Sallie Mae 2005 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

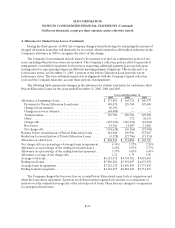

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)

F-27

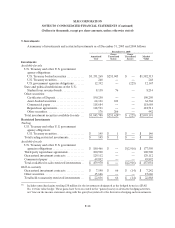

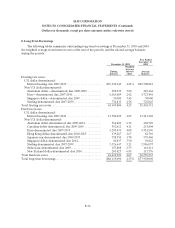

4. Allowance for Student Loan Losses (Continued)

Delinquencies

The table below shows the Company’s Private Education Loan delinquency trends as of December 31,

2005, 2004 and 2003. Delinquencies have the potential to adversely impact earnings if the account charges

off and results in increased servicing and collection costs.

December 31,

2005 2004 2003

(Dollars in millions) Balance % Balance % Balance %

Loans in-school/grace/deferment(1) ............... $4,301 $2,787 $1,970

Loans in forbearance(2) .......................... 303 166 236

Loans in repayment and percentage of each status:

Loanscurrent................................ 3,311 90.4% 2,555 89.9% 2,268 88.9%

Loans delinquent 31-60 days(3) ................. 166 4.5 124 4.4 115 4.5

Loans delinquent 61-90 days................... 77 2.1 56 2.0 62 2.4

Loans delinquent greater than90 days.......... 108 3.0 107 3.7 106 4.2

Total Private Education Loans in repayment..... 3,662 100% 2,842 100

% 2,551 100.0%

Total PrivateEducation Loans, gross ............. 8,266 5,795 4,757

Private Education Loanunamortized discount..... (305) (203) (121 )

Total PrivateEducation Loans................... 7,961 5,592 4,636

Private Education Loan allowance for losses....... (204) (172) (166 )

Private Education Loans, net .................... $7,757 $5,420 $4,470

Percentage of Private Education Loans

inrepayment ................................ 44.3% 49.0% 53.6 %

Delinquencies as a percentage of Private Education

Loans in repayment .......................... 9.6% 10.1% 11.1 %

(1) Loans for borrowers who still may be attending school or engaging in other permitted educational activities and

are not yet required to make payments on the loans, e.g., residency periods for medical students or a grace period

for bar exam preparation.

(2) Loans for borrowers who have requested extension of grace period during employment transition or who have

temporarily ceased making full payments due to hardship or other factors, consistent with the established loan

program servicing procedures and policies.

(3) The period of delinquency is based on the number of days scheduled payments are contractually past due.