Sallie Mae 2005 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

35

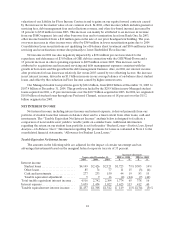

probable net credit losses. The maturing of our Private Education Loan portfolios has provided us with

more historical data on borrower default behavior such that we now analyze those portfolios to determine

the effects that the various stages of delinquency have on borrower default behavior and ultimate charge-

off. As a result, in the second quarter of 2005, we changed our estimate of the allowance for loan losses for

our Managed loan portfolio to include a migration analysis of delinquent and current accounts, in addition

to other considerations. A migration analysis is a technique used to estimate the likelihood that a loan

receivable may progress through the various delinquency stages and ultimately charge-off, and is a widely

used reserving methodology in the consumer finance industry. Previously, we calculated the allowance for

Private Education Loan losses by estimating the probable losses in the portfolio based primarily on loan

characteristics and where pools of loans were in their life, with less emphasis on current delinquency status

of the loan. Also, in our prior methodology for calculating the allowance, some Private Education Loan

loss rates were based on proxies and extrapolations of FFELP loan loss data.

We also transitioned to a migration analysis to revise our estimated losses associated with accrued

interest income. Under the new methodology, we estimate the amount of uncollectible accrued interest on

Private Education Loans and write it off against current period interest income. Under our prior

methodology, Private Education Loans continued to accrue interest, even during periods of forbearance,

until they were charged off, at which time, the loans were placed on non-accrual status and all previously

accrued interest was reversed against income in the month of charge-off. The allowance for loan losses

provided for a portion of the probable losses in accrued interest receivable prior to charge-off.

This change in reserving methodology has been accounted for as a change in estimate in accordance

with the Accounting Principles Board (“APB”) Opinion No. 20, “Accounting Changes.” The effect of this

change in estimate was to increase the allowance by $40 million and to reduce student loan interest income

for the estimate of uncollectible accrued interest receivable by $14 million. On the income statement,

adjustments to the allowance are recorded through the provisions for losses whereas adjustments to

accrued interest are recorded in interest income.

When calculating the Private Education Loan loss reserve, we divide the portfolio into categories of

similar risk characteristics based on loan program type, loan status (in-school, grace, repayment,

forbearance, delinquency), underwriting criteria, existence or absence of a co-borrower, and aging. We

then apply default and collection rate projections to each category. Our higher education Private

Education Loan programs (89 percent of the Managed Private Education Loan portfolio at December 31,

2005) do not require the borrowers to begin repayment until six months after they have graduated or

otherwise left school. Consequently, our loss estimates for these programs are minimal while the borrower

is in school. Our career training and alternative Private Education Loan programs (11 percent of the

Managed Private Education Loan portfolio at December 31, 2005) generally require the borrowers to start

repaying their loans immediately. At December 31, 2005, 46 percent of the principal balance in the higher

education Managed Private Education Loan portfolio related to borrowers who are still in-school and not

required to make payments. As the current portfolio ages, an increasing percentage of the borrowers will

leave school and be required to begin payments on their loans. The allowance for losses will change

accordingly with the percentage of borrowers in repayment.

Our loss estimates include losses to be incurred generally over a two year loss confirmation period.

Similar to the rules governing FFELP payment requirements, our collection policies allow for periods of

nonpayment for borrowers requesting additional payment grace periods upon leaving school or

experiencing temporary difficulty meeting payment obligations. This is referred to as forbearance status.

The majority of forbearance occurs early in the repayment term when borrowers are starting their careers

(see “LENDING BUSINESS SEGMENT—Private Education Loans—Delinquencies”). At December 31,

2005, 10 percent of the Managed Private Education Loan portfolio in repayment and forbearance was in

forbearance status. The loss confirmation period is in alignment with our typical collection cycle and takes

into account these periods of nonpayment.