Sallie Mae 2005 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

33

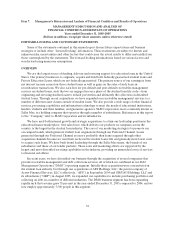

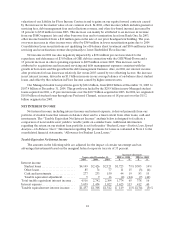

In December 2004, we completed the Wind-Down of the GSE through the defeasance of all

remaining GSE debt obligations and dissolution of the GSE’s federal charter. The liquidity provided to the

Company by the GSE has been replaced primarily by securitizations. In addition to securitizations, we have

also increased and diversified our investor base over the last three years to enable us to access a number of

additional sources of liquidity including an asset-backed commercial paper program, unsecured revolving

credit facilities, and other unsecured corporate debt and equity security issuances.

We manage our business through two primary operating segments: the Lending operating segment

and the DMO operating segment. Accordingly, the results of operations of the Company’s Lending and

DMO operating segments are presented separately below under “BUSINESS SEGMENTS.” These

operating segments are considered reportable segments under the Financial Accounting Standards Board’s

(“FASB”) Statement of Financial Accounting Standards (“SFAS”) No. 131, “Disclosures about Segments

of an Enterprise and Related Information,” based on quantitative thresholds applied to the Company’s

financial statements.

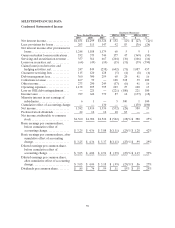

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Managment’s Discussion and Analysis of Financial Condition and Results of Operations discusses our

consolidated financial statements, which have been prepared in accordance with generally accepted

accounting principles in the Unites States (“GAAP”). The preparation of these financial statements

requires management to make estimates and assumptions that affect the reported amounts of assets and

liabilities and the reported amounts of income and expenses during the reporting periods. We base our

estimates and judgments on historical experience and on various other factors that we believe are

reasonable under the circumstances. Actual results may differ from these estimates under varying

assumptions or conditions. Note 2 to the consolidated financial statements, “Significant Accounting

Policies,” includes a summary of the significant accounting policies and methods used in the preparation of

our consolidated financial statements.

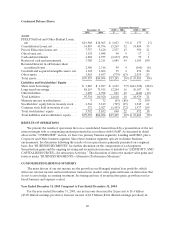

On an ongoing basis, management evaluates its estimates, particularly those that include the most

difficult, subjective or complex judgments and are often about matters that are inherently uncertain. These

estimates relate to the following accounting policies that are discussed in more detail below: application of

the effective interest method for loans (premiums, discounts and Borrower Benefits), securitization

accounting and Retained Interests, provisions for loan losses, and derivative accounting. Also, as part of

our regular quarterly evaluation of the critical estimates used by the Company, we have updated a number

of estimates to account for the increase in Consolidation Loan activity.

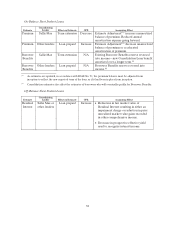

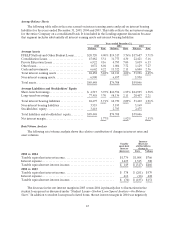

Premiums, Discounts and Borrower Benefits

For both federally insured and Private Education Loans, we account for premiums paid, discounts

received and certain origination costs incurred on the origination of student loans in accordance with

SFAS No. 91, “Accounting for Nonrefundable Fees and Costs Associated with Originating or Acquiring

Loans and Initial Direct Costs of Leases.” The unamortized portion of the premiums and the discounts is

included in the carrying value of the student loan on the consolidated balance sheet. We recognize income

on our student loan portfolio based on the expected yield of the student loan after giving effect to the

amortization of purchase premiums and accretion of student loan discounts, as well as the impact of

Borrower Benefits. In arriving at the expected yield, we must make a number of estimates that when

changed must be reflected as a cumulative catch-up from the inception of the student loan. The most

sensitive estimate for premium and discount amortization is the estimate of the Constant Prepayment Rate

(“CPR”) which measures the rate at which loans in the portfolio pay before their stated maturity. The CPR

is used in calculating the average life of the portfolio. A number of factors can affect the CPR estimate

such as the rate of Consolidation Loan activity and default rates. Changes in CPR estimates are discussed

in more detail below.