PNC Bank 2014 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

N

OTE

4P

URCHASED

L

OANS

Purchased Impaired Loans

Purchased impaired loan accounting addresses differences

between contractual cash flows and cash flows expected to be

collected from the initial investment in loans if those

differences are attributable, at least in part, to credit quality.

Several factors were considered when evaluating whether a

loan was considered a purchased impaired loan, including the

delinquency status of the loan, updated borrower credit status,

geographic information, and updated LTV. GAAP allows

purchasers to account for loans individually or to aggregate

purchased impaired loans acquired in the same fiscal quarter

into one or more pools, provided that the loans have common

risk characteristics. A pool is then accounted for as a single

asset with a single composite interest rate and an aggregate

expectation of cash flows. Purchased impaired homogeneous

consumer, residential real estate and smaller balance

commercial loans with common risk characteristics are

aggregated into pools where appropriate, whereas commercial

loans with a total commitment greater than a defined threshold

are accounted for individually. For pooled loans, proceeds of

individual loans are not applied individually to each loan

within a pool, but to the pool’s recorded investment since it is

accounted for as a single asset. Upon final disposition of a

loan within a pool (e.g., payoff, short-sale, foreclosure, etc.),

the loan’s carrying value is removed from the pool and any

gain or loss associated with the transaction is retained in the

pool’s recorded investment. For example, upon final

disposition of a loan by short-sale, the proceeds of the short-

sale may be less (or more) than the loan’s recorded

investment. This shortfall or loss (excess or gain) is not

accounted for as an individual loan sale in our income

statement and is instead retained as part of the pool’s recorded

investment consistent with our accounting for the pool as a

single asset. This treatment is designed to maintain a constant

effective yield for recognition of interest income.

Accordingly, a pool’s recorded investment includes the net

accumulation of realized losses or gains attributable to these

final dispositions. As there are no future expected cash flows

related to these dispositions, their net carrying value is $0. The

recorded investment, including these realized losses and gains,

is evaluated for collectability based upon the net present value

of the pool’s remaining expected cash flows when establishing

our allowance for loan losses. See below and Note 1

Accounting Policies and Note 5 Allowances for Loan and

Lease Losses and Unfunded Loan Commitments and Letters

of Credit for additional information.

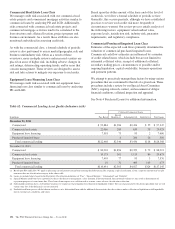

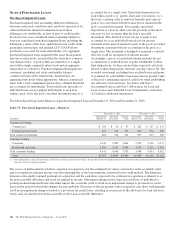

The following table provides balances of purchased impaired loans at December 31, 2014 and December 31, 2013:

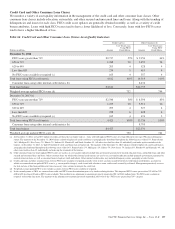

Table 71: Purchased Impaired Loans – Balances

December 31, 2014 December 31, 2013

In millions

Outstanding

Balance (a)

Recorded

Investment

Carrying

Value

Outstanding

Balance (a)

Recorded

Investment

Carrying

Value

Commercial lending

Commercial $ 159 $ 74 $ 57 $ 282 $ 157 $ 131

Commercial real estate 307 236 174 655 516 409

Total commercial lending 466 310 231 937 673 540

Consumer lending

Consumer 2,145 1,989 1,661 2,523 2,312 1,971

Residential real estate 2,396 2,559 2,094 3,025 3,121 2,591

Total consumer lending 4,541 4,548 3,755 5,548 5,433 4,562

Total $5,007 $4,858 $3,986 $6,485 $6,106 $5,102

(a) Outstanding balance represents the balance on the loan servicing system for active loans. It is possible for the outstanding balance to be lower than the recorded investment for certain

loans due to the use of pool accounting.

The excess of undiscounted cash flows expected at acquisition over the estimated fair value is referred to as the accretable yield

and is recognized as interest income over the remaining life of the loan using the constant effective yield method. The difference

between contractually required payments at acquisition and the cash flows expected to be collected at acquisition is referred to as

the non-accretable difference and is not recognized in income. Subsequent changes in the expected cash flows of individual or

pooled purchased impaired loans will either impact the accretable yield or result in an impairment charge to provision for credit

losses in the period in which the changes become probable. Decreases to the net present value of expected cash flows will generally

result in an impairment charge recorded as a provision for credit losses, resulting in an increase to the allowance for loan and lease

losses, and a reclassification from accretable yield to non-accretable difference.

142 The PNC Financial Services Group, Inc. – Form 10-K