Capital One 2015 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

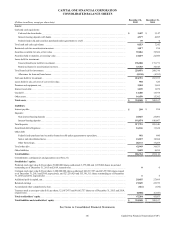

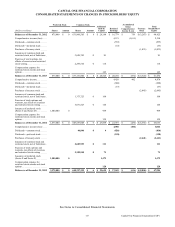

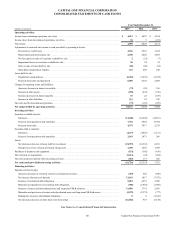

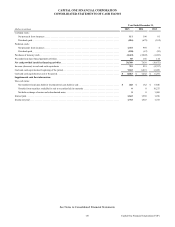

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

126 Capital One Financial Corporation (COF)

Charge-Offs

We charge-off loans as a reduction to the allowance for loan and lease losses when we determine the loan is uncollectible and

record subsequent recoveries of previously charged off amounts as an increase to the allowance for loan and lease losses. We

exclude accrued and unpaid finance charges and fees and fraud losses from charge-offs. Costs to recover charged-off loans are

recorded as collection expense and included in our consolidated statements of income as a component of other non-interest expense

as incurred. Our charge-off time frames for loans by loan type are presented below.

• Credit card loans: We generally charge-off credit card loans in the period the account becomes 180 days past due. We charge

off delinquent credit card loans for which revolving privileges have been revoked as part of loan workout when the account

becomes 120 days past due. Credit card loans in bankruptcy are generally charged-off by the end of the month following

30 days after the receipt of a complete bankruptcy notification from the bankruptcy court. Credit card loans of deceased

account holders are charged-off by the end of the month following 60 days of receipt of notification.

• Consumer banking loans: We generally charge-off consumer banking loans at the earlier of the date when the account is a

specified number of days past due or upon repossession of the underlying collateral. Our charge-off time frame is 180 days

for home loans and 120 days for auto and other consumer installment loans. Small business banking loans generally charge

off at 90 or 120 days past due based on when unpaid principal loan amounts are deemed uncollectible. We calculate the

initial charge-off amount for home loans based on the excess of our recorded investment in the loan over the fair value of

the underlying property less estimated selling costs as of the date of the charge-off. We update our home value estimates

on a regular basis and may recognize additional charge-offs for subsequent declines in home values. Consumer loans in

bankruptcy, except for auto and home loans, generally are charged-off within 40 days of receipt of notification from the

bankruptcy court. Auto and home loans where the borrower has filed for Chapter 11 bankruptcy are generally charged-off

in the period that the loan is both 60 days or more past due and 60 days or more past the bankruptcy notification date. Auto

and home loans where the borrower has filed for Chapter 7 bankruptcy are charged off by the end of the month in which

the bankruptcy notification is received. Consumer loans of deceased account holders are charged-off by the end of the month

following 60 days of receipt of notification.

• Commercial banking loans: We charge-off commercial loans in the period we determine that the unpaid principal loan

amounts are uncollectible.

• Acquired Loans: We do not record charge-offs on Acquired Loans that are performing in accordance with or better than our

expectations as of the date of acquisition, as the fair values of these loans already reflect a discount for expected future

credit losses. We record charge-offs on Acquired Loans only if actual losses exceed estimated credit losses incorporated

into the fair value recorded at acquisition.

Allowance for Loan and Lease Losses

We maintain an allowance for loan and lease losses (“allowance”) that represents management’s best estimate of incurred loan

and lease losses inherent in our held for investment portfolio as of each balance sheet date. The provision for credit losses, which

is charged to income, reflects credit losses we believe have been incurred and will eventually be reflected over time in our charge-

offs. Charge-offs of uncollectible amounts are deducted from the allowance and subsequent recoveries are added back.

Management performs a quarterly analysis of our loan portfolio to determine if impairment has occurred and to assess the adequacy

of the allowance based on historical and current trends as well as other factors affecting credit losses. We apply documented

systematic methodologies to separately calculate the allowance for our consumer loan and commercial loan portfolios and for

loans within each of these portfolios that we identify as individually impaired. Our allowance for loan and lease losses consists of

three components that are allocated to cover the estimated probable losses in each loan portfolio based on the results of our detailed

review and loan impairment assessment process: (i) a component for loans collectively evaluated for impairment; (ii) an asset-

specific component for individually impaired loans; and (iii) a component related to Acquired Loans that have experienced

significant decreases in expected cash flows subsequent to acquisition. Each of our allowance components is supplemented by an

amount that represents management’s qualitative judgment of the imprecision and risks inherent in the processes and assumptions

used in establishing the allowance. Management’s judgment involves an assessment of subjective factors, such as process risk,

modeling assumption and adjustment risks and probable internal and external events that will likely impact losses.

Our consumer loan portfolio consists of smaller-balance, homogeneous loans, divided into four primary portfolio segments: credit

card loans, auto loans, residential home loans and retail banking loans. Each of these portfolios is further divided by our business