Sallie Mae 2005 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

34

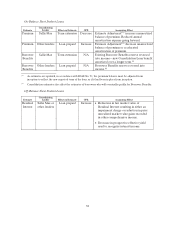

The impact of Borrower Benefits is dependent on the estimate of the number of borrowers who will

eventually qualify for these benefits. For competitive purposes, we occasionally change Borrower Benefits

programs in both amount and qualification factors. These programmatic changes must be reflected in the

estimate of the Borrower Benefits discount.

Securitization Accounting and Retained Interests

We regularly engage in securitization transactions as part of our financing strategy (see also

“LIQUIDITY AND CAPITAL RESOURCES—Securitization Activities”). In a securitization, we sell

student loans to a trust that issues bonds backed by the student loans as part of the transaction. When our

securitizations meet the sale criteria of SFAS No. 140, “Accounting for Transfers and Servicing of

Financial Assets and Extinguishments of Liabilities—a Replacement of SFAS No. 125,” we record a gain

on the sale of the student loans, which is the difference between the allocated cost basis of the assets sold

and the relative fair value of the assets received. The primary judgment in determining the fair value of the

assets received is the valuation of the Residual Interest.

The Residual Interests in each of our securitizations are treated as available-for-sale securities in

accordance with SFAS No. 115, “Accounting for Certain Investments in Debt and Equity Securities,” and

therefore must be marked-to-market with temporary unrealized gains and losses recognized, net of tax, in

accumulated other comprehensive income in stockholders’ equity. Since there are no quoted market prices

for our Residual Interests, we estimate their fair value both initially and each subsequent quarter using the

key assumptions listed below:

•the projected net interest yield from the underlying securitized loans, which can be impacted by the

forward yield curve, as well as the Borrower Benefits program;

•the calculation of the Embedded Floor Income associated with the securitized loan portfolio;

• the CPR;

•the discount rate used, which is intended to be commensurate with the risks involved; and

•the expected credit losses from the underlying securitized loan portfolio.

We recognize interest income and periodically evaluate our Residual Interests for other than

temporary impairment in accordance with the Emerging Issues Task Force (“EITF”) Issue No. 99-20,

“Recognition of Interest Income and Impairment on Purchased and Residual Beneficial Interests in

Securitized Financial Assets.” Under this standard, each quarter we estimate the remaining cash flows to

be received from our Retained Interests and use these revised cash flows to prospectively calculate a yield

for income recognition. In cases where our estimate of future cash flows results in a lower yield from that

used to recognize interest income in the prior quarter, the Residual Interest is written down to fair value,

first to the extent of any unrealized gain in accumulated other comprehensive income, then through

earnings as an other than temporary impairment, and the yield used to recognize subsequent income from

the trust is negatively impacted.

We also receive income for servicing the loans in our securitization trusts. We assess the amounts

received as compensation for these activities at inception and on an ongoing basis to determine if the

amounts received are adequate compensation as defined in SFAS No. 140. To the extent such

compensation is determined to be no more or less than adequate compensation, no servicing asset or

obligation is recorded.

Provisions for Loan Losses

We maintain an allowance for loan losses at an amount sufficient to absorb losses inherent in our

FFELP and Private Education Loan portfolios at the reporting date based on a projection of estimated