Sallie Mae 2005 Annual Report Download - page 65

Download and view the complete annual report

Please find page 65 of the 2005 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

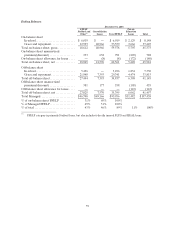

55

institutions on a constant, inflation-adjusted basis since the academic year (“AY”) 1995-1996 and are

projected to continue to rise at a pace greater than inflation. Management believes that these factors will

drive growth in education financing well into the next decade.

On March 22, 2005, the Company announced that it extended both its JPMorgan Chase and Bank

One student loan and loan purchase commitments to August 31, 2010. This comprehensive agreement

provided for the dissolution of the joint venture between Chase and Sallie Mae that had been making

student loans under the Chase brand since 1996 and resolved a lawsuit filed by Chase on February 17,

2005.

JPMorgan Chase will continue to sell substantially all student loans to the Company (whether made

under the Chase or Bank One brand) that are originated or serviced on the Company’s platforms. In

addition, the agreement provides that substantially all Chase-branded education loans made for the July 1,

2005 to June 30, 2006 academic year (and future loans made to these borrowers) will be sold to the

Company, including certain loans that are not originated or serviced on Sallie Mae platforms.

This agreement permits JPMorgan Chase to compete with the Company in the student loan

marketplace and releases the Company from its commitment to market the Bank One and Chase brands

on campus. The Company will continue to support its school customers through its comprehensive set of

products and services, including its loan origination and servicing platforms, its family of lending brands

and strategic lending partners.

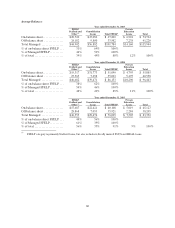

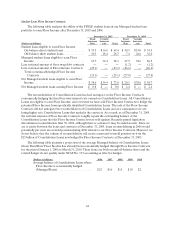

Over the past three years, we have experienced a surge in Consolidation Loan activity as a result of

historically low interest rates and aggressive marketing in the industry which has substantially changed the

composition of our student loan portfolio. Consolidation Loans earn a lower yield than FFELP Stafford

loans due primarily to the 105 basis point Consolidation Loan Rebate Fee. This negative impact is

somewhat mitigated by higher SAP spreads, the longer average life of Consolidation Loans and the greater

potential to earn Floor Income. Since interest rates on Consolidation Loans are fixed to term for the

borrower, older Consolidation Loans with higher borrower rates can earn Floor Income over an extended

period of time. In both 2004 and 2005, substantially all Floor Income was earned on Consolidation Loans.

The HEA requires lenders to rebate Floor Income on all FFELP loans originated after April 1, 2006, so

this benefit will gradually decrease over time. During 2005, $17.1 billion of FFELP Stafford loans in our

Managed loan portfolio consolidated either with us ($14.0 billion) or with other lenders ($3.1 billion). The

net result of consolidation activity in 2005 was a net portfolio loss of $26 million. Consolidation Loans now

represent over 73 percent of our on-balance sheet federally guaranteed student loan portfolio and over

62 percent of our Managed federally guaranteed portfolio.

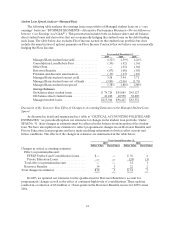

During 2005, the surge in consolidations was abetted by new industry practices. First, borrowers, who

elected to have their Consolidation Loans prematurely enter repayment, were permitted for the first time

to consolidate their loans while still in school, due to an interpretation of the HEA that allows borrowers

to voluntarily transfer into repayment status before graduation. Previously, borrowers typically only

consolidated FFELP Stafford loans upon graduation. Second, a significant volume of our Consolidation

Loans was consolidated with third party lenders using the Direct Lending program as a pass-through entity

to circumvent the statutory prohibition on the FFELP reconsolidation of Consolidation Loans. The HEA

eliminates this practice by July 1, 2006, but we are working with others in the industry to end it before

June 30, 2006, because we believe that this practice is improper and not permitted by current regulations.

This practice contributed to a net run-off of $540 million in our portfolio in the fourth quarter of 2005,

which will continue at a high rate until this practice ceases.

To meet the increasing cost of higher education, students and parents have turned to alternative

sources of education financing outside of the FFELP. A large and growing source of this supplemental

education financing is provided by Private Education Loans, for which we are the largest provider. These

loans are primarily originated through campus-based programs but this channel has recently been