Capital One 2015 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

80 Capital One Financial Corporation (COF)

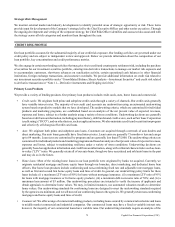

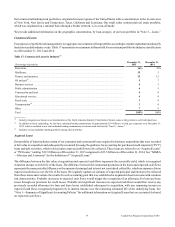

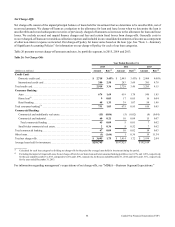

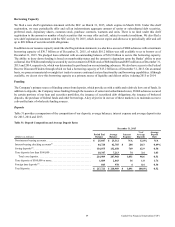

Table 21: Credit Score Distribution

(Percentage of portfolio) December 31,

2015

December 31,

2014

Domestic credit card - Refreshed FICO scores:(1)

Greater than 660 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 66% 68%

660 or below . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34 32

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100% 100%

Auto - At origination FICO scores:(2)

Greater than 660 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51% 47%

621 - 660 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17 17

620 or below . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32 36

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 100% 100%

__________

(1) Credit scores generally represent FICO scores. These scores are obtained from one of the major credit bureaus at origination and are refreshed monthly

thereafter. We approximate non-FICO credit scores to comparable FICO scores for consistency purposes. Balances for which no credit score is available or

the credit score is invalid are included in the 660 or below category.

(2) Credit scores represent FICO scores. These scores are obtained from three credit bureaus at the time of application and are not refreshed thereafter. The FICO

score distribution is based on the average scores. Balances for which no credit score is available or the credit score is invalid are included in the 620 or below

category.

We present information in the section below on the credit performance of our loan portfolio, including the key metrics we use in

tracking changes in the credit quality of our loan portfolio.

See “Note 5—Loans” in this Report for additional credit quality information. Also, see “Note 1—Summary of Significant

Accounting Policies” for information on our accounting policies for delinquent and nonperforming loans, net charge-offs and

TDRs for each of our loan categories.

Delinquency Rates

We consider the entire balance of an account to be delinquent if the minimum required payment is not received by the customer’s

due date, measured at the reporting date. Our 30+ day delinquency metrics include all loans held for investment that are 30 or

more days past due, whereas our 30+ day performing delinquency metrics include loans that are 30 or more days past due but are

currently classified as performing and accruing interest. The 30+ day delinquency and 30+ day performing delinquency metrics

are the same for domestic credit card loans, as we continue to classify the substantial majority of domestic credit card loans as

performing until the account is charged-off, typically when the account is 180 days past due. See “Note 1—Summary of Significant

Accounting Policies” for information on our policies for classifying loans as nonperforming for each of our loan categories. We

provide additional information on our credit quality metrics above under “Business Segment Financial Performance.”