Capital One 2015 Annual Report Download - page 125

Download and view the complete annual report

Please find page 125 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

106 Capital One Financial Corporation (COF)

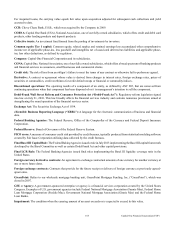

Impaired loans: A loan is considered impaired when, based on current information and events, it is probable that we will not be

able to collect all amounts due from the borrower in accordance with the original contractual terms of the loan.

Inactive Insured Securitizations: Securitizations as to which the monoline bond insurers have not made repurchase-related

requests or loan file requests to one of our subsidiaries.

ING Direct acquisition: On February 17, 2012, we completed the acquisition of substantially all of the ING Direct business in

the United States (“ING Direct”) from ING Groep N.V., ING Bank N.V., ING Direct N.V. and ING Direct Bancorp.

Insured securitizations: Securitizations supported by bond insurance.

Interest rate sensitivity: The exposure to interest rate movements.

Interest rate swaps: Contracts in which a series of interest rate flows in a single currency are exchanged over a prescribed period.

Interest rate swaps are the most common type of derivative contract that we use in our asset/liability management activities.

Investment grade: Represents Moody’s long-term rating of Baa3 or better; and/or a Standard & Poor’s, Fitch or DBRS long-term

rating of BBB- or better; or if unrated, an equivalent rating using our internal risk ratings. Instruments that fall below these levels

are considered to be non-investment grade.

Investments in Qualified Affordable Housing Projects: Capital One invests in private investment funds that make equity

investments in multifamily affordable housing properties that provide affordable housing tax credits for these investments. The

activities of these entities are financed with a combination of invested equity capital and debt.

Investor entities: Entities that invest in community development entities (“CDE”) that provide debt financing to businesses and

non-profit entities in low-income and rural communities.

Leverage ratio (Basel I guideline): Tier 1 capital divided by average assets after certain adjustments, as defined by the regulators.

Liquidity risk: The risk that the Company will not be able to meet its future financial obligations as they come due, or invest in

future asset growth because of an inability to obtain funds at a reasonable price within a reasonable time period.

Loan-to-value (“LTV”) ratio: The relationship expressed as a percentage, between the principal amount of a loan and the appraised

value of the collateral (i.e., residential real estate, autos, etc.) securing the loan.

Managed presentation: A non-GAAP presentation of financial results that includes reclassifications to present revenue on a fully

taxable-equivalent basis. Management uses this non-GAAP financial measure at the segment level, because it believes this provides

information to enable investors to understand the underlying operational performance and trends of the particular business segment

and facilitates a comparison of the business segment with the performance of competitors.

Market risk: The risk that an institution’s earnings or the economic value of equity could be adversely impacted by changes in

interest rates, foreign exchange rates or other market factors.

Master netting agreement: An agreement between two counterparties that have multiple contracts with each other that provides

for the net settlement of all contracts through a single payment in the event of default or termination of any one contract.

Mortgage-backed security (“MBS”): An asset-backed security whose cash flows are backed by the principal and interest payments

of a set of mortgage loans.

Mortgage servicing rights (“MSR”): The right to service a mortgage loan when the underlying loan is sold or securitized.

Servicing includes collections for principal, interest and escrow payments from borrowers and accounting for and remitting principal

and interest payments to investors.

Net interest margin: The result of dividing net interest income by average interest-earning assets.

Nonperforming loans and leases: Loans and leases that have been placed on non-accrual status.

North Fork: North Fork Bancorporation, Inc., which was acquired by the Company in 2006.

Operational risk: The risk of loss, capital impairment, adverse customer experience or reputational impact resulting from failure

to comply with policies and procedures, failed internal processes or systems, or from external events.

Option-ARM loans: The option-ARM real estate loan product is an adjustable-rate mortgage loan that initially provides the

borrower with the monthly option to make a fully-amortizing, interest-only or minimum fixed payment. After the initial payment

option period, usually five years, the recalculated minimum payment represents a fully-amortizing principal and interest payment

that would effectively repay the loan by the end of its contractual term.