PNC Bank 2014 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

The discount rate used to measure pension obligations is

determined by comparing the expected future benefits that

will be paid under the plan with yields available on high

quality corporate bonds of similar duration. The impact on

pension expense of a .5% decrease in discount rate in the

current environment is an increase of $18 million per year.

This sensitivity depends on the economic environment and

amount of unrecognized actuarial gains or losses on the

measurement date.

The expected long-term return on assets assumption also has a

significant effect on pension expense. The expected return on

plan assets is a long-term assumption established by

considering historical and anticipated returns of the asset

classes invested in by the pension plan and the asset allocation

policy currently in place. For purposes of setting and

reviewing this assumption, “long term” refers to the period

over which the plan’s projected benefit obligations will be

disbursed. We review this assumption at each measurement

date and adjust it if warranted. Our selection process

references certain historical data and the current environment,

but primarily utilizes qualitative judgment regarding future

return expectations.

To evaluate the continued reasonableness of our assumption,

we examine a variety of viewpoints and data. Various studies

have shown that portfolios comprised primarily of U.S. equity

securities have historically returned approximately 9%

annually over long periods of time, while U.S. debt securities

have returned approximately 6% annually over long periods.

Application of these historical returns to the plan’s allocation

ranges for equities and bonds produces a result between 6.50%

and 7.25% and is one point of reference, among many other

factors, that is taken into consideration. We also examine the

plan’s actual historical returns over various periods and

consider the current economic environment. Recent

experience is considered in our evaluation with appropriate

consideration that, especially for short time periods, recent

returns are not reliable indicators of future returns. While

annual returns can vary significantly (actual returns for 2014,

2013 and 2012 were +6.50%, +15.48%, and +15.29%,

respectively), the selected assumption represents our estimated

long-term average prospective returns.

Acknowledging the potentially wide range for this

assumption, we also annually examine the assumption used by

other companies with similar pension investment strategies, so

that we can ascertain whether our determinations markedly

differ from others. In all cases, however, this data simply

informs our process, which places the greatest emphasis on

our qualitative judgment of future investment returns, given

the conditions existing at each annual measurement date.

Taking into consideration all of these factors, the expected

long-term return on plan assets for determining net periodic

pension cost for 2014 was 7.00%, down from 7.50% for 2013.

After considering the views of both internal and external

capital market advisors, particularly with regard to the effects

of the recent economic environment on long-term prospective

fixed income returns, we are reducing our expected long-term

return on assets to 6.75% for determining pension cost for

2015.

Under current accounting rules, the difference between

expected long-term returns and actual returns is accumulated

and amortized to pension expense over future periods. Each

one percentage point difference in actual return compared

with our expected return can cause expense in subsequent

years to increase or decrease by up to $9 million as the impact

is amortized into results of operations.

We currently estimate pretax pension expense of $9 million in

2015 compared with pretax income of $7 million in 2014.

This year-over-year expected increase in expense reflects the

effects of the lower expected return on asset assumption,

improved mortality, and the lower discount rate required to be

used in 2015. These factors will be partially offset by the

favorable impact of the increase in plan assets at

December 31, 2014 and the assumed return on a $200 million

voluntary contribution to the plan made in February 2015.

The table below reflects the estimated effects on pension

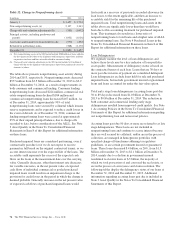

expense of certain changes in annual assumptions, using 2015

estimated expense as a baseline.

Table 26: Pension Expense – Sensitivity Analysis

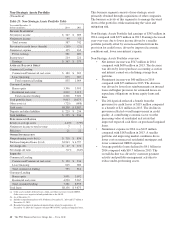

Change in Assumption (a)

Estimated

Increase/(Decrease)

to 2015

Pension

Expense

(In millions)

.5% decrease in discount rate $18

.5% decrease in expected long-term return on

assets $22

.5% increase in compensation rate $ 2

(a) The impact is the effect of changing the specified assumption while holding all other

assumptions constant.

Our pension plan contribution requirements are not

particularly sensitive to actuarial assumptions. Investment

performance has the most impact on contribution requirements

and will drive the amount of required contributions in future

years. Also, current law, including the provisions of the

Pension Protection Act of 2006, sets limits as to both

minimum and maximum contributions to the plan.

Notwithstanding the voluntary contribution made in February

2015 noted above, we do not expect to be required to make

any contributions to the plan during 2015.

We maintain other defined benefit plans that have a less

significant effect on financial results, including various

nonqualified supplemental retirement plans for certain

employees, which are described more fully in Note 13

Employee Benefit Plans in the Notes To Consolidated

Financial Statements in Item 8 of this Report.

66 The PNC Financial Services Group, Inc. – Form 10-K