Sallie Mae 2005 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

51

Company’s core business activities. ‘‘Core earnings’’ reflect only current period adjustments to GAAP, as

described in the more detailed discussion of the differences between GAAP and ‘‘core earnings’’ that

follows, which includes further detail on each specific adjustments required to reconcile our ‘‘core

earnings’’ segment presentation to our GAAP earnings.

1) Securitization Accounting: Under GAAP, certain securitization transactions in our Lending operating

segment are accounted for as sales of assets. Under “core earnings” for the Lending operating

segment, we present all securitization transactions on a Managed Basis as long-term non-recourse

financings. The upfront “gains” on sale from securitization transactions as well as ongoing “servicing

and securitization revenue” presented in accordance with GAAP are excluded from “core earnings”

and are replaced by the interest income, provisions for loan losses, and interest expense as they are

earned or incurred on the securitization loans. We also exclude transactions with our off-balance sheet

trusts from “core earnings” as they are considered intercompany transactions on a Managed Basis.

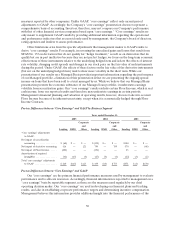

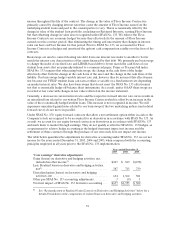

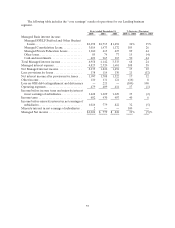

The following table summarizes “core earnings” securitization adjustments for the Lending operating

segment the years ended December 31, 2005, 2004 and 2003.

Years Ended December 31,

2005 2004 2003

“Core earnings” securitization adjustments:

Net interest income on securitized loans, after provisions

forlosses ....................................... $ (935) $ (1,065) $ (1,104)

Gains on student loan securitizations................. 552 375 744

Servicingand securitization revenue.................. 357 561 667

Intercompany transactions with off-balance sheet trusts. (34) (23) (7)

Total “core earnings” securitization adjustments ....... $ (60) $ (152) $ 300

2) Derivative Accounting: “Core earnings” exclude periodic unrealized gains and losses arising primarily

in our Lending operating segment, and to a lesser degree in our Corporate and Other reportable

segment, that are caused primarily by the one-sided mark-to-market derivative valuations prescribed

by SFAS No. 133 on derivatives that do not qualify for “hedge treatment” under GAAP. Under “core

earnings,” we recognize the economic effect of these hedges, which generally results in any cash paid

or received being recognized ratably as an expense or revenue over the hedged item’s life. “Core

earnings” also exclude the gain or loss on equity forward contracts that under SFAS No. 133, are

required to be accounted for as derivatives and are marked-to-market through earnings.

SFAS No. 133 requires that changes in the fair value of derivative instruments be recognized currently

in earnings unless specific hedge accounting criteria, as specified by SFAS No. 133, are met. We

believe that our derivatives are effective economic hedges, and as such, are a critical element of our

interest rate risk management strategy. However, some of our derivatives, primarily Floor Income

Contracts, certain Eurodollar futures contracts and certain basis swaps and equity forward contracts

(discussed in detail below), do not qualify for “hedge treatment” as defined by SFAS No. 133, and the

stand-alone derivative must be marked-to-market in the income statement with no consideration for

the corresponding change in fair value of the hedged item. “Gains (losses) on derivative and hedging

activities, net” are primarily caused by interest rate volatility, changing credit spreads and changes in

our stock price during the period as well as the volume and term of derivatives not receiving hedge

treatment.

Our Floor Income Contracts are written options which must meet more stringent requirements than

other hedging relationships to achieve hedge effectiveness under SFAS No. 133. Specifically, our

Floor Income Contracts do not qualify for hedge accounting treatment because the paydown of

principal of the student loans underlying the Floor Income embedded in those student loans does not

exactly match the change in the notional amount of our written Floor Income Contracts. Under SFAS

No. 133, the upfront payment is deemed a liability and changes in fair value are recorded through