Capital One 2015 Annual Report Download - page 166

Download and view the complete annual report

Please find page 166 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

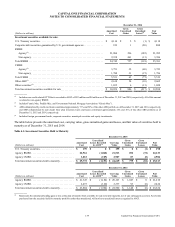

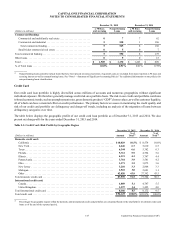

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

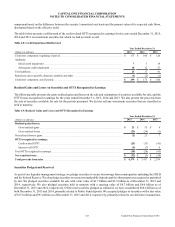

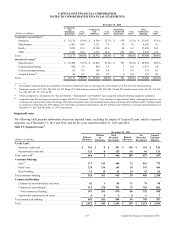

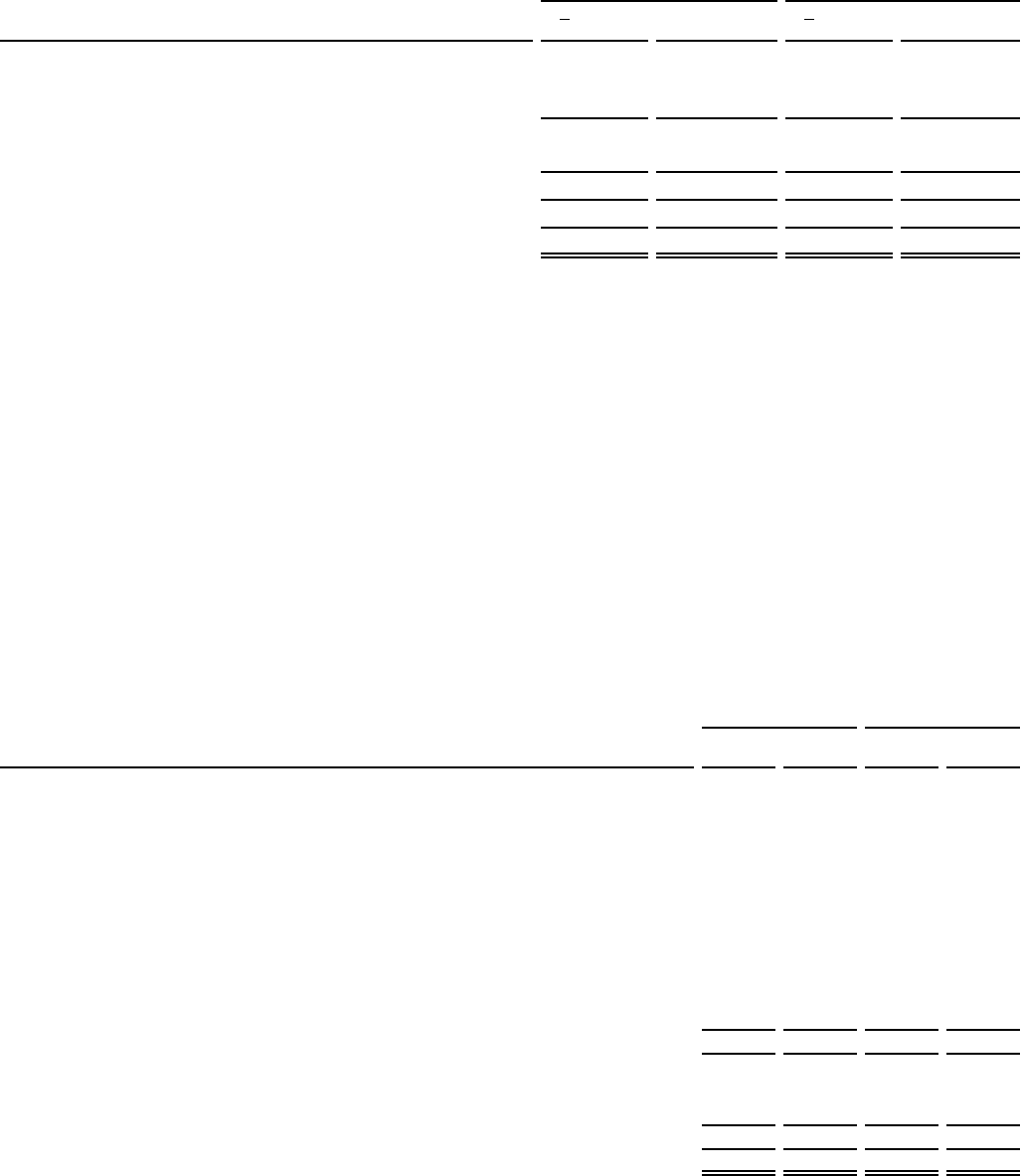

147 Capital One Financial Corporation (COF)

December 31, 2015 December 31, 2014

(Dollars in millions)

