Sallie Mae 2005 Annual Report Download - page 208

Download and view the complete annual report

Please find page 208 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214

|

|

A-10

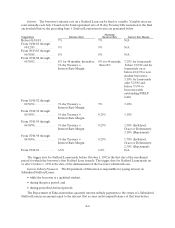

received before January 1, 1993, Consolidation Loans were available only to borrowers who had aggregate

outstanding student loan balances of at least $5,000.

To obtain a Consolidation Loan, the borrower must be either in repayment status or in a grace period

before repayment begins. In addition, for applications received before January 1, 1993, the borrower must

not have been delinquent by more than 90 days on any student loan payment. Married couples who agree

to be jointly and severally liable will be treated as one borrower for purposes of loan consolidation

eligibility.

Consolidation Loans bear interest at a fixed rate equal to the greater of the weighted average of the

interest rates on the unpaid principal balances of the consolidated loans and 9 percent for loans originated

before July 1, 1994. For Consolidation Loans made on or after July 1, 1994 and for which applications were

received before November 13, 1997, the weighted average interest rate is rounded up to the nearest whole

percent. Consolidation Loans made on or after July 1, 1994 for which applications were received on or

after November 13, 1997 through September 30, 1998 bear interest at the annual variable rate applicable to

Stafford Loans subject to a cap of 8.25 percent. Consolidation Loans for which the application is received

on or after October 1, 1998 bear interest at a fixed rate equal to the weighted average interest rate of the

loans being consolidated rounded up to the nearest one-eighth of one percent, subject to a cap of 8.25

percent.

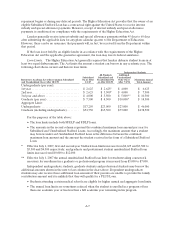

Interest on Consolidation Loans accrues and, for applications received before January 1, 1993, is paid

without interest subsidy by the Department. For Consolidation Loans for which applications were received

between January 1 and August 10, 1993, all interest of the borrower is paid during deferral periods.

Consolidation Loans for which applications were received on or after August 10, 1993 are only subsidized

if all of the underlying loans being consolidated were Subsidized Stafford Loans. In the case of

Consolidation Loans made on or after November 13, 1997, the portion of a Consolidation Loan that is

comprised of Subsidized FFELP Loans and Subsidized FDLP Loans retains subsidy benefits during

deferral periods.

No insurance premium is charged to a borrower or a lender in connection with a Consolidation Loan.

However, lenders must pay a monthly rebate fee to the Department at an annualized rate of 1.05 percent

on principal and interest on Consolidation Loans for loans disbursed on or after October 1, 1993, and at an

annualized rate of 0.62 percent for Consolidation Loan applications received between October 1, 1998 and

January 31, 1999. The rate for special allowance payments for Consolidation Loans is determined in the

same manner as for other FFELP loans.

A borrower must begin to repay his Consolidation Loan within 60 days after his consolidated loans

have been discharged. For applications received on or after January 1, 1993, repayment schedule options

include graduated, income-sensitive, and extended (for new borrowers on or after October 7, 1998)

repayment plans, and loans are repaid over periods determined by the sum of the Consolidation Loan and

the amount of the borrower’s other eligible student loans outstanding. The maximum maturity schedule is

30 years for indebtedness of $60,000 or more.

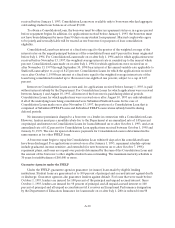

Guarantee Agencies under the FFELP

Under the FFELP, guarantee agencies guarantee (or insure) loans made by eligible lending

institutions. Student loans are guaranteed as to 100 percent of principal and accrued interest against death

or discharge. Guarantee agencies also guarantee lenders against default. For loans that were made before

October 1, 1993, lenders are insured for 100 percent of the principal and unpaid accrued interest. Since

October 1, 1993, lenders are insured for 98 percent of principal and all unpaid accrued interest or 100

percent of principal and all unpaid accrued interest if it receives an Exceptional Performance designation

by the Department of Education. Insurance for loans made on or after July 1, 2006 is reduced from 98