Capital One 2015 Annual Report Download - page 226

Download and view the complete annual report

Please find page 226 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

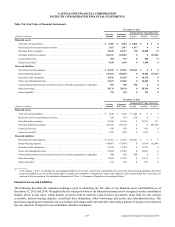

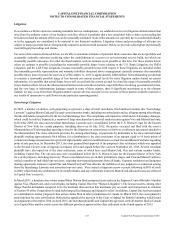

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

207 Capital One Financial Corporation (COF)

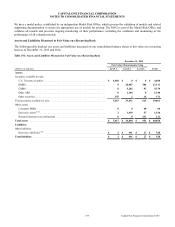

Due to the use of significant unobservable inputs, loans held for investment are classified as Level 3 under the fair value hierarchy.

Fair value adjustments for individually impaired collateralized loans held for investment are recorded in provision for credit losses

in the consolidated statements of income.

Loans Held For Sale

Loans held for sale are carried at the lower of aggregate cost, net of deferred fees and deferred origination costs, or fair value. We

originate loans with the intent to sell them. Certain commercial mortgage loans are sold to government-sponsored enterprises as

part of a delegated underwriting and servicing (“DUS”) program. For DUS commercial mortgage loans, the fair value is estimated

primarily using contractual prices and other observable market-based inputs. For residential mortgage loans classified as held for

sale, the fair value is estimated using observable market prices for loans with similar characteristics as the primary component,

with the secondary component derived from typical securitization activities and market conditions. Credit card loans held for sale

are valued based on other observable market-based inputs. These assets are therefore classified as Level 2. Fair value adjustments

to loans held for sale are recorded in other non-interest income in our consolidated statements of income.

Interest Receivable

The carrying amount of interest receivable approximates the fair value of this asset due to its relatively short-term nature.

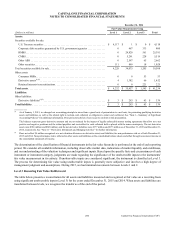

Derivative Assets and Liabilities

We use both exchange-traded derivatives and OTC derivatives to manage our interest rate and foreign currency risk exposure.

Quoted market prices are available and used to value our exchange-traded derivatives, which we classify as Level 1. However,

predominantly all of our derivatives are traded in OTC markets where quoted market prices are not always readily available.

Therefore, we value most OTC derivatives using valuation techniques, which include internally-developed models. We primarily

rely on market observable inputs for our models, such as interest rate yield curves, credit curves, option volatility and currency

rates, that vary depending on the type of derivative and nature of the underlying rate, price or index upon which the derivative’s

value is based. Where model inputs can be observed in a liquid market and the model does not require significant judgment, such

derivatives are typically classified as Level 2. When instruments are traded in less liquid markets and significant inputs are

unobservable, such as interest rate swaps whose remaining terms do not correlate with market observable interest rate yield curves,

the derivatives are classified as Level 3. The impact of counterparty non-performance risk is considered when measuring the fair

value of derivative assets. We validate the pricing obtained from the internal models through comparison of pricing to additional

sources, including external valuation agents and other internal sources. Pricing variances among different pricing sources are

analyzed and validated. These derivatives are included in other assets or other liabilities on the consolidated balance sheets.

Mortgage Servicing Rights

We record consumer MSRs at fair value on a recurring basis, while commercial MSRs are subsequently measured at amortized

cost with impairment recognized as a reduction in other non-interest income. MSRs do not trade in an active market with readily

observable prices. Accordingly, we determine the fair value of MSRs using a valuation model that calculates the present value of

estimated future net servicing income. The model incorporates assumptions that we believe other market participants use in

estimating future net servicing income, including estimates of prepayment speeds, discount rate/option-adjusted spreads, cost to

service, contractual servicing fee income, ancillary income and late fees. Fair value measurements of MSRs use significant

unobservable inputs and, accordingly, are classified as Level 3. In the event we enter into an agreement with a third party to sell

the MSRs, the valuation is based on the agreed upon sale price which is considered to be the exit price and the MSRs are classified

as Level 2.

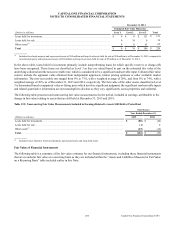

Retained Interests in Securitizations

We have retained interests in various mortgage securitizations from previous acquisitions. Our retained interest includes rights to

future cash flows arising from the receivables, the most significant being certificated interest-only bonds issued by a trust. We

record our interest in these deals at fair value using market indications and valuation models to calculate the present value of future

income. The models incorporate various assumptions that market participants use in estimating future income including weighted-

average life, constant prepayment rate, discount rate, default rate and severity.