> 90 Days

and Accruing

Nonperforming

Loans

> 90 Days

and Accruing

Nonperforming

Loans

Commercial Banking:

Commercial and multifamily real estate . . . . . . . . . . . . . . . . . . . . . . . . 0 7 7 62

Commercial and industrial . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 538 1 106

Total commercial lending. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 545 8 168

Small-ticket commercial real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . 0 5 0 7

Total commercial banking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5 550 8 175

Other loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0 9 0 15

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 1,505 $ 1,170 $ 1,263 $ 809

% of Total loans . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 0.65% 0.51% 0.61% 0.39%

__________

(1) Nonperforming loans generally include loans that have been placed on nonaccrual status. Acquired Loans are excluded from loans reported as 90 days and

accruing interest as well as nonperforming loans. See “Note 1—Summary of Significant Accounting Policies” for additional information on our policies for

non-performing loans classification.

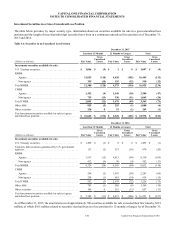

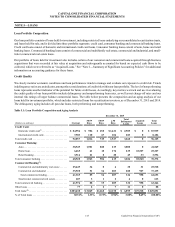

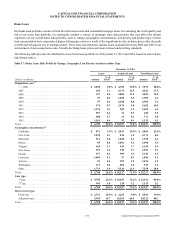

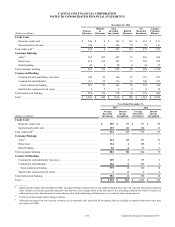

Credit Card

Our credit card loan portfolio is highly diversified across millions of accounts and numerous geographies without significant

individual exposure. We therefore generally manage credit risk on a portfolio basis. The risk in our credit card portfolio correlates

to broad economic trends, such as unemployment rates, gross domestic product (“GDP”), home values, as well as customer liquidity,

all of which can have a material effect on credit performance. The primary factors we assess in monitoring the credit quality and

risk of our credit card portfolio are delinquency and charge-off trends, including an analysis of the migration of loans between

delinquency categories over time.

The table below displays the geographic profile of our credit card loan portfolio as of December 31, 2015 and 2014. We also

present net charge-offs for the years ended December 31, 2015 and 2014.

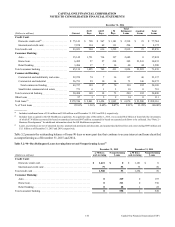

Table 5.3: Credit Card: Risk Profile by Geographic Region

December 31, 2015 December 31, 2014

(Dollars in millions) Amount

% of

Total(1) Amount

% of

Total(1)

Domestic credit card:

California . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 10,029 10.5% $ 8,574 10.0%

New York . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,446 6.7 5,610 6.5

Texas . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6,344 6.6 5,382 6.3

Florida . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5,712 5.9 4,794 5.6

Illinois . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,121 4.3 3,747 4.4

Pennsylvania . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,764 3.9 3,581 4.2

Ohio. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,371 3.5 3,075 3.6

New Jersey . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,210 3.3 2,868 3.3

Michigan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2,922 3.0 2,681 3.1

Other . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42,020 43.8 37,392 43.5

Total domestic credit card . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87,939 91.5 77,704 90.5

International credit card:

Canada. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4,889 5.1 4,747 5.5

United Kingdom . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3,297 3.4 3,425 4.0

Total international credit card. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8,186 8.5 8,172 9.5

Total credit card . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 96,125 100.0% $ 85,876 100.0%

__________

(1) Percentages by geographic region within the domestic and international credit card portfolios are calculated based on the total held for investment credit card

loans as of the end of the reported period.