Sallie Mae 2005 Annual Report Download - page 148

Download and view the complete annual report

Please find page 148 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(Dollars in thousands, except per share amounts, unless otherwise stated)

F-26

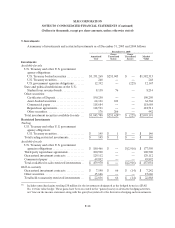

4. Allowance for Student Loan Losses (Continued)

During the third quarter of 2005, the Company changed its methodology for estimating the amount of

charged off student loans that will ultimately be recovered, which resulted in a $49 million reduction in the

Company’s allowance in 2005 to recognize the effect of this change.

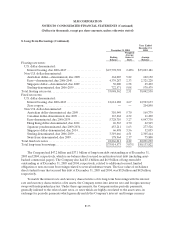

The Company’s loss estimates include losses to be incurred over the loss confirmation period of two

years, including when the borrowers are in school. The Company’s collection policies allow for periods of

nonpayment, or modified repayment, for borrowers requesting additional payment grace periods upon

leaving school or experiencing temporary difficulty meeting payment obligations. This is referred to as

forbearance status. At December 31, 2005, 4 percent of the Private Education Loan portfolio was in

forbearance status. The loss confirmation period is in alignment with the Company’s typical collection

cycle and the Company takes into account these periods of nonpayment.

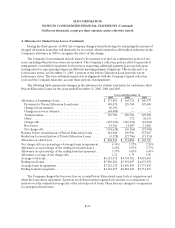

The following table summarizes changes in the allowance for student loan losses for on-balance sheet

Private Education Loans for the years ended December 31, 2005, 2004 and 2003.

Years ended December 31,

2005 2004 2003

Allowance at beginning of year............................. $ 171,886 $ 165,716 $ 180,933

Provision for Private Education Loan losses ............... 185,078 129,768 107,408

Change in loss estimate................................. 40,192 — —

Change in recovery estimate............................. (48,488) — —

Totalprovision......................................... 176,782 129,768 107,408

Other................................................. — 372 20,631

Charge-offs............................................ (153,994) (110,271) (83,001)

Recoveries............................................ 19,366 14,007 11,096

Net charge-offs ........................................ (134,628) (96,264) (71,905)

Balance before securitization of Private Education Loans ..... 214,040 199,592 237,067

Reduction for securitization ofPrivate Education Loans ...... (9,928) (27,706) (71,351)

Allowance at end of year .................................. $ 204,112 $ 171,886 $ 165,716

Net charge-offs as a percentage of average loans in repayment . 4.14% 3.57% 2.59%

Allowance as a percentage of the ending total loan balance .... 2.56% 3.07% 3.57%

Allowance as a percentage of the ending loans in repayment . . . 5.57% 6.05% 6.50%

Allowance coverage of net charge-offs ...................... 1.52 1.79 2.30

Averagetotalloans....................................... $6,921,975 $4,794,782 $5,018,491

Endingtotalloans........................................ $7,960,882 $5,591,497 $4,635,872

Average loans in repayment............................... $3,252,238 $2,696,818 $2,771,815

Endingloansinrepayment ................................ $3,662,255 $2,842,220 $2,551,415

The Company charges the borrower fees on certain Private Education Loans, both at origination and

when the loan enters repayment. Such fees are deferred and recognized into income as a component of

interest over the estimated average life of the related pool of loans. These fees are charged to compensate

for anticipated loan losses.