Capital One 2015 Annual Report Download - page 232

Download and view the complete annual report

Please find page 232 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

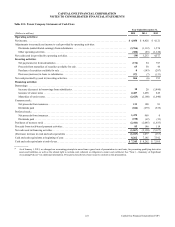

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

213 Capital One Financial Corporation (COF)

Mortgage Representation and Warranty Liabilities

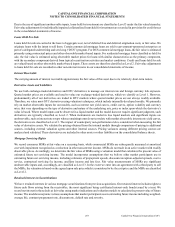

We acquired three subsidiaries that originated residential mortgage loans and sold these loans to various purchasers, including

purchasers who created securitization trusts. These subsidiaries are Capital One Home Loans, LLC, which was acquired in February

2005; GreenPoint, which was acquired in December 2006 as part of the North Fork acquisition; and CCB, which was acquired in

February 2009 and subsequently merged into CONA (collectively, the “subsidiaries”).

In connection with their sales of mortgage loans, the subsidiaries entered into agreements containing varying representations and

warranties about, among other things, the ownership of the loan, the validity of the lien securing the loan, the loan’s compliance

with any applicable loan criteria established by the purchaser, including underwriting guidelines and the existence of mortgage

insurance, and the loan’s compliance with applicable federal, state and local laws. The representations and warranties do not address

the credit performance of the mortgage loans, but mortgage loan performance often influences whether a claim for breach of

representation and warranty will be asserted and has an effect on the amount of any loss in the event of a breach of a representation

or warranty.

Each of these subsidiaries may be required to repurchase mortgage loans in the event of certain breaches of these representations

and warranties. In the event of a repurchase, the subsidiary is typically required to pay the unpaid principal balance of the loan

together with interest and certain expenses (including, in certain cases, legal costs incurred by the purchaser and/or others). The

subsidiary then recovers the loan or, if the loan has been foreclosed, the underlying collateral. The subsidiary is exposed to any

losses on the repurchased loans, taking into account any recoveries on the collateral. In some instances, rather than repurchase the

loans, a subsidiary may agree to make cash payments to make an investor whole on losses or to settle repurchase claims, possibly

including claims for attorneys’ fees and interest. In addition, our subsidiaries may be required to indemnify certain purchasers and

others against losses they incur as a result of certain breaches of representations and warranties.

These subsidiaries, in total, originated and sold to non-affiliates approximately $111 billion original principal balance of mortgage

loans between 2005 and 2008, which are the years (or “vintages”) with respect to which our subsidiaries have received the vast

majority of the repurchase-related requests and other related claims.

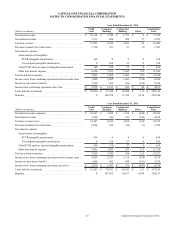

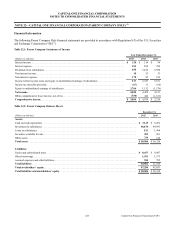

The following table presents the original principal balance of mortgage loan originations, by vintage for 2005 through 2008, for

the three general categories of purchasers of mortgage loans and the estimated unpaid principal balance as of December 31, 2015

and 2014:

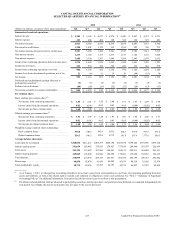

Table 21.1: Unpaid Principal Balance of Mortgage Loans Originated and Sold to Third Parties Based on Category of Purchaser

Estimated Unpaid Principal Balance Original Principal Balance

(Dollars in billions)

December 31,

2015

December 31,

2014 Total 2008 2007 2006 2005

GSEs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 2 $ 3 $ 11 $ 1 $ 4 $ 3 $ 3

Insured Securitizations. . . . . . . . . . . . . . . . . . . . . . . 44 20 0 2 8 10

Uninsured Securitizations and Other. . . . . . . . . . . . 14 16 80 3 15 30 32

Total. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 20 $ 23 $ 111 $ 4 $ 21 $ 41 $ 45

Between 2005 and 2008, our subsidiaries sold an aggregate amount of $11 billion in original principal balance mortgage loans to

the GSEs.

Of the $20 billion in original principal balance of mortgage loans sold directly by our subsidiaries to private-label purchasers who

placed the loans into securitizations supported by bond insurance (“Insured Securitizations”), approximately 48% of the original

principal balance was covered by bond insurance. Further, approximately $16 billion original principal balance was placed in

securitizations as to which the monoline bond insurers have made repurchase-related requests or loan file requests to one of our

subsidiaries (“Active Insured Securitizations”) and the remaining approximately $4 billion original principal balance was placed

in securitizations as to which the monoline bond insurers have not made repurchase-related requests or loan file requests to one

of our subsidiaries (“Inactive Insured Securitizations”). Insured Securitizations often allow the monoline bond insurer to act

independently of the investors. Bond insurers typically have indemnity agreements directly with both the mortgage originators

and the securitizers, and they often have super-majority rights within the trust documentation that allow them to direct trustees to

pursue mortgage repurchase-related requests without coordination with other investors.