Capital One 2015 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2015 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

|

|

85 Capital One Financial Corporation (COF)

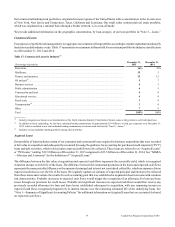

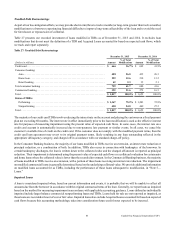

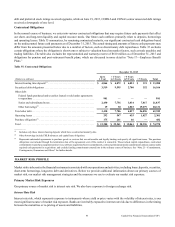

Troubled Debt Restructurings

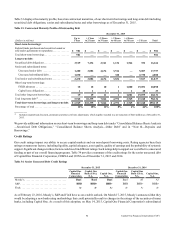

As part of our loss mitigation efforts, we may provide short-term (three to twelve months) or long-term (greater than twelve months)

modifications to a borrower experiencing financial difficulty to improve long-term collectability of the loan and to avoid the need

for foreclosure or repossession of collateral.

Table 27 presents our recorded investment of loans modified in TDRs as of December 31, 2015 and 2014. It excludes loan

modifications that do not meet the definition of a TDR and Acquired Loans accounted for based on expected cash flows, which

we track and report separately.

Table 27: Troubled Debt Restructurings

December 31, 2015 December 31, 2014

(Dollars in millions) Amount

% of Total

Modifications Amount

% of Total

Modifications

Credit card. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 666 36.7% $ 692 41.9%

Consumer banking:

Auto . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 488 26.8 435 26.3

Home loan . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 229 12.6 218 13.2

Retail banking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42 2.3 35 2.1

Total consumer banking . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 759 41.7 688 41.6

Commercial banking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 392 21.6 272 16.5

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 1,817 100.0% $ 1,652 100.0%

Status of TDRs:

Performing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 1,367 75.2% $ 1,203 72.8%

Nonperforming . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 450 24.8 449 27.2

Total . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $ 1,817 100.0% $ 1,652 100.0%

The majority of our credit card TDRs involve reducing the interest rate on the account and placing the customer on a fixed payment

plan not exceeding 60 months. The interest rate in effect immediately prior to the loan modification is used as the effective interest

rate for purposes of measuring impairment using the present value of expected cash flows. In some cases, the interest rate on a

credit card account is automatically increased due to non-payment, late payment or similar events. In all cases, we cancel the

customer’s available line of credit on the credit card. If the customer does not comply with the modified payment terms, then the

credit card loan agreement may revert to its original payment terms, likely resulting in any loan outstanding reflected in the

appropriate delinquency category, and charged off in accordance with our standard charge-off policy.

In the Consumer Banking business, the majority of our loans modified in TDRs receive an extension, an interest rate reduction or

principal reduction, or a combination of both. In addition, TDRs also occur in connection with bankruptcy of the borrower. In

certain bankruptcy discharges, the loan is written down to the collateral value and the charged off amount is reported as principal

reduction. Their impairment is determined using the present value of expected cash flows or a collateral evaluation for certain auto

and home loans where the collateral value is lower than the recorded investment. In the Commercial Banking business, the majority

of loans modified in TDRs receive an extension, with a portion of these loans receiving an interest rate reduction. The impairment

on modified commercial loans is generally determined based on the underlying collateral value. We provide additional information

on modified loans accounted for as TDRs, including the performance of those loans subsequent to modification, in “Note 5—

Loans.”

Impaired Loans

A loan is considered impaired when, based on current information and events, it is probable that we will be unable to collect all

amounts due from the borrower in accordance with the original contractual terms of the loan. Generally, we report loans as impaired

based on the method for measuring impairment in accordance with applicable accounting guidance. Loans defined as individually

impaired include larger balance commercial nonperforming loans and TDRs. Loans held for sale are not reported as impaired, as

these loans are recorded at lower of cost or fair value. Impaired loans also exclude Acquired Loans accounted for based on expected

cash flows because this accounting methodology takes into consideration future credit losses expected to be incurred.