cash flow methodologies use standard market observable inputs including market yield curve, duration, call provisions, observable prices

and spreads for similar publicly traded or privately traded issues.

Valuations classified as Level 3 are based primarily on discounted cash flow methodologies that utilize unobservable discount rates that can vary

significantly based upon the specific terms of each individual arrangement. The determination of estimated fair values of collateral financing

arrangements incorporates valuations obtained from the counterparties to the arrangements, as part of the collateral management process.

Other Liabilities

Other liabilities consist primarily of interest and dividends payable, amounts due for securities purchased but not yet settled, funds withheld

amounts payable, which are contractually withheld by the Company in accordance with the terms of the reinsurance agreements, and amounts

payable under certain assumed reinsurance agreements, which are recorded using the deposit method of accounting. The Company evaluates the

specific terms, facts and circumstances of each instrument to determine the appropriate estimated fair values, which are not materially different from

the carrying values, with the exception of certain deposit type reinsurance payables. For such payables, the estimated fair value is determined as the

present value of expected future cash flows, which are discounted using an interest rate determined to reflect the appropriate credit standing of the

assuming counterparty.

Separate Account Liabilities

Separate account liabilities represent those balances due to policyholders under contracts that are classified as investment contracts.

Separate account liabilities classified as investment contracts primarily represent variable annuities with no significant mortality risk to the Company

such that the death benefit is equal to the account balance, funding agreements related to group life contracts and certain contracts that provide for

benefit funding.

Since separate account liabilities are fully funded by cash flows from the separate account assets which are recognized at estimated fair value as

described in the section “— Recurring Fair Value Measurements,” the value of those assets approximates the estimated fair value of the related separate

account liabilities. The valuation techniques and inputs for separate account liabilities are similar to those described for separate account assets.

11. Goodwill

Goodwill is the excess of cost over the estimated fair value of net assets acquired. Goodwill is not amortized but is tested for impairment at least

annually or more frequently if events or circumstances, such as adverse changes in the business climate, indicate that there may be justification for

conducting an interim test. Step 1 of the goodwill impairment process requires a comparison of the fair value of a reporting unit to its carrying value. In

performing the Company’s goodwill impairment tests, the estimated fair values of the reporting units are first determined using a market multiple valuation

approach. When further corroboration is required, the Company uses a discounted cash flow valuation approach. For reporting units which are

particularly sensitive to market assumptions, the Company may use additional valuation methodologies to estimate the reporting units’ fair values.

The market multiple valuation approach utilizes market multiples of companies with similar businesses and the projected operating earnings of the

reporting unit. The discounted cash flow valuation approach requires judgments about revenues, operating earnings projections, capital market

170 MetLife, Inc.