MetLife 2013 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2013 MetLife annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

|

|

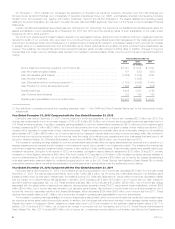

Financial Services for Executive Life Insurance Company of New York (“ELNY”). Results for 2012 include a $52 million, net of income tax, charge

representing a multi-state examination payment related to unclaimed property and MetLife’s use of the U.S. Social Security Administration’s Death

Master File to identify potential life insurance claims, as well as the expected acceleration of benefit payments to policyholders under the settlements.

Also, 2012 includes a $50 million, net of income tax, impairment charge on an intangible asset related to a previously acquired dental business.

Consolidated Company Outlook

As part of an enterprise-wide strategic initiative, by 2016, we expect to increase our operating return on common equity, excluding accumulated

other comprehensive income (“AOCI”), to the 12% to 14% range, driven by higher operating earnings. This target assumes that regulatory capital rules

appropriately reflect the life insurance business model and that we have clarity on the rules in a reasonable time frame, allowing for meaningful share

repurchases prior to 2016. If we are unable to engage in such repurchases, we expect the range of our operating return on common equity, excluding

AOCI, to be 11% to 13%. Also, as part of this initiative, we will leverage our scale to improve the value we provide to customers and shareholders in

order to achieve $1 billion in efficiencies, $600 million of which is expected to be related to net pre-tax expense savings, and $400 million of which we

expect to be primarily reinvested in our technology, platforms and functionality to improve our current operations and develop new capabilities. We also

continue to shift our product mix toward protection products and away from more capital-intensive products, in order to generate more predictable

operating earnings and cash flows, and improve our risk profile and free cash flow.

We expect to achieve the 2016 target range on our operating return on common equity by primarily focusing on the following:

‰Growth in premiums, fees and other revenues driven by:

– Accelerated growth in Group, Voluntary & Worksite Benefits;

– Increased fee revenue reflecting the benefit of higher equity markets on our separate account balances; and

– Increases in our businesses outside of the U.S., notably accident & health, from continuing organic growth throughout our various geographic

regions and leveraging of our multichannel distribution network.

‰Expanding our presence in emerging markets, including potential merger and acquisition activity. We expect that by 2016, 20% or more of our

operating earnings will come from emerging markets, with the acquisition of ProVida contributing to this increase.

‰Focus on disciplined underwriting. We see no significant changes to the underlying trends that drive underwriting results; however, unanticipated

catastrophes, similar to Superstorm Sandy, could result in a high volume of claims.

‰Focus on expense management in the light of the low interest rate environment, and continued focus on expense control throughout the

Company.

‰Continued disciplined approach to investing and asset/liability management (“ALM”), through our enterprise risk and ALM governance process.

Impact of Superstorm Sandy

On October 29, 2012, Superstorm Sandy made landfall in the northeastern United States causing extensive property damage. MetLife’s property &

casualty business’ gross losses from Superstorm Sandy were approximately $150 million, before income tax. As of December 31, 2012, we recognized

total net losses related to the catastrophe of $90 million, net of income tax and reinsurance recoverables and including reinstatement premiums, which

impacted the Retail and Group, Voluntary & Worksite Benefits segments. The Retail and Group, Voluntary & Worksite Benefits segments recorded net

losses related to the catastrophe of $49 million and $41 million, each net of income tax reinsurance recoverables and reinstatement premiums,

respectively.

We did not incur any losses related to Superstorm Sandy in 2013, however, we may incur additional storm-related losses in future periods as claims

are received from insureds and claims to reinsurers are processed. Reinsurance recoveries are dependent on the continued creditworthiness of the

reinsurers, which may be affected by their other reinsured losses in connection with Superstorm Sandy and otherwise.

Industry Trends

We continue to be impacted by the unstable global financial and economic environment that has been affecting the industry.

Financial and Economic Environment

Our business and results of operations are materially affected by conditions in the global capital markets and the economy generally. Stressed

conditions, volatility and disruptions in global capital markets, particular markets, or financial asset classes can have an adverse effect on us, in part

because we have a large investment portfolio and our insurance liabilities are sensitive to changing market factors. Global market factors, including

interest rates, credit spreads, equity prices, real estate markets, foreign currency exchange rates, consumer spending, business investment,

government spending, the volatility and strength of the capital markets, deflation and inflation, all affect the business and economic environment and,

ultimately, the amount and profitability of our business. Disruptions in one market or asset class can also spread to other markets or asset classes.

Upheavals in the financial markets can also affect our business through their effects on general levels of economic activity, employment and customer

behavior. While our diversified business mix and geographically diverse business operations partially mitigate these risks, correlation across regions,

countries and global market factors may reduce the benefits of diversification. Financial markets have also been affected by concerns over U.S. fiscal

and monetary policy, although recent signs of Congressional compromise, reflected in the passage of a two-year budget agreement in December 2013

and the approval on February 12, 2014 of a bill to raise the debt ceiling until March 2015, appear to have alleviated some of these concerns. However,

unless long-term steps are taken to raise the debt ceiling and reduce the federal deficit, rating agencies have warned of the possibility of future

downgrades of U.S. Treasury securities. These issues could, on their own, or combined with the possible slowing of the global economy generally,

send the U.S. into a new recession, have severe repercussions to the U.S. and global credit and financial markets, further exacerbate concerns over

sovereign debt of other countries and disrupt economic activity in the U.S. and elsewhere.

Concerns about the economic conditions, capital markets and the solvency of certain European Union (“EU”) member states, including Portugal,

Ireland, Italy, Greece and Spain (“Europe’s perimeter region”) and Cyprus, and of financial institutions that have significant direct or indirect exposure to

debt issued by these countries, have been a cause of elevated levels of market volatility. However, after several tumultuous years, economic conditions

in Europe’s perimeter region seem to be stabilizing or improving, as evidenced by the stabilization of downward credit ratings momentum, particularly in

Spain, Portugal and Ireland. This, combined with greater European Central Bank (“ECB”) support and improving macroeconomic conditions at the

country level, has reduced the risk of default on the sovereign debt of Europe’s perimeter region and Cyprus and the risk of possible withdrawal of one

or more countries from the Euro zone. See “— Investments — Current Environment” for information regarding credit ratings downgrades, support

programs for Europe’s perimeter region and Cyprus and our exposure to obligations of European governments and private obligors.

The financial markets have also been affected by concerns that other EU member states could experience similar financial troubles, that some

countries could default on their obligations, have to restructure their outstanding debt, or be unable or unwilling to comply with the terms of any aid

MetLife, Inc. 9