Sallie Mae 2005 Annual Report Download - page 210

Download and view the complete annual report

Please find page 210 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214

|

|

A-12

Student loans are discharged if the borrower becomes totally and permanently disabled. A physician

must certify eligibility for discharge.

If a school closes while a student is enrolled, or within 90 days after the student withdrew, loans made

for that enrollment period are discharged. If a school falsely certifies that a borrower is eligible for the

loan, the loan may be discharged. And if a school fails to make a refund to which a student is entitled, the

loan is discharged to the extent of the unpaid refund.

Rehabilitation of Defaulted Loans

The Department of Education is authorized to enter into agreements with the guarantor under which

the guarantor may sell defaulted loans that are eligible for rehabilitation to an eligible lender. For a loan to

be eligible for rehabilitation, the guarantor must have received reasonable and affordable payments for 12

months (reduced to 9 payments in 10 months effective July 1, 2006), then the borrower may request that

the loan be rehabilitated. Because monthly payments are usually greater after rehabilitation, not all

borrowers opt for rehabilitation. Upon rehabilitation, a borrower is again eligible for all the benefits under

the Higher Education Act for which he or she is not eligible as a default, such as new federal aid, and the

negative credit record is expunged. No student loan may be rehabilitated more than once.

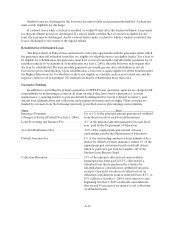

Guarantor Funding

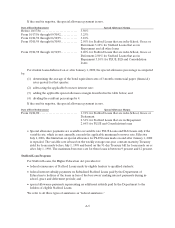

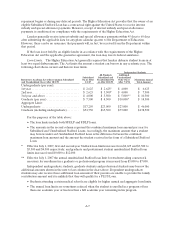

In addition to providing the primary guarantee on FFELP loans, guarantee agencies are charged with

responsibility for maintaining records on all loans on which they have issued a guarantee (“account

maintenance”), assisting lenders to prevent default by delinquent borrowers (“default aversion”), post-

default loan administration and collections and program awareness and oversight. These activities are

funded by revenues from the following statutorily prescribed sources plus earnings on investments.

Source Basis

Insurance Premium......................... Up to 1% of the principal amount guaranteed, withheld

(Changes to Federal Default Fee July 1, 2006) from the proceeds of each loan disbursement.

Loan Processing andIssuance Fee............ .4% of the principal amount guaran

teed in each fiscal

year, paid by the Department of Education.

Account Maintenance Fee................... .10%of the original principal amountof loans

outstanding, paid by the Department of Education.

Default Aversion Fee....................... 1%of the outstanding amount of loans submitted by a

lender for default aversion assistance, minus 1% of the

unpaid principal and interest paid on default claims,

which is, paid once per loan by transfers out of the

Student Loan Reserve Fund.

Collection Retention ....................... 23% of the amount collected on loans on which

reinsurance has been paid (18.5% collected for a

defaulted loan that is purchased by a lender for

rehabilitation or consolidation), withheld from gross

receipts. Guarantor retention of collection fees on

defaulted consolidation loans is reduced from 18.5% to

10% (effective October 1, 2006), and reduced to zero

beginning October 1, 2009 on default consolidations

that exceed 45 percent of an agency’s total collections

on defaulted loans.