Capital One 2015 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

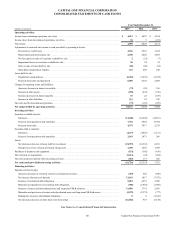

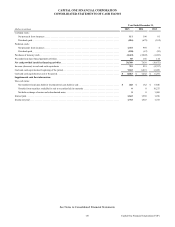

|

|

CAPITAL ONE FINANCIAL CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

123 Capital One Financial Corporation (COF)

Loans Held for Investment

Loans that we have the ability and intent to hold for the foreseeable future and loans associated with on-balance sheet securitization

transactions accounted for as secured borrowings are classified as held for investment. Loans classified as held for investment,

except Acquired Loans accounted for based upon expected cash flows described below, are reported at their amortized cost, which

is the outstanding principal balance, net of any unearned income, unamortized deferred fees and costs, unamortized premiums and

discounts and charge-offs. Credit card loans also include billed finance charges and fees, net of the estimated uncollectible amount.

Interest income is recognized on loans held for investment on an accrual basis. We generally defer certain loan origination fees

and direct loan origination costs on originated loans, premiums and discounts on purchased loans and loan commitment fees. We

recognize these amounts in interest income as yield adjustments over the life of the loan and/or commitment period using the

effective interest method. Where appropriate, prepayment estimates are factored into the calculation of the constant effective yield

necessary to apply the interest method. Prepayment estimates are based on historical prepayment data and existing and forecasted

interest rates and economic data. For credit card loans, loan origination fees and direct loan origination costs are amortized on a

straight-line basis over a 12-month period. We establish an allowance for loan losses for probable losses inherent in our held for

investment loan portfolio as of each balance sheet date. Loans held for investment are subject to our allowance for loan and lease

losses methodology described below under “Allowance for Loan and Lease Losses.”

Loans Held for Sale

Loans purchased or originated with the intent to sell or for which we do not have the ability and intent to hold for the foreseeable

future are classified as held for sale. Interest on these loans is recognized on an accrual basis. These loans are recorded at the lower

of amortized cost or fair value. Loan origination fees and direct loan origination costs are deferred until the loan is sold and are

then recognized as part of the total gain or loss on sale.

If a loan is transferred from held for investment to held for sale, declines in fair value related to credit are recorded as a charge-

off and amortization of deferred loan origination fees and costs ceases. Subsequent to transfer, we report write-downs or recoveries

in fair value up to the carrying value at the date of transfer and realized gains or losses on loans held for sale in our consolidated

statements of income as a component of other non-interest income. We calculate the gain or loss on loan sales as the difference

between the proceeds received and the carrying value of the loans sold, net of the fair value of any retained servicing rights.

Loans Acquired

All purchased loans, including loans transferred in a business combination, acquired on or after January 1, 2009, are initially

recorded at fair value, which includes consideration of expected future losses, as of the date of the acquisition. We account for

purchased loans using the guidance for accounting for purchased credit-impaired loans and debt securities, which is based upon

expected cash flows, if the purchased loans have a discount attributable, at least in part, to credit deterioration and they are not

specifically scoped out of the guidance. We refer to these purchased loans that are subsequently accounted for based on expected

cash flows to be collected in accordance with Accounting Standard Codification (“ASC”) 310-30, Loans and Debt Securities

Acquired with Deteriorated Credit Quality (formerly known as “Statement of Position 03-3, Accounting for Certain Loans or Debt

Securities Acquired in a Transfer,” commonly referred to as “SOP 03-3”) as “Acquired Loans” or “PCI loans.” Other purchased

loans that don’t meet our criteria described above are accounted for based on contractual cash flows.

Loans Acquired and Accounted for Based on Expected Cash Flows

In accounting for purchased loans based on expected cash flows, we first determine the contractually required payments due, which

represent the total undiscounted amount of all uncollected principal and interest payments, adjusted for the effect of estimated

prepayments. We then estimate the undiscounted cash flows we expect to collect, incorporating several key assumptions including

expected default rates, loss severities and the amount and timing of prepayments. We estimate the fair value by discounting the

estimated cash flows we expect to collect using an observable market rate of interest, when available, adjusted for factors that a

market participant would consider in determining fair value. We may aggregate loans acquired in the same fiscal quarter into one

or more pools if the loans have common risk characteristics. A pool is then accounted for as a single asset, with a single composite

interest rate and an aggregate fair value and expected cash flows.

The excess of cash flows expected to be collected over the estimated fair value of purchased loans is referred to as the accretable

yield. This amount is not recorded on our consolidated balance sheets, but is accreted into interest income over the life of the loan,