Sallie Mae 2005 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

81

Purchased Paper—Non-Mortgage

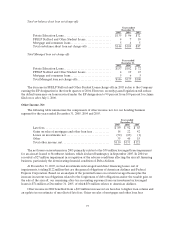

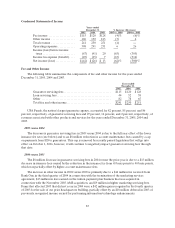

Years ended

December 31,

2005 2004(1)

Face value ofpurchases.................................... $2,830 $426

Purchase price............................................ 198 19

% of face value purchased ................................. 7.0% 4.5%

Gross Cash Collections (“GCC”) ........................... $ 250 $ 59

Collections revenue ....................................... 157 39

% of GCC ............................................... 63% 66%

Carrying value of purchases................................ $ 158 $ 52

(1) AFS was purchased in September 2004. Prior to this acquisition, the Company was not in the

purchased paper business.

The amount of face value of purchases in any quarter is a function of a combination of factors

including the amount of receivables available for purchase in the marketplace, average age of each

portfolio, the asset class of the receivables, and competition in the marketplace. As a result, the percentage

of principal purchased will vary from quarter to quarter. The decrease in purchase paper revenue as a

percentage of GCC can primarily be attributed to the increase in new portfolio purchases in the second

half of 2005. Typically, revenue recognition based on a portfolio’s effective interest rate is a lower

percentage of cash collections in the early stages of servicing a portfolio.

Purchased Paper—Mortgage/Properties

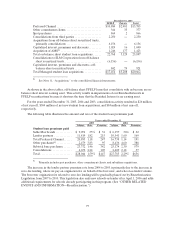

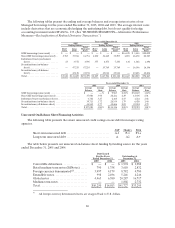

Year ended

December 31, 2005(1)

Face value ofpurchases..................................... $165

Collections revenue ........................................ 10

Collateral value of purchases................................ 232

Purchase price............................................. 141

% of collateral value ....................................... 61%

Carrying value of purchases................................. $298

(1) GRP was purchased in August 2005. Prior to this acquisition, the Company was not in the mortgage

purchased paper business.

The purchase price for sub-performing and non-performing mortgage loans is generally determined as

a percentage of the underlying collateral. Fluctuations in the purchase price as a percentage of collateral

value can be caused by a number of factors including the percentage of second mortgages in the portfolio

and the level of private mortgage insurance associated with particular assets.