PNC Bank 2014 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2014 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

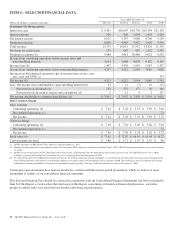

• Noninterest income was $6.9 billion for 2014 and

2013, as strong overall client fee income was offset

by lower residential mortgage revenue, declines in

asset valuations and reduced sales of securities.

• The provision for credit losses decreased to $273

million for 2014 compared to $643 million for 2013

due to overall credit quality improvement.

• Noninterest expense was $9.5 billion for 2014, a

decrease of 2% compared with 2013, primarily

reflecting well managed expenses.

Credit Quality Highlights

• Asset quality trends in 2014 improved from 2013.

For additional detail, see the Credit Risk

Management portion of the Risk Management section

of this Item 7.

• Nonperforming assets decreased $.6 billion, or 17%,

to $2.9 billion at December 31, 2014 compared to

December 31, 2013. Nonperforming assets to total

assets were 0.83% at December 31, 2014, compared

to 1.08% at December 31, 2013.

• Overall loan delinquencies of $1.9 billion at

December 31, 2014 decreased $.5 billion, or 22%,

compared with December 31, 2013.

• The allowance for loan and lease losses was 1.63% of

total loans and 133% of nonperforming loans at

December 31, 2014, compared with 1.84% and 117%

at December 31, 2013, respectively.

• Net charge-offs of $.5 billion in 2014 declined 51%

compared to net charge-offs of $1.1 billion for 2013.

Net charge-offs were 0.27% of average loans in 2014

and 0.57% of average loans in 2013. These

comparisons were impacted by alignment with

interagency guidance in the first quarter of 2013 on

practices for loans and lines of credit related to

consumer lending. In the first quarter 2013, this

alignment had the overall effect of (i) accelerating

charge-offs, (ii) increasing nonperforming loans and

(iii) in the case of loans accounted for under the fair

value option, increasing nonaccrual loans.

Balance Sheet Highlights

• Total loans increased by $9.2 billion to $205 billion

at December 31, 2014 compared to December 31,

2013.

• Total commercial lending increased by $11.2

billion, or 10%, as a result of growth in

commercial and commercial real estate loans.

• Total consumer lending decreased $2.0 billion,

or 3%, due to lower home equity, education

and residential mortgage loans, partially offset

by growth in automobile loans.

• Total deposits increased by $11.3 billion, or 5%, to

$232 billion at December 31, 2014 compared with

December 31, 2013, driven by growth in transaction

deposits.

• PNC further increased its liquidity position as

reflected in higher deposit balances maintained with

the Federal Reserve Bank.

• The regulatory short-term Liquidity Coverage

Ratio became effective for PNC as an advanced

approaches bank beginning January 1, 2015,

with a minimum phased-in requirement of 80%

in 2015, calculated as of month end. The

estimated pro forma ratio at December 31,

2014 exceeded 100% and 95% for PNC and

PNC Bank, respectively.

• PNC’s well-positioned balance sheet remained core

funded with a loans to deposits ratio of 88% at

December 31, 2014.

• The Transitional Basel III common equity Tier 1

capital ratio, calculated using the regulatory capital

methodology applicable to PNC during 2014, was

10.9% at December 31, 2014.

• Pro forma fully phased-in Basel III common equity

Tier 1 capital ratio increased to an estimated 10.0% at

December 31, 2014 from 9.4% at December 31, 2013

based on the standardized approach rules. See the

Capital discussion and Table 18 in the Consolidated

Balance Sheet Review section of this Item 7 and the

December 31, 2013 capital ratio tables in the

Statistical Information (Unaudited) section in Item 8

of this Report for more detail.

Our Consolidated Income Statement and Consolidated

Balance Sheet Review sections of this Item 7 describe in

greater detail the various items that impacted our results

during 2014 and 2013 and balances at December 31, 2014 and

December 31, 2013, respectively.

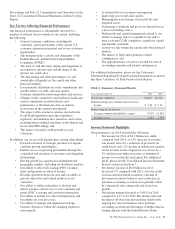

Capital and Liquidity Actions

Our ability to take certain capital actions, including plans to

pay or increase common stock dividends or to repurchase

shares under current or future programs, is subject to the

results of the supervisory assessment of capital adequacy

undertaken by the Federal Reserve and our primary bank

regulators as part of the CCAR process.

In connection with the 2014 CCAR, PNC submitted its 2014

capital plan, as approved by its Board of Directors, to the

Federal Reserve in January 2014. As we announced on

March 26, 2014, the Federal Reserve accepted the capital plan

and did not object to our proposed capital actions, which

included a recommendation to increase the quarterly common

stock dividend in the second quarter of 2014. The capital plan

also included share repurchase programs of up to $1.5 billion

for the four quarter period beginning in the second quarter of

2014 under PNC’s existing common stock repurchase

authorization. These programs include repurchases of up to

$200 million to mitigate the financial impact of employee

benefit plan transactions. In the last three quarters of 2014, in

34 The PNC Financial Services Group, Inc. – Form 10-K