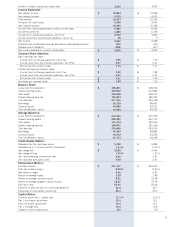

Capital One 2015 Annual Report Download - page 23

Download and view the complete annual report

Please find page 23 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

4 Capital One Financial Corporation (COF)

Mortgage Lending

The CFPB has issued several final rules pursuant to the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-

Frank Act”) that provide additional disclosure requirements and substantive limitations on our mortgage lending activities. These

rules, which include the Ability-to-Repay and Qualified Mortgage Standards under the TILA (Regulation Z) and Integrated

Mortgage Disclosures under the Real Estate Settlement Procedures Act (Regulation X) and the TILA (Regulation Z), could impact

the type and amount of mortgage loans we offer.

Under the Dodd-Frank Act credit risk retention rules, securitizers also are generally required to retain a 5% economic interest in

the credit risk of assets sold through the issuance of asset-backed securitizations, with an exemption for traditionally underwritten

residential mortgage loans that meet the definition of a qualified residential mortgage loan. The final implementing rules on risk

retention define a qualified residential mortgage loan to be identical to the CFPB’s definition of a qualified mortgage loan. Therefore,

we may securitize such loans without being required to retain credit risk under these rules.

Debit Interchange Fees

The Dodd-Frank Act requires that the amount of any interchange fee received by a debit card issuer with respect to debit card

transactions be reasonable and proportional to the cost incurred by the issuer with respect to the transaction. In 2011 and 2012,

the Federal Reserve adopted final rules that implement the portion of the Dodd-Frank Act that limits interchange fees received by

a debit card issuer. The final rules limited interchange fees per debit card transaction to $0.21 plus five basis points of the transaction

amount and provided for an additional $0.01 fraud prevention adjustment to the interchange fee for issuers that meet certain fraud

prevention requirements. In August 2015, the Federal Reserve issued a clarification regarding the inclusion of transaction-

monitoring costs in its interchange fee rules, which clarification did not have any impact on the rules or our debit card business.

The clarification followed a series of decisions in the federal courts that upheld the interchange rules.

Bank Secrecy Act and USA PATRIOT Act of 2001

The Bank Secrecy Act and the USA PATRIOT Act of 2001 (“Patriot Act”) require financial institutions, among other things, to

implement a risk-based program reasonably designed to prevent money laundering and to combat the financing of terrorism,

including through suspicious activity and currency transaction reporting, compliance, record-keeping and due diligence on

customers.

The Patriot Act also contains financial transparency laws and enhanced information collection tools and enforcement mechanisms

for the U.S. government, including: due diligence and record-keeping requirements for private banking and correspondent accounts;

standards for verifying customer identification at account opening; and rules to produce certain records upon request of a regulator

or law enforcement and to promote cooperation among financial institutions, regulators, and law enforcement in identifying parties

that may be involved in terrorism, money laundering and other crimes.

Funding

Under the Federal Deposit Insurance Corporation Improvement Act of 1991 (“FDICIA”), as discussed in “MD&A—Liquidity

Risk Profile,” only well-capitalized and adequately-capitalized institutions may accept brokered deposits. Adequately-capitalized

institutions, however, must first obtain a waiver from the FDIC before accepting brokered deposits, and such deposits may not

pay rates that significantly exceed the rates paid on deposits of similar maturity from the institution’s normal market area or, for

deposits from outside the institution’s normal market area, the national rate on deposits of comparable maturity. The FDIC is

authorized to terminate a bank’s deposit insurance upon a finding by the FDIC that the bank’s financial condition is unsafe or

unsound or that the institution has engaged in unsafe or unsound practices or has violated any applicable rule, regulation, order or

condition enacted or imposed by the bank’s regulatory agency. The termination of deposit insurance for a bank could have a material

adverse effect on its liquidity and its earnings.

For any of our funding conducted through securitization, in addition to the credit risk retention provision requiring a securitizer

to retain a portion of the credit risk of an asset-backed securitization, the Dodd-Frank Act also prohibits conflicts of interest relating

to securitizations.

Nonbank Activities

Certain of our nonbank subsidiaries are subject to supervision and regulation by various other federal and state authorities. Capital

One Securities, Inc. and Capital One Investing, LLC (formerly known as Capital One Sharebuilder, Inc.) are registered broker-