Sallie Mae 2005 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

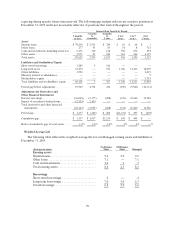

91

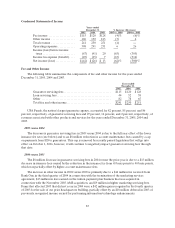

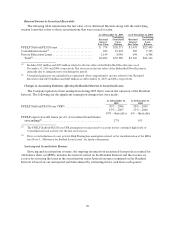

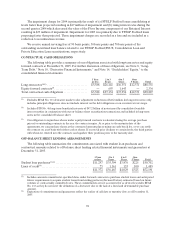

The following table summarizes the components of servicing and securitization revenue for the years

ended December 31, 2005, 2004 and 2003.

Years ended December 31,

2005 2004 2003

Servicingrevenue ............................................. $ 323 $ 326 $ 314

Securitization revenue, before Embedded Floor

Income and impairment...................................... 270 230 269

Servicing and securitization revenue, before

Embedded Floor Income and impairment ...................... 593 556 583

Embedded Floor Income....................................... 81 241 337

Less: Floor Income previously recognized in

gain calculation............................................. (57) (156) (157)

Net Embedded Floor Income ................................... 24 85 180

Servicing andsecuritizationrevenue, before impairment ........... 617 641 763

Retained Interest impairment................................... (260) (80) (96)

Total servicing and securitization revenue........................ $ 357 $ 561 $ 667

Average off-balance sheet student loans.......................... $41,220 $40,558 $ 38,205

Average balance of Retained Interest ............................ $ 2,476 $ 2,434 $ 2,615

Servicing and securitization revenue as a percentage of the average

balance of off-balance sheet student loans (annualized).......... .87% 1.38% 1.74%

Servicing and securitization revenue is primarily driven by the average balance of off-balance sheet

student loans and the amount of and the difference in the timing of Embedded Floor Income recognition

on off-balance sheet student loans. Servicing and securitization revenue can also be negatively impacted by

impairments of the value of our Retained Interest, caused primarily by the effect of higher than expected

Consolidation Loan activity on FFELP Stafford/PLUS student loan securitizations and the effect of

market interest rates on the Embedded Floor Income included in the Retained Interest. When loans in a

securitization trust consolidate, they are a prepayment to the trust resulting in a shorter average life. We

use a CPR assumption to estimate the effect of trust prepayments from loan consolidation and other

factors on the life of the trust. When consolidation activity is higher than forecasted, the Residual Interest

asset can be impaired and the yield used to recognize subsequent income from the trust is negatively

impacted. The majority of the consolidations bring the loans back on-balance sheet so for those loans we

retain the value of the asset on-balance sheet versus in the trust. For the years ended December 31, 2005,

2004 and 2003, we recorded impairments to the Retained Interests of $260 million, $80 million and $96

million, respectively. The impairment charge in 2005 was primarily caused by the effect of record levels of

consolidation activity as well as the increase of expected future CPR assumptions used to value the

Residual Interest. This surge in Consolidation Loan activity was due to FFELP Stafford borrowers locking

in lower interest rates by consolidating their loans prior to the July 1 interest rate reset for FFELP Stafford

loans. The level and timing of Consolidation Loan activity is highly volatile, and in response we continue to

revise our estimates of the effects of Consolidation Loan activity on our Retained Interests and it may

result in additional impairment recorded in future periods if Consolidation Loan activity remains higher

than projected. Our FFELP Retained Interests were also impaired by $23 million to account for the effect

of the one percent Risk Sharing loss applied to student loans receiving the EP designation. The increase in

Risk Sharing was included in legislation reauthorizing the Higher Education Act (see “OTHER

RELATED EVENTS AND INFORMATION—Reauthorization”). See “LENDING BUSINESS

SEGMENT—Allowance for FFELP Student Loans” for further discussion regarding the change in the

Risk Sharing exposure